Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

With the economic expansion nine months from being the longest in U.S. history, the yield curve nearly flat and housing market indicators peaking earlier this year, it doesn’t take much imagination to see what’s next: a recession and falling interest rate cycle – i.e., a U.S. Treasury bull market. This article studies the history of these cycles and offers a roadmap for the upcoming one.

The history

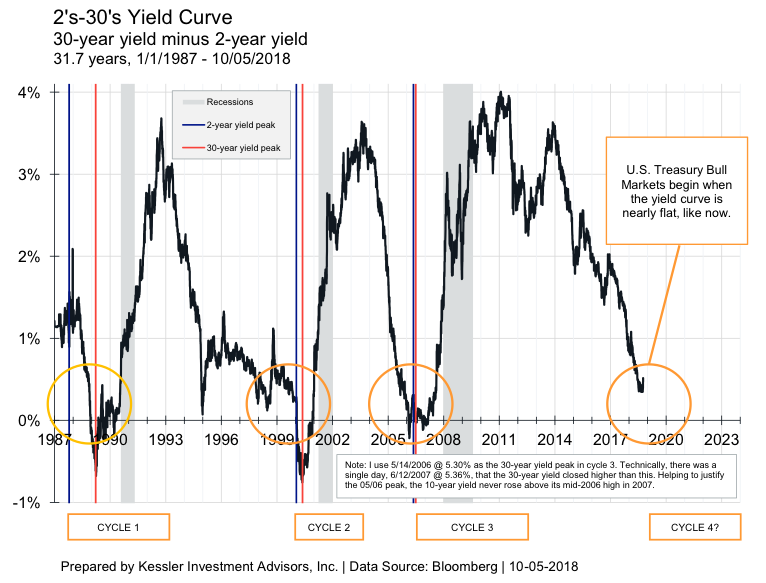

There have been three major U.S. Treasury bull markets coinciding with recessions in the last 30 years (orange boxed areas in the chart below). They all look remarkably similar and the periods leading up to them look a lot like now.

First, in all of them, the two-year yield peaked within a month of the last Fed raise in the raising cycle. On average, the 30-year yield peaked about seven months before the two-year peak (albeit with a wide range, from one and a half months to 1.4 years) while the Fed was still raising rates. In general, this happens because Fed policy reacts to a narrow view of the economy, half of which is old news.

The Fed is primarily concerned with stable prices (inflation) and employment. Employment is a coincident indicator of the economy, but inflation reliably lags it, often by more than a year. At these yield peaks, the 30-year yield will start falling as financial assets or leading economic indicators start to erode, but inflation tends to still rise (see inflation peaks in chart above) which keeps the Fed, and its closely-linked two-year yield, rising for a longer time.

Second, these bull markets began far before their accompanying recession did. The bull markets started an average of 1.8 years before. This happens because the start of a recession is marked by a decline in real economic activity, yet long-term Treasury yields start to move lower from the mere hint of a slowdown in activity. This is important because many familiar commentators and banks (Ray Dalio, Ben Bernanke, Nouriel Roubini, Mark Zandi, Societe Generale, JP Morgan) are warning of a recession in 2020. This 1.8-year average combined with a mid-2020 recession would suggest a U.S. Treasury bull market beginning around now.

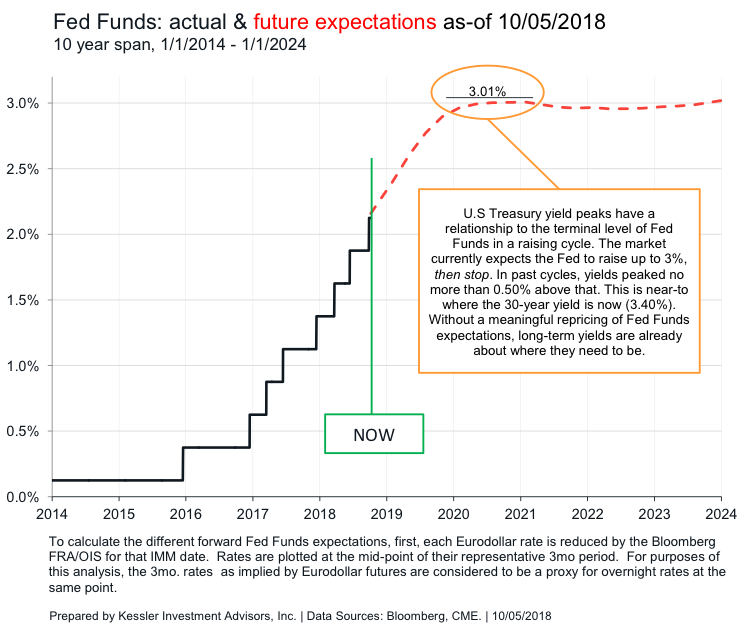

Third, the yield peaks in these cycles have a relationship to the terminal level of Fed Funds. The two-year yield has peaked between 0.02% and 0.43% above the terminal Fed funds rate, the 30-year yield has peaked between 0.05% and 0.47% above the terminal rate. Currently, the market is priced for the Fed to raise rates to 3.0% by mid-2020, then stop. This is another three and a half raises from here (see chart below). The 30-year already yields 3.40% (10/5/2018). If the Fed were to raise to 3.0%, the highest spread would suggest a 3.47% 30-year yield peak, just seven basis points above where it is now.

Finally, these bull markets began after extended periods of the Fed raising rates with a flattening yield curve; the 30-year yield rose slower than the two-year yield. On average, the 30-year yield peaked with a 2’s-30’s curve (the 30-year yield minus the two-year yield) at +0.54% – notably, before the yield curve inverted. The two-year yield peaked with an average inverted 2-30 curve at -0.43%. The 2-30 curve now (10/5/2018) is near the average 30-year peak at +0.52%. See below:

As applied to now

I believe we are close, in time and yield, to the peak in the 30-year yield. Barring an interim geopolitical or economic shock, the Fed will continue to raise rates into the middle of next year, and the two-year yield will drift higher to peak around that same time.

The next recession will be a cousin of the 1937/38 recession, the first recession following the Great Depression that shocked everyone with its ferocity. The S&P 500 lost 49.8% (2/1937-3/1938) during that recession. Because the Fed was so responsive in the 2008 recession, there are still excesses in the economy that haven’t been flushed. The stock market (S&P 500 total return) has returned 18.7% annualized since the 03/2009 low (3/5/2009-10/5/2018). But, its long term average is 10.1% (12/31/1925-09/30/2018) and just 6.1% above the dividend return. The dividend yield of the S&P 500 today is 1.8%. Squaring 18.7% to a 7.9% (6.1% + 1.8%) long-term average is a tremendous mean reversion. Also, China hasn’t had a recession since its statistics began in 1992. Even command economies are not exempt from business cycles. It is entirely likely that the next recession will ensnare the world’s biggest two economies simultaneously, increasing its severity.

The ideal investment to take advantage of the next bull market in U.S. Treasuries is to own the long-end of the yield curve first, and when the Fed stops raising rates, transition to a duration equivalent of the two-year to take advantage of the further distance its yield will likely drop. In a prior article, “The Case for Leveraged U.S. Treasury Bonds”, I explained that without leverage, investors wanting more opportunity from the Treasury market are stuck with longer maturities (i.e., the 30-year U.S. Treasury). Leverage, with its multiplicative effect on returns and volatility, can give any part of the yield curve the same opportunity for a given move in interest rates. In bond lingo, leverage can provide duration equivalence. Because the two-year yield fell much more than the 30-year in these cycles, it would’ve been more advantageous to own a duration-equivalent two-year U.S. Treasury position than the 30-year U.S. Treasury.

It is counterintuitive, but U.S. Treasury bull markets begin when the economic weather is the sunniest. It happens when the unemployment rate is the lowest and consumer and industrial confidence the highest. By the time a recession is obvious, a good chunk of the move lower in rates will have taken place. Of course, there are no hard and fast rules to make money in finance, but to the extent that ”this time isn’t different,” now is the time to get ready for a large opportunity in the U.S Treasury market.

A table with the statistics and sources used in this article is available upon request.

Eric Hickman is president of Kessler Investment Advisors, an advisory firm located in Denver, Colorado specializing in U.S. Treasury bonds.

Read more articles by Eric Hickman