Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Adaptive regime-based investment strategies should incorporate the financial cycle. Given the absurd decision by mainstream macroeconomics to ignore credit, money and the financial cycle, as I discussed in prior articles (here and here), it is not much of a surprise that they completely missed the oncoming crisis in 2008. In fact, twice since 2000, investors have suffered losses of 40% of their portfolios. My firm’s motto is: "Better not to lose in the first place."

In response to this shortfall, we have created an adaptive regime-based investment framework that generates multi-asset and equity-sector-rotation model portfolios. The investment objective of these model portfolios is to combine downside protection with upside participation. Many firms say they do this – but our process integrates macroeconomic and financial cycle risk.

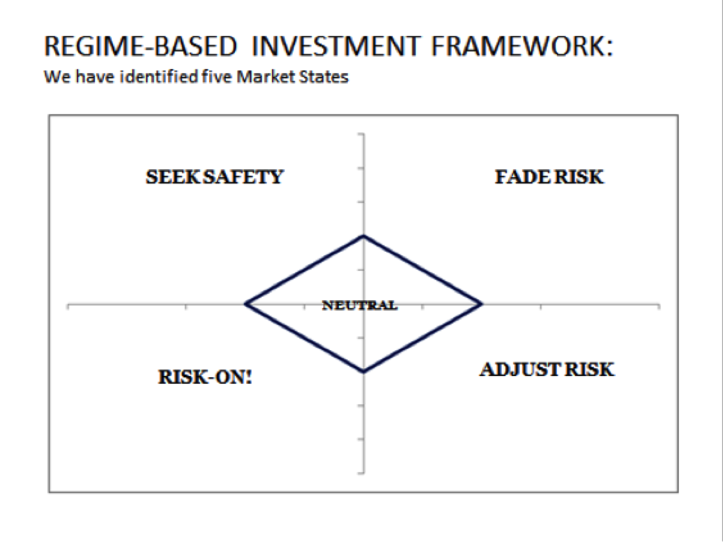

Our market state (or regime-based) investment framework utilizes more than a dozen variables that include measures of (1) market sentiment, (2) interest rates, (3) balance sheets, (4) real economic activity, and (5) asset prices. Once this information is distilled using a proprietary statistical process, we apply our adaptive regime-based framework, described below:

Our framework consists of five regimes. Each regime must offer different features. If the regimes are not sufficiently distinct from one another, performance will be inferior. For example, in our back tests, from September 2008 to February 2009, we were in a seeking safety regime and the portfolio was invested in safe assets, such as U.S. Treasury securities, cash and gold. Alternatively, in 2009-2010, we were invested in a risk-on market state, which included extensive exposure to risk, including equities, commodities and risky bonds, such as high-yield and emerging-market debt. Our process is intentionally designed to adapt to changes in market conditions and macro-financial risks.

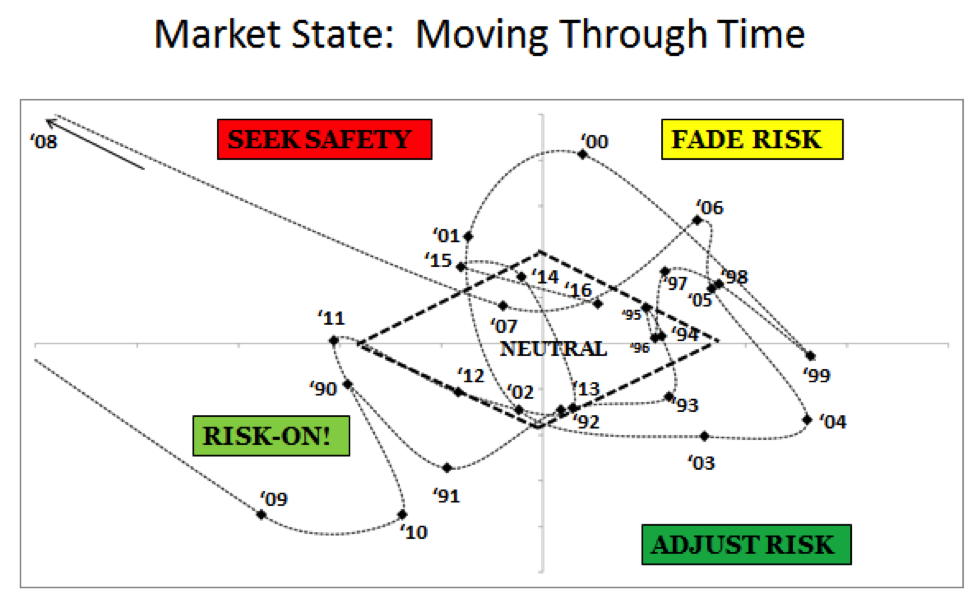

The movement in market states from one year-end to the next is provided in the figure below – we ran back tests from 1990 to 2016. Note especially that the portfolio at the end of 2008 was at an extreme (“off-the-chart”) seeking-safety market state, before recovering in 2009.

Current portfolio positions

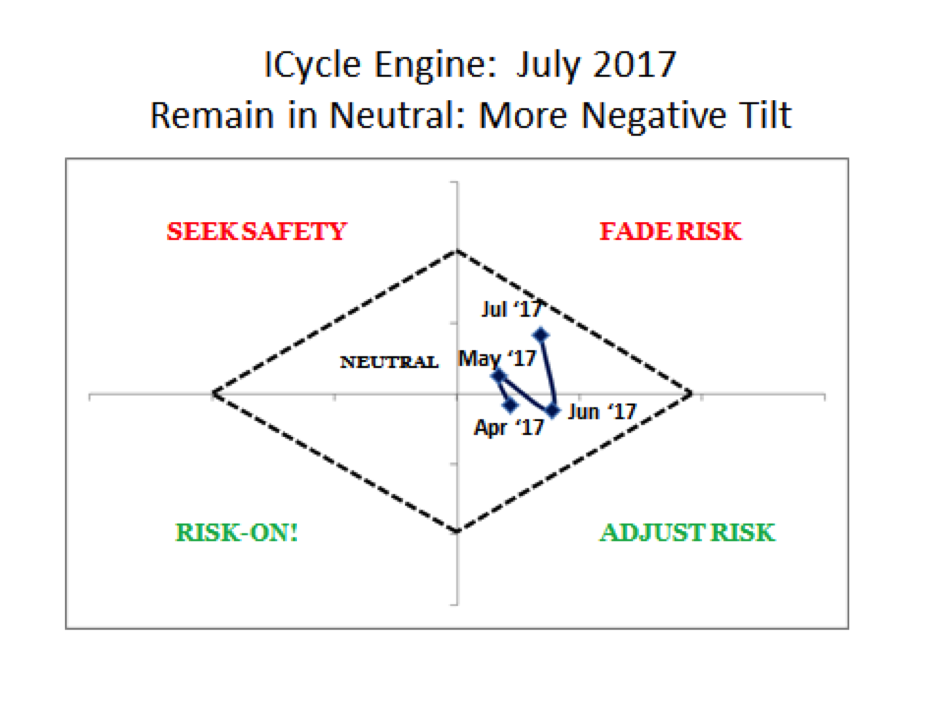

We run this process on a monthly basis. So where are the model portfolios currently positioned? Our framework has been in a neutral market state for more than one year. As the chart below describes, our portfolio recently shifted away from a more aggressive tilt toward the more bearish fade-risk market state (see below).

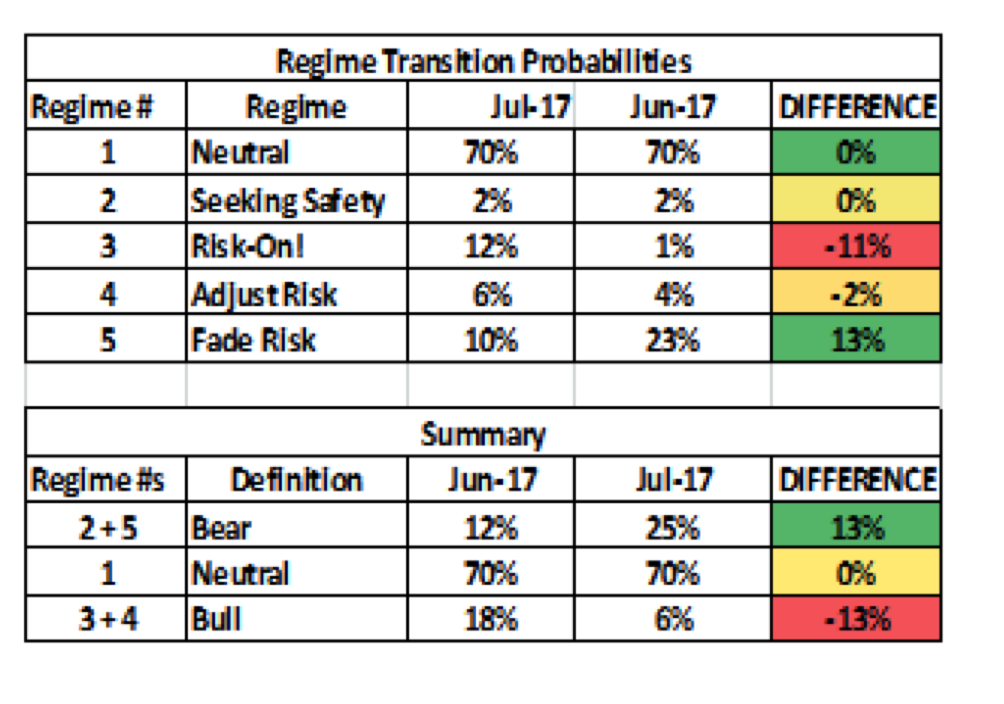

This investment framework incorporates regime transition probabilities (RTPs) for the next three months (see table below). As the tables below indicate, our positions became less aggressive in July than in June, given the shift toward the fade-risk market state. The probability that conditions will improve (see table below) declined from 18% in June to 6% in July and prospects for deterioration increased from 12% to 25%. And the probability that we will remain in a neutral market state over the next three months remained steady at 70%.

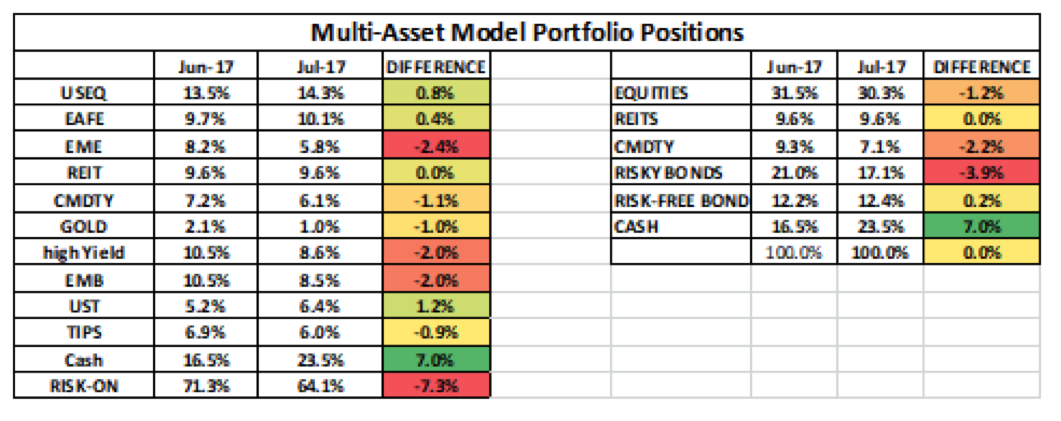

Implications for model portfolio positions: July 2017

Let’s examine the implications of the current market state for our two model (multi-asset and equity-sector-rotation) model portfolios. In July, our exposure to risky asset classes in our multi-asset model portfolio declined from 71% to 64% as our cash holdings increased by 7%. However, we continue to be exposed to risky assets (64%) and have not (as of yet) become risk-averse. We run our process at the end of each month and implement positions within the first few days of the following month. We implement these positions utilizing a simple rule that allocates to asset classes that have done well historically in the weighted combination of regimes that currently prevail (with some adjustments made for current versus historical valuations).

This approach offers a degree of diversification, as opposed to investing based on only one regime. In addition, our separate tail-risk indicator indicates that market turbulence is minimal – so we currently do not expect any severe losses over the next 30 days. Our biggest worry is the reversal of what we see as excessive market complacency, especially given that we are late-cycle, with rising interest rates, excessive private-sector indebtedness, over valued asset prices, etc.

Notation: USEQ = US Equities: EAFE = Europe, Australia and the Far East Equities: EME = Emerging Market Equities: REITS = Real Estate Investment Trusts, CMDTY = Goldman Sachs Commodity Index: GOLD = Gold: HY = High Yield Bonds: EMB = Emerging Market Bonds: UST = Short-Term U.S. Treasury Bonds TIPS = U.S. Treasury Inflation-Protected Bonds, Cash = 3-month T-Bills.

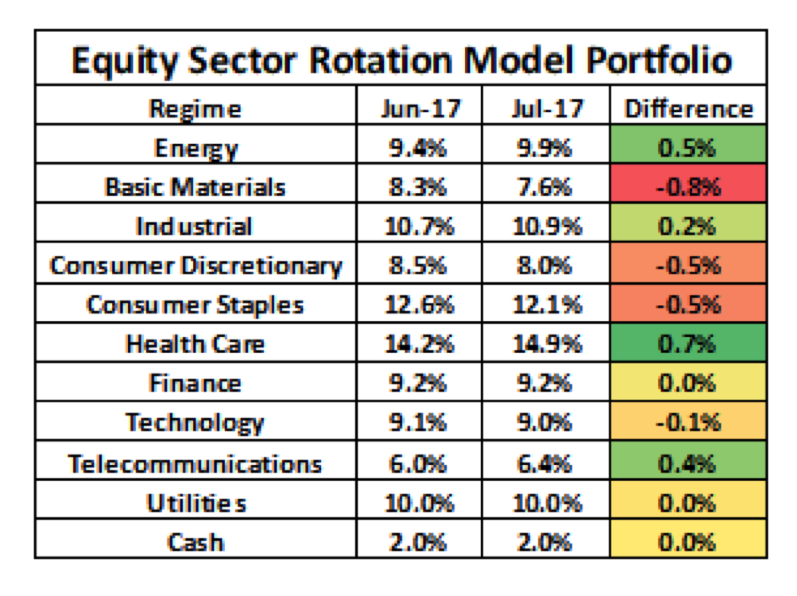

We also manage our own money in an equity-sector-rotation model portfolio that invests in 10 equity sectors. Importantly, the regime framework and the RTP are identical for both the multi-asset and equity-sector-rotation model portfolios. The only difference is the statistical attributes for each asset class and equity sector.

The equity-sector-rotation model portfolio allocation is in the table below. We do not adjust for valuations in this portfolio, so it tends to invest in cash only to the extent that there is a probability that we are in the seeking-safety market state (currently a 2% probability). In terms of the current allocation, positions have changed little from June to July.

Conclusion

We began running our own money in the multi-asset model portfolio in January 2016 and in the equity-sector-rotation model portfolio in May 2016. Performance to-date has exceeded our expectations. We are neither an investment firm nor an RIA. We create research around our investment framework and model portfolios that are of interest to individual investors, RIAs and investment organizations.

John Balder is a co-founder and CIO at Investment Cycle Engine, Inc. His experience combines more than 25 years of work building innovative investment strategies at firms that included GMO and SSgA. He previously worked with the U.S. Treasury and Federal Reserve Bank of New York after beginning his career with the House Banking Committee on Capitol Hill. His research has focused on the topic of financial stability and the real world relationship between economics and finance. More information is available at www.icycleengine.com.

The information in this presentation is solely intended for the purpose of information exchange. This is not a solicitation or offer to buy or sell any security. We do not manage money and this is not a solicitation to manage money. We are a research shop.

Read more articles by John M. Balder