Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This is the second of my four-part empirical research into the fallacy of the random walk paradigm in investments. Part 1 focused on the failure of the random walk to depict the Dow Jones Industrial Average. In this article, I expand the study to include six diverse asset classes including large-caps (the S&P500), small-caps (the Russell 2000), emerging markets, gold, the dollar and the 10-year Treasury bond. Asset prices do not walk in tiny steps along an orderly bell curve, but often take giant leaps leaving chaotic turbulence behind.

What are the common features among seven widely diverse asset classes? Why are asset prices so hard to pin down by random walk or other analytical and descriptive models? What are the investment implications if asset returns do not fit the bell curves?

Part 3 will deal with its flaws in defining investment risk. Part 4 offers a new reward and risk framework alternative to the random walk paradigm. The new framework yields new insights on how to logically beat the S&P 500 total return.

Empirical evidence against the random walk model

In Part 1, I presented price return histograms of the Dow Jones Industrial Average from 1900 to 2016. In this paper, I extend the empirical research to six other assets. Detailed results are in the Appendix. Figure 1 summarizes the five-year return histograms (light blue bars) of seven asset classes – the DJIA from Part 1 and six other assets from the Appendix. No return histogram (light blue bar) has any resemblance to its corresponding random walk probability density functions PDF (dark blue curve). All random walk PDFs are unimodal (with a single central mean) with matching wings on both sides. All empirical distributions have multiple peaks with no central symmetry.

Common themes among different asset classes

1. None of the return histograms of the seven asset classes follows the random walk bell curve for periods longer than one day. The longer the return periods, the less bell-shaped they become. Real world prices do not follow a random walk.

2. Even for the one-day returns, all histograms show asymmetric fat tails. Random walk theorists have no explanation for them and treat them as anomalous statistical outliers.

3. All return distributions of time horizons beyond one year do not have a single mean and a definable variance. Random walk's mean-variance paradigm does not reflect reality.

4. Random walk's bell curve underestimates the probabilities of both large losses and gains beyond ± one standard deviation. This has dire consequences in risk management.

5. It is standard practice to scale returns and volatilities in different time horizons by the number of trading days and by the square root of trading days, respectively. Data show that neither return nor the volatility follows such scaling rules.

Why are asset prices so elusive for the theoreticians to capture?

1. Random walk is not the only model that fails to explain price behaviors. Power-laws, game theory, agent-based models, behavioral finance and adaptive market hypothesis are all incomplete theories at best. The rational beliefs equilibria model appears to have the potential for solving the asset-pricing puzzle but it is still too early to tell.

2. Why are prices so hard to pin down? The culprits are the agents involved. Unlike mindless pollens and particles that blindly obey physical laws, humans write their own rules, adapt to their own mistakes and adjust their actions to new encounters with a mix of unscripted rational and emotional responses.

3. Investors appraise prices from the perspective of an imagined future shaped by their past memories and current value judgments. These mental chain reactions transform their decision-making processes into highly complex systems. Our imagined future today can in turn create a new future that could then alter the current reality. The feedback loops continue in real time and exacerbate the already complex systems.

4. To model asset prices properly, economists must track all these nonlinear, multifaceted and interactive dynamics. By comparison, modeling the physical world is a trivial task.

What are the implications for investors?

1. There are many types of randomness described by different analytical probability density functions (PDFs). The bell curve is one of the most well behaved kinds. Figure 1 exhibits a wild form of randomness that does not fit any known PDF. Frank Knight called them "radical uncertainties". Donald Rumsfeld named them "unknown unknowns". Nassim Nicholas Taleb referred to them as "Black Swans".

2. Because asset prices do not follow the bell curve, it comes as no surprise why many random-walk based doctrines stopped working when prices plunged beyond one standard deviation. Markowitz's mean-covariance matrix, Sharpe's beta, Fama's factors and Black-Scholes' volatility neutrality all broke down during market crashes.

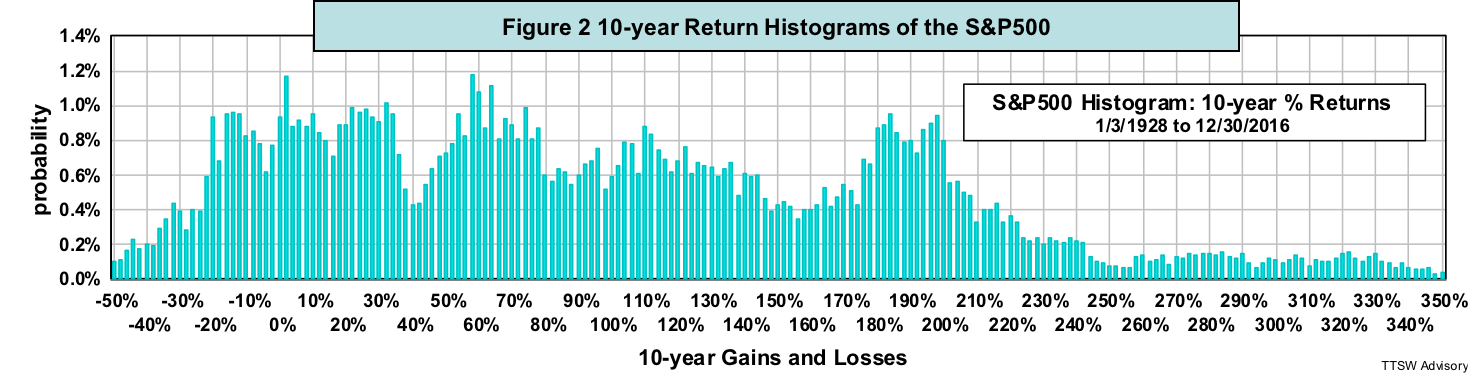

3. Because asset prices are radically random, investors should be skeptical of all market forecasts. Figure 2 shows the 10-year return histogram of the S&P 500 from 1928 to 2016. If you think that forecasting returns on a widely disperse bell curve is challenging, then mining for predictive patterns in the erratic randomness in figure 2 is a fool's errand because the probabilities of a +200% gain and a -20% loss are nearly the same.

4. Additionally, statistical flaws are common in many long-term forecasts. For example, analysts use overlapping data to compute the CAPE-based regression lines (here) and researchers gauge secular market cycles with sample sizes of less than a dozen (here). These forecasters not only try to predict something that is statistically unpredictable, they do so with incorrect math.

Concluding remarks

We live our lives every day without forecasting when the next big earthquakes will hit our hometowns. We mitigate quake risks by upgrading building codes and buying insurance.

Likewise, because asset prices exhibit radical randomness, predicting future returns is futile. Investors should focus on managing risk. To manage investment risk properly, however, we must first identify what risk truly is. Unfortunately, the academics view risk as volatility through a distorted random walk lens. In Part 3, I will point out the conceptual flaws and operational pitfalls of viewing volatility as risk. Mistaking risk as volatility has dire financial consequences for investors.

In Part 4, I will present a new framework for defining reward and risk as an alternative to the random walk paradigm. The new reward-risk framework offers investors a probabilistic path for beating the S&P500 total return – a blasphemy in the view of the efficient market orthodoxy. We win not by developing models with superior forecasting ability, but by beating Mr. Market at his own game. Stay tuned for details.

Theodore Wong graduated from MIT with a BSEE and MSEE degree and earned an MBA degree from Temple University. He served as general manager in several Fortune-500 companies that produced infrared sensors for satellite and military applications. After selling the hi-tech company that he started with a private equity firm, he launched TTSW Advisory, a consulting firm offering clients investment research services. For almost four decades, Ted has developed a true passion for studying the financial markets. He applies engineering design principles and statistical tools to achieve absolute investment returns by actively managing risk in both up and down markets. He can be reached at mailto:[email protected].

Appendix: Returns of six Asset Classes – Actual Histograms vs. Random Walk PDFs

Section (A) shows linear and logarithmic histograms of short-horizon returns of three equity assets (the S&P500, the Russell 2000 and emerging markets). Section (B) shows linear and logarithmic histograms of short-horizon returns of three alternative assets (gold, the dollar and the 10-year Treasury bond). Section © shows linear and logarithmic histograms of long-horizon returns of the S&P500, the Russell 2000 and emerging markets. Section (D) shows linear and logarithmic histograms of long-horizon returns of gold, the dollar and the 10-year Treasury bond. Data sources are FRED, Yahoo Finance and MetaStock.

(A) Short-horizon returns of large-caps, small-caps and the emerging markets

Figure A1 shows linear histograms of the returns in short-term horizons – daily, weekly, monthly and quarterly (top to bottom) across different equity styles – the S&P500 (big-caps), the Russell 2000 (small-caps) and emerging markets (left to right). Big-caps and small-caps (left and center) bear some resemblances to the random walk probability density functions (PDFs). However, for the emerging markets (right), fat tails are visible even in monthly and quarterly returns. Gaps between the data and the PDFs near the peaks are noticeable among all three assets.

Figure A2 displays the same data in logarithmic histograms. All log histograms exhibit fat tails on both sides of the peaks. The random walk PDFs fail to account for the high probabilities at both return extremes across all three assets.

(B) Short-horizon returns of gold, the dollar and the U.S. Treasury bond

Figure A3 shows three different alternatives – gold, the dollar and the 10-year Treasury bond (left to right) in linear histograms of short-horizon returns – daily, weekly, monthly and quarterly (top to bottom). Deviations from the random walk PDFs grow with increasing time horizons. Gold and the dollar have wider spreads than the random walk PDFs while the 10-year Treasury has tall spikes near the peaks.

Figure A4 displays the same data in a log scale. All histograms exhibit higher probabilities at both extremes than those predicted by the PDFs. Gold and bond are asymmetric and skewed to the right relative to the PDFs.

(C ) Long-horizon returns of large-caps, small-caps and the emerging markets

Figure A5 shows linear histograms of long-horizon returns – one year, five years and ten year (top to bottom) across three equity indices – the S&P500, the Russell 2000 and emerging markets (left to right). All charts show multiple peaks and wildly different spreads.

Figure A6 shows the same data in a log scale. Beyond one year, the data distributions show no central tendency and they are skewed to the right. Actual returns offer much better upside opportunities than what random walk predicts.

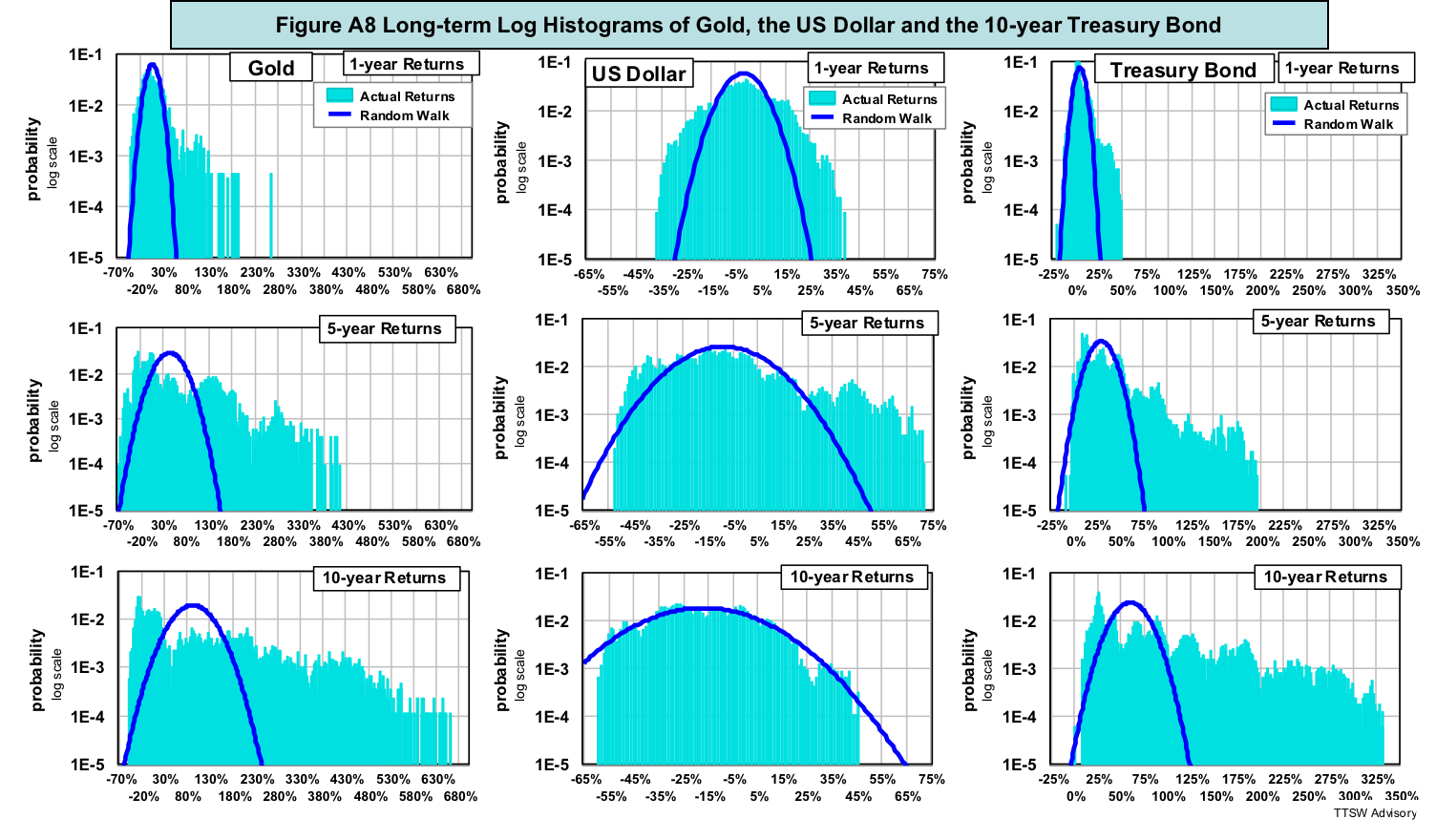

(D) Long-horizon returns of gold, the dollar and the U.S. Treasury bond

Figure A7 shows linear histograms of different long-horizon returns – one year, five years and ten year (top to bottom) across three alternatives – gold, the dollar and the 10-year Treasury bond (left to right). None of these plots resembles the random-walk bell curve.

Figure A8 shows log histograms of the same data in Figure A7. Most of the fat tails are skewed to the right versus the perfectly symmetric random walk PDFs.

Read more articles by Theodore Wong