In part 1, I provided the case for time segmentation strategies used by their advocates, as well as how it fits into the spectrum of retirement-income approaches. In part 2, I examined the potential for time segmentation by considering three different ways to implement it. Now, we reach the heart of the matter: Is time segmentation a superior investment strategy for retirees relative to total-return investing? To examine this, we need to disentangle the effects of the dynamic asset allocation created by time segmentation from whether holding individual bonds to maturity helps to manage sequence-of-returns risk.

Whether time segmentation is a superior investing strategy is a controversial issue, though the general consensus is that time segmentation is not a uniquely better way to invest. Under some restrictive assumptions my findings confirm this consensus view.

To be a better investment strategy, time segmentation needs to reduce sequence risk relative to a total-return portfolio with the same asset allocation. The difficulty is how to compare two different strategies while controlling for asset allocation. A time segmentation strategy necessitates a dynamic (variable) asset allocation with a potentially higher average stock holding, and it cannot easily be compared to a total-return investing strategy with a static allocation.

Whether time segmentation is a better strategy depends on three interrelated issues:

- Because asset allocation is allowed to fluctuate, a time segmentation approach can have a very different asset allocation glide path than a total-return approach. Is this dynamic asset allocation acceptable to the retiree if he or she believes that a more static or slowly changing allocation is the right way to invest?

- Time segmentation approaches require varying degrees of effort to avoid selling stocks at inopportune times.

- Because time segmentation requires holding individual bonds to maturity, fixed income assets do not need to be sold at a loss to support retirement income.

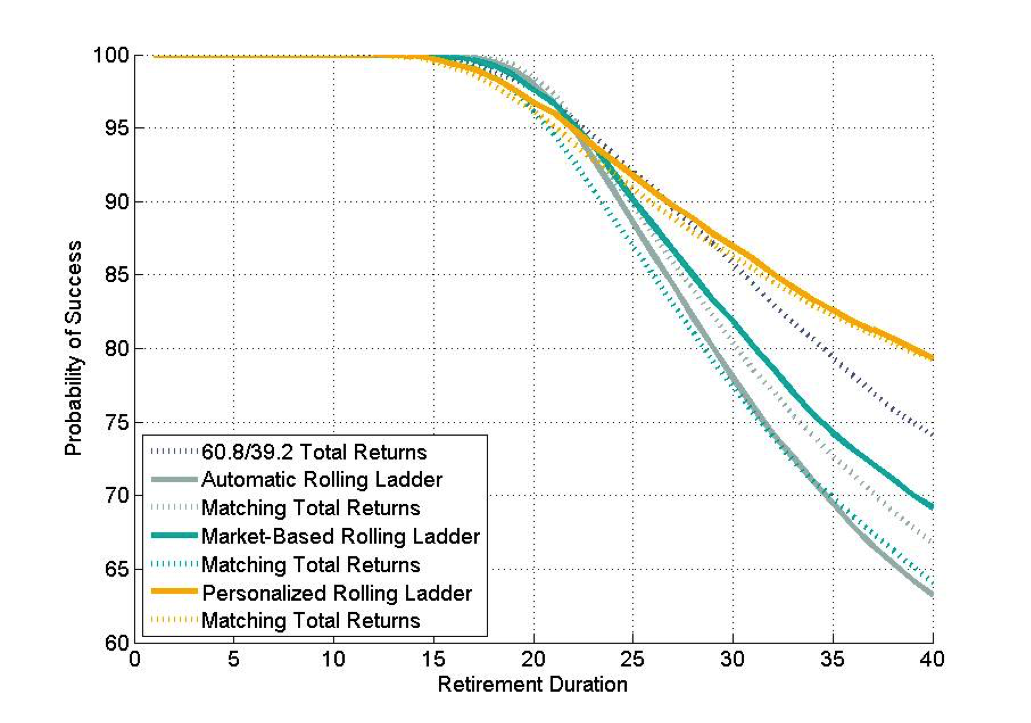

Figure 1 provides the ongoing probabilities of success for seven different strategies to support a retirement spending goal of $40,000 initially with 2% cost-of-living adjustments in subsequent years for up to 40 years of retirement. The client has $1 million available to support this goal. The analysis is based on 10,000 Monte Carlo simulations starting from today’s low bond yields with the capacity for rates to increase over time (this is the Monte Carlo simulation approach I have been using recently for a number of peer-reviewed research articles).

Three of the strategies are the time segmentation rolling ladder approaches previously described in part 2 with bond ladder lengths targeted at 10 years. Ladders are extended either automatically, just in years after positive market returns, or when remaining wealth exceeds the critical path level for that year of retirement.

Figure 1

Probability of success for different investment strategies in retirement

to support an initial $40,000 spending goal with a 2% COLA

The other four strategies are total-return investment portfolios with different asset allocations. The first of these maintains a fixed 60.8% stock allocation throughout retirement, which matches the initial stock allocation after constructing a 10-year bond ladder at the start of retirement. This strategy is included because retirees using total-return portfolios are more likely to maintain a relatively stable asset allocation in retirement. However, this strategy is not directly comparable to the time segmentation strategies because their asset allocations will be different in subsequent years.

The other three total-return strategies use dynamic asset allocations designed to match the asset allocation generated by the time segmentation strategies for each Monte Carlo simulation in each year of retirement. Though retirees would be unlikely to use such dynamic asset allocation strategies as a practical matter, especially since they would have no way to know what these allocations should be, these are important to include because they control for the effects of dynamic asset allocation. This allows us to isolate the specific role of the bond ladder portion of a time segmentation strategy as opposed to holding an equivalent amount of bond funds.

We learn a lot from the exhibit. First, after about 27 years of retirement, the personalized time segmentation approach with the critical path offers the highest probabilities of success. However, the total-return approach with a matching asset allocation provides almost identical success rates. This suggests that the success of the time segmentation strategy is due to its generally more aggressive asset allocation, rather than the bond ladder.

Moving down, a fixed-asset-allocation total-return approach shows up next in terms of its ability to support retirement income. This is important to note, since this strategy is more indicative of what a retiree would use instead of a time segmentation approach.

Next we observe the market-based time segmentation approach. While it underperforms relative to the fixed-asset-allocation total-return case, the time segmentation version does noticeably better than its total-return counterpart with the same asset allocation. This suggests that the market-based approach is reducing sequence risk relative to an equivalent total-return portfolio. It avoids selling stocks after a stock market downturn.

Finally, the automatic rolling-ladder- time-segmentation approach performs noticeably worse than other strategies, including a total-return strategy with a matching dynamic asset allocation. The reason is that this strategy drains the growth portfolio more quickly, reduces the stock allocation, and increases the sequence-of-returns risk as more pressure is placed on distributions for the growth portfolio.

We can understand this by considering distribution rates for the second year of retirement while including a simple assumption that the market return in the first year of retirement was sufficient to precisely offset the first-year distribution, and that interest rates do not change from their initial 2.45% level in year two. These simplifying assumptions illustrate the point without a loss of generality. For the total-return portfolio, the distribution in year two after the 2% COLA is $40,800. This represents 4.08% from a $1 million portfolio. Meanwhile, for the time segmentation strategy, after building the bond ladder the growth portfolio has $608,000 left. The distribution from this portfolio is the amount needed to support spending in year 11. This is $40,000 with 11 years of 2% COLAs, then discounted for 10 years at the 2.45% discount rate. This is $39,043, which reflects a much higher 6.42% distribution rate from the remaining growth portfolio. The automatic rolling ladder approach does not provide discretion to avoid extending the bond ladder, and for the example illustrated here it creates too much distribution pressure on the remaining growth portfolio to be an effective strategy. It actually enhances sequence-of-returns risk.

The total-return approach with matching dynamic asset allocation performs a bit better, since it does not increase the distribution rate as quickly, but this asset allocation cannot support spending as well as a fixed 60.8% stock allocation. When the portfolio is endangered, the strategy pushes the stock allocation down, which effectively locks failure into place for a greater number of the simulated market scenarios.

The bottom line

It is difficult to argue that time segmentation by itself provides a superior investing strategy for retirees. The personalized time segmentation strategy does outperform. That is due to the dynamic asset allocation that results from coupling the critical path to a time segmentation strategy to create a personalized rolling ladder.

However, the results are nearly equivalent to a total-return approach with the same dynamic asset allocation. That suggests that the more aggressive asset allocation is primarily responsible for the overperformance. Time segmentation could be recommended for retirees who would otherwise reject a more aggressive total-return approach, but are comfortable with a more aggressive allocation when the bond ladder is implemented.

Of course, in some cases with this strategy, the bond ladder depletes and the retiree may be left with 100% stocks in the latter part of retirement (though heirs may be fine with that). The strategy is tough to recommend for investors who are unpersuaded with this argument and the empirical tests that confirm it.

Recommendations for time segmentation should be based as strongly on the behavioral aspects of the strategy as its performance. For retirees who may struggle to stay the course with a total-return investing approach, the appealing logic of time segmentation could help them to maintain better investment discipline in retirement. While time segmentation may not provide a superior investing strategy when compared to a total-return approach with matching dynamic asset allocation, it is a viable strategy deserving of its place in the retirement income toolkit. Retirees must understand, however, its implementation will mean dynamic asset allocations and that a clear rule must be designed and followed for when to extend the bond ladder.

Acknowledgements: I am grateful for helpful feedback on earlier drafts of these columns from Stephen J. Huxley and J. Brent Burns of Asset Dedication.

Wade D. Pfau, Ph.D., CFA, is a professor of retirement income in the Ph.D. program in financial services and retirement planning at The American College in Bryn Mawr, PA. He is also a principal and director at McLean Asset Management and the Chief Planning Scientist for inStream Solutions. He actively blogs at RetirementResearcher.com. See his Google+ profile for more information.

Read more articles by Wade D. Pfau