Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

In my previous article, I discussed how the U.S. Treasury yield curve foretells an imminent bull market in U.S. Treasury bonds. This article corroborates those findings from the perspective of the housing market.

Among leading indicators, the housing market predicts economic activity with the longest lead time. Housing market indicators peaked far before the last three recessions – before the yield curve inverted, the Fed finished raising rates, U.S. Treasury yields peaked, and even before the index of leading indicators (of which building permits is a part) peaked. Logically, because the housing market represents the full breadth of the economy and its health is negatively affected by higher interest rates, it has slowed well before other indicators. An article on this here.

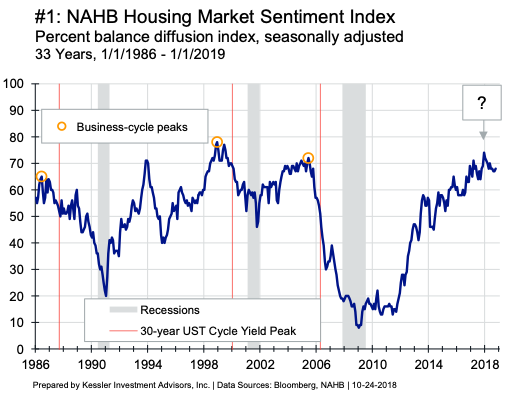

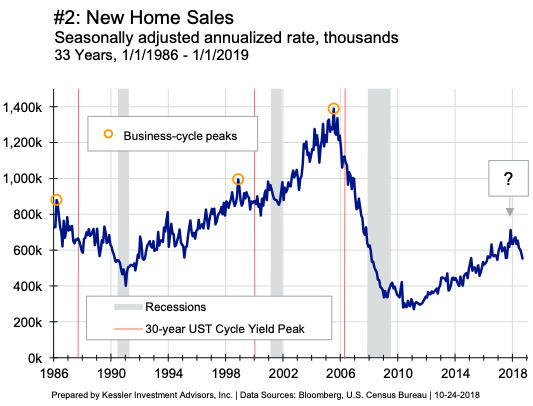

Of the many housing indicators, four have the longest history and most reliable leading properties. In their charts below, notice that the business cycle peaks (orange circles) precede the peaks in the 30-year yield (red lines) which come before the recessions (gray bars).

With the October 24th new-home sales report, the September 2018 housing data has been released and cements that a housing market peak occurred late last year/early this year. Specifically, the tentative peaks occurred between seven and 11 months ago (gray boxes with question marks in charts above):

- New home sales, November 2017

- National Association of Home Builders (NAHB) sentiment index, December 2017

- Housing starts, January 2018

- Building permits, March 2018

There is no guarantee that these indicators won’t turn around and make new highs – a cycle peak is subjective until much later. But, with the indicators peaking contemporaneously, the nine-and-a-quarter-year age of the economic expansion and corroboration with the yield curve, it is likely housing is past its best cyclical level.

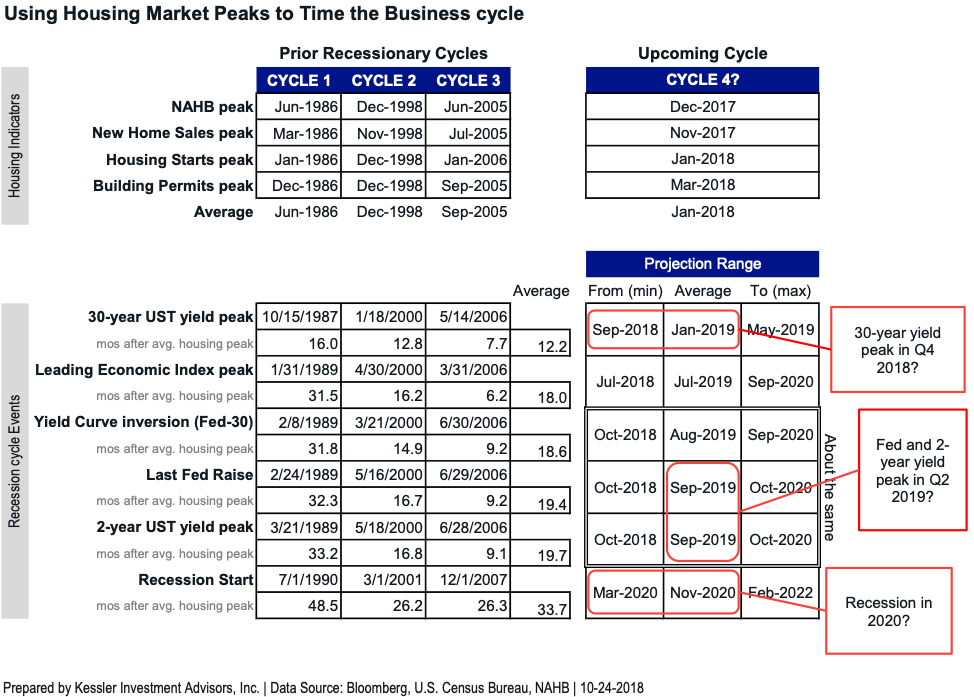

The lead time between prior housing-market peaks and various business-cycle events can be used to project timing in this upcoming hypothetical cycle four (see table below):

The timing suggested in this study matches the findings of my prior article to within three months. It suggests a 30-year yield peak this quarter, the Fed funds rate and two-year yield peaking next year and a recession in 2020. These results most certainly oversimplify the uncertain nature of markets, but business cycles have more similarities than are readily known. It is helpful to be aware of them.

Eric Hickman is president of Kessler Investment Advisors, an advisory firm located in Denver, Colorado specializing in U.S. Treasury bonds.

Read more articles by Eric Hickman