Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This is part one of a two-part series on asset strategies that address financial instability.

Understanding the interplay between credit and finance is critical to recognizing the signs of economic distress. Yet this was precisely the failure that plagued economic analysis leading up to the financial crisis. Let’s take a look at the recent history of credit, finance and the underlying nature of market stability.

As the financial crisis approached in 2008, mainstream macroeconomic models missed the oncoming disaster, leaving the Queen of England to ask: “Why did no one see it coming?” Fortunately, several economists (e.g., Steve Keen, Michael Hudson, Claudio Borio, Wynne Godley and Dean Baker) did – based on approaches that incorporated credit and finance. Unfortunately, their views were not seriously considered by mainstream economists (which Andrew Haldane, chief economist with the Bank of England, has labeled a “methodological mono-culture”).

Curiously, the decision by mainstream economists to ignore finance and credit was based on the assumption (embedded in loanable funds theory) that credit cannot exceed already existing savings. This led to the conclusion that credit is “neutral” and has no effect on the real economy. A bank can make a loan of $100 only if it first has $100 in deposits. Money must first be saved before it can be deployed as credit. As if this relationship is entirely obvious, Paul Krugman wrote:

Think of it this way: when debt is rising, it’s not the economy as a whole borrowing more money. It is, rather, a case of less patient people – people who for whatever reason want to spend sooner rather than later – borrowing from more patient people.

The concept that deposits must precede loans is intuitive – almost like a law of nature. After all, we cannot lend $100 unless we have $100…..right? Credit must be neutral.

But is this perspective correct?

The answer to this important question was provided by no less an authority than the Bank of England (BOE). The answer is that, indeed, the mainstream view is wrong. In the BOE’s own words: “Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.” Banks create loans that become matching deposits.

For example, when a bank makes a loan for $100,000, it immediately credits the borrower with a deposit of $100,000. According to Richard Werner’s book, New Paradigm in Macroeconomics, this is how more than 95% of money is created in the U.S. and U.K. The notion from Economics 101 that the bank must first have deposits in hand before making a loan does not correspond with reality, according to the BOE. Today, credit and thus money can be created, ex nihilo (“out of nothing”). A bank need only make a loan – the deposit counterpart, given double-entry bookkeeping, is money, plain and simple.

So why does this matter? If the BOE’s claim is true, then credit and finance cannot be neutral! This certainly corresponds with our real-world intuition. The decision by mainstream macroeconomics to ignore credit makes no sense, especially given developments in financial markets over the past 30 years.

To understand credit, we will take a very quick tour of post-war financial history. For several decades after the end of the World War II, credit growth paralleled GDP growth as the world recovered from the Great Depression and the war. During this economic “Golden Age” (1945-1970), banks provided credit that fostered capital formation and the production of goods and services. Financial channels were subject to extensive regulation (interest rates were regulated, interstate banking was prohibited and Glass-Steagall limited combinations between banking and securities activities) and there were very few signs of financial instability.

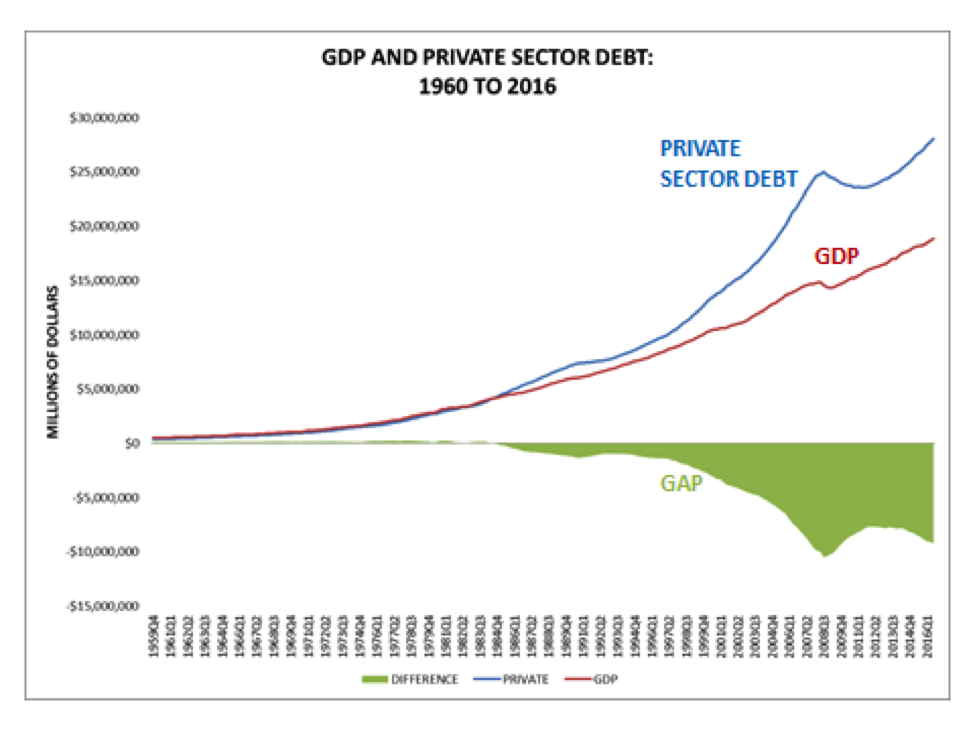

This era continued for 25 years before ending in the 1970s with the collapse of Bretton Woods and the rise in inflation. Beginning in the 1980s, restrictions on financial activities were gradually lifted. As markets were deregulated and liberalized, finance emerged as a much more important component of economic activity. In fact, private sector credit, having remained steady from 1945 to 1970, increased from 94% of GDP in 1980 to 165% in 2007 (see chart below). In addition, how that credit was used changed. More importantly, the vast majority of new credit was allocated to support asset purchases, mostly mortgages, and not productive activity.

This shift in economic activity awakened the financial cycle. Restrictions on finance were eased, prompting rapid credit growth and serial boom-bust cycles in real estate, equities and other assets. Banks and other financial firms were given tremendous latitude to determine where and how to allocate credit (and uniquely in the case of banks, money via creation of deposits), with significant consequences for financial stability and economic growth. More than 75% of the credit created from 1980 to 2007 was allocated to the financial circuit (primarily for purchases of assets and other financial activities, e.g., derivatives, securitization, etc.).

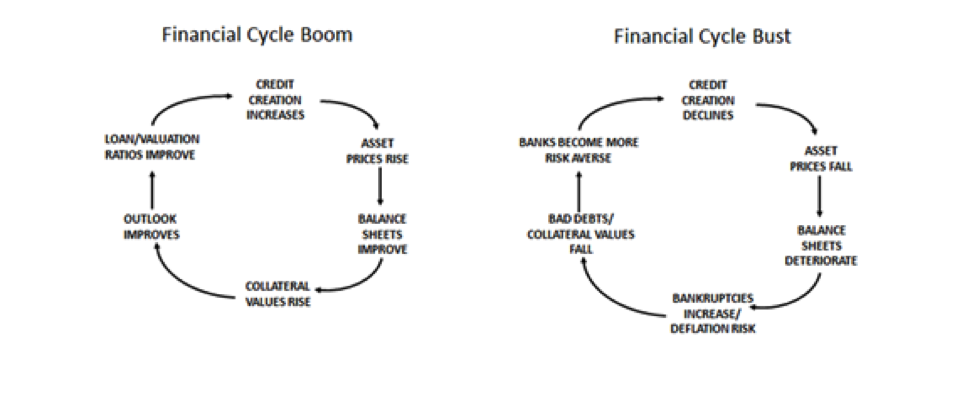

A stylized financial cycle tends to evolve as follows. In the early phase, private sector credit increases, but the rise is more than offset by the surge in asset prices (positive feedbacks from credit growth) and net worth. Throughout this phase, the balance sheets of the private sector appear robust (what Claudio Borio with the Bank for International Settlements calls the “paradox of financial stability”). This sets the stage for further expansion of credit (see left diagram below). This pattern persists until the growth in net worth and asset-price appreciation begins to slow relative to the pace of credit growth. Balance sheets adjust and investors may begin to sell assets to meet increasing liabilities. Credit creation declines, asset prices fall and balance sheets deteriorate (see right hand diagram below). Eventually the costs of servicing debt cut into wages and profits as bankruptcies increase. Aggregate demand then declines. The central bank responds by lowering short-term interest rates, etc., but its actions are belated and eventually a financial crisis and recession ensue.

Financial cycles have existed for centuries and what is, arguably, most remarkable about the postwar period was the “Golden Age” during which these cycles were absent. The revived financial cycle today introduces challenges to financial stability and economic growth that are compared with lending to the productive sector below:

- Lending to the productive circuit for capital formation and production of goods and services generates wages that facilitate consumption (in support of aggregate demand) and profits (that are used to pay off debt). Money is created when the loan is established and later destroyed when the loan is paid off. Loans for productive activity contribute directly to GDP growth with minimal implications for financial stability.

- Lending to the financial circuit (the FIRE sector) tends to boost asset prices, generating both realized and unrealized capital gains. These gains are not included in GDP growth (though wealth-effects support aggregate demand). Creation of credit for the financial circuit dominated economic activity from 1980 to 2007, and, unlike lending to the productive sector, these loans were not self-amortizing. As a consequence, they contributed less to GDP growth and increased periods of financial instability.

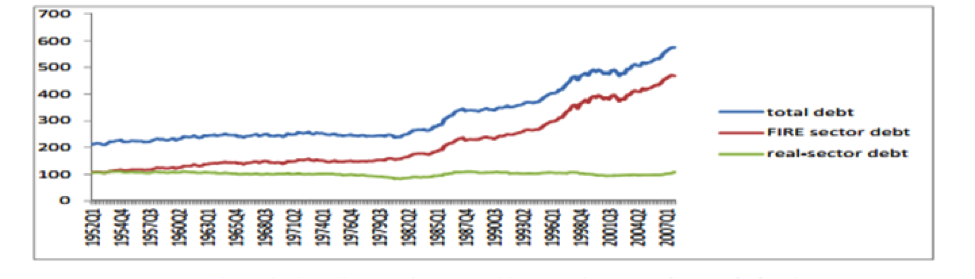

Dirk Bezemer has written a number of articles, including Finance and Growth: When Credit Helps, When it Hinders, examining lending to the productive versus financial circuits. He offers the chart below, which differentiates lending to the two circuits from 1952 to 2007 (using Federal Reserve flow of funds data). Lending to the real economy remained very stable over the 55-year period, ranging from 83% to 111%. Lending to the finance, insurance and real estate sector accelerated during the 1980s and remained robust up until the crisis in 2008. Bezemer notes that “total debt growth is equal to financial sector debt growth.”

Total US Bank Domestic Debt Stock (%GDP): 1952 - 2007

Source: Dirk Bezemer (2012) and Federal Reserve Flow of Funds

These structural changes help explain the combination of slower GDP growth and increased financial instability that has existed over the past three decades. Economic activity has tilted heavily toward lending to support asset prices. The challenge to economic growth today has less to do with private sector credit flows and more to do with the large stock of private sector credit (150% of GDP). Especially given its distribution, this is now a significant burden for many low- and moderate-income households. These households, absent this debt burden, would have a much higher propensity to consume than wealthier households, meaning that they could do more to support growth in aggregate demand (again, absent the debt). This debt burden will, no doubt, continue to hinder improved economic growth.

The financial cycle has returned with a vengeance over the past several decades, yet it was ignored by mainstream macroeconomic models. It is important to restore foundations for macroeconomics that incorporate the financial cycle.

Conclusion

A regime-based multi-asset investment framework can be designed that incorporates not only macroeconomic risk, but risks related to the financial cycle, as well. What is needed today is a framework that creates foundations for macroeconomics and that incorporate risks related to financial instability. I will have more to say about designing these strategies in a subsequent article.

John Balder is a co-founder and CIO at Investment Cycle Engine, Inc. His experience combines more than twenty-five years of work building innovative investment strategies at firms that include GMO and SSgA. He previously worked with the US Treasury and Federal Reserve Bank of New York after beginning his career with the House Banking Committee on Capitol Hill. His research has focused on the topic of financial stability and the real world relationship between economics and finance. More information is available at www.icycleengine.com.

Read more articles by John M. Balder