The Financial Planning Association (FPA) divides retirement income strategies into three categories: systematic withdrawals, time-based segmentation and essential-versus-discretionary income. Time-based segmentation provides a middle ground between the two extremes represented by systematic withdrawals (relying on a total-return investment portfolio for all distributions) and essential-versus-discretionary (using insurance-based products to implement a lifetime-income floor before considering investments). In occupying this middle ground, time segmentation is wildly popular in practice and it goes by many different names. But it is also the least studied retirement income approach. Whether time segmentation is a superior investing approach for retirement income has led to many heated debates. I anticipate a lengthy discussion will show up at APViewpoint about these issues.

This column is the first of a three-part series on time segmentation. In this first column, I will provide the case for time segmentation strategies provided by their advocates, as well as how it fits into the spectrum of retirement-income approaches. Part 2 will then demonstrate how time segmentation can work in practice by considering three different approaches for managing the strategy over a long retirement. Part 3 will answer the question of whether time segmentation is a superior investing strategy for retirees.

Introducing time segmentation

Time segmentation serves as a middle ground for retirement approaches. It differs from systematic withdrawal strategies in that fixed-income assets are held to maturity to fund future retiree expenses over the short and medium term. A growth portfolio is also built with more volatile assets having higher expected returns, to be deployed to cover expenses in the more distant future. This is not total-return investing, since different investing strategies are used to cover different time horizons.

Time segmentation also differs from an essential-versus-discretionary strategy because it does not build a lifetime income floor. Rather, there is an income front-end with contractual protections. The assumption is that people have not saved enough to fund their entire lifetime of spending. Importantly, time segmentation also accounts for the fact that spending needs may change, and this requires flexibility and the avoidance of irreversible decisions.

Defining time segmentation as it is used in practice is challenging, but I must do that in order to test the approach quantitatively. Time segmentation, also known as bucketing, is used by countless financial advisors, each of whom defines their process in a unique way. Differences can be found with regard to the number of time segments and their respective lengths, the choice of asset classes used within each segment, whether individual bonds are used in place of bond funds, the degree to which the overall asset allocation is allowed to change over time and how and when the different segments are further extended as time passes. These issues may not always be addressed, and critics of time segmentation wonder if there is really a “there there,” as Jonathan Guyton questioned in a 2014 Journal of Financial Planning column.

At its core, though, time segmentation involves investing differently for retirement spending goals falling at different points in retirement. Fixed income assets with greater security are generally reserved for earlier retirement expenses, and higher volatility investments with greater growth potential are employed to support later retirement expenses.

The most lucid explanation of time segmentation was provided in the 2004 book, Asset Dedication: How to Grow Wealthy with the Next Generation of Asset Allocation, by Stephen J. Huxley and J. Brent Burns, both of whom are active at APViewpoint. However, those authors may not necessarily be comfortable with the label of “time segmentation” for what they describe, showing just how difficult the issue of nomenclature can be. Nonetheless, their description serves as a motivation for this discussion, even though when I model different strategies I do not incorporate the same degree of sophistication as they suggest for their personalized strategy.

Accurately discussing and simulating time segmentation requires defining it in core terms without some of the bells and whistles that occasionally get included. For example, I will consider two time segments rather than six, will use individual bonds for the upfront time segment and a large-capitalization stock fund for the growth segment meant to cover later expenses, and will include straightforward automated rules to guide how the upfront time segment is extended over time with a rolling bond ladder. This latter point is important, because many versions of time segmentation used in practice treat the process of extending earlier time segments in an ad hoc fashion, or may even neglect it.

Defining asset allocation within time segmentation

Building bond ladders to fund retirement spending needs is a relatively understudied topic within the retirement income world. The best source for education about the logic of holding individual bonds is provided by Huxley and Burns. With traditional bond ladders, one reinvests assets as they mature into new bonds to extend the ladder. With retirement income, however, income and principal from maturing bonds is spent rather than reinvested. Extending a retirement income bond ladder requires drawing from a separate pool of assets to build out new rungs.

With time segmentation, asset allocation varies in a dynamic manner because no effort is made to maintain a fixed ratio of stocks and bonds. Rather, bond holdings are based on the cost of maintaining a bond ladder with the desired length and income level. Stock holdings consist of what is left over after building and maintaining the bond ladder. An initial stock allocation of 50% could easily rise above 90% if the growth portfolio performs well, and it could fall to 0% with poor growth forcing all available assets to be used to maintain a bond ladder until it depletes as well.

To the extent that time segmentation does not call for portions of a bond ladder to be sold in order to rebalance funds into the growth portfolio, it can only have one possible direction for portfolio rebalancing: extend the bond ladder with funds from the growth portfolio. Time segmentation provides a way to reallocate funds from stocks to bonds, by moving assets from the growth portfolio to the bond ladder. It does not provide a mechanism to move in the other direction. The only mechanism available to increase stock allocation is to avoid extending the bond ladder over time; maturing bonds are spent and are not replaced.

A volatile asset allocation may make retirees uncomfortable. Nonetheless, Huxley and Burns are critical of traditional asset allocation, because other than saying that risk tolerant individuals can hold more stocks, there is no clear way to decide on the appropriate allocation between stocks and bonds. They reject the utility of commonly used risk-tolerance questionnaires. With asset allocation, they argue, bond funds are treated as “stocks-lite,” in which a volatile bond mutual fund is held that still fluctuates in value, but just to a lesser degree than stocks. Huxley and Burns criticize retirement portfolio bond mutual funds for behaving as equities but with lower returns and volatility. Given bond funds’ volatility, they say it is hard to explain to retirees why their asset allocation should be 60/40 rather than 50/50 or 70/30. The traditional asset-allocation approach is grounded in a single-period framework that abstracts from an investor’s goal to build a nest egg that will allow for desired spending amounts for as long as retirement lasts. Risk, according to Huxley and Burns, is not being able to meet retirement goals, rather than simple measures of portfolio volatility.

The time segmentation approach to asset allocation leads to a much more dynamic asset allocation over time. The bond allocation is determined by the cost of building the bond ladder, rather than trying to keep the overall portfolio at a fixed percentage of bonds. Bonds provide the cash flows to match assets to liabilities. Stocks, meanwhile, represent whatever is left after the bond ladder is created and updated. Goals and performance drive the asset allocation. If stocks perform sufficiently well, the stock allocation may increase over time. If stocks do not perform well, the stock allocation could creep toward 0% as the cost of maintaining the bond ladder takes up an increasing percentage of the remaining portfolio value.

A retiree would understand that his or her bond allocation is 40%, for example, if this is the amount needed to lock in spending goals for a targeted eight-year horizon. The important discussion becomes: How much spending and for how long is one comfortable locking into place fixed-income assets? Conservative investors would build a longer bond ladder in order to lock in more spending. Asset allocation is determined by goals and investment performance, rather than questionnaires or other tools that attempt to measure an investor’s tolerance for portfolio volatility and potential losses.

The bond allocation is the portion of assets required to build the bond ladder with sufficient income and the desired length. More conservative behavior is reflected with a longer upfront bond ladder, which implies a higher allocation to bonds. The fundamental tradeoff in choosing the bond ladder length is the degree of certainty versus growth. A longer bond ladder length creates greater income security in retirement as more years of spending are covered by holding more individual bonds to maturity. A shorter bond ladder allows more assets to remain in the growth portfolio; if growth is realized then the portfolio can support a longer retirement.

If a client’s desired withdrawal rate is greater than what the bond yield curve can support, one can’t build a bond ladder to meet lifetime spending needs. Bonds would be a drag on the portfolio as there will be no chance to get the returns needed to meet lifetime spending goals. If annuities are not in the cards, one must either cut back on spending or add more volatile assets offering a greater potential investment return. Some retirees may rely on the assumption of future portfolio growth to justify spending more today than bonds could otherwise support. But the hope for greater portfolio growth could backfire, ultimately reducing retirement sustainability relative to what a longer bond ladder could have supported.

The upshot is that dynamic asset allocation is not a concern. The portion of assets needed to build the desired bond ladder as the percentage of available assets determines the initial bond allocation. Retirees can focus on this bond ladder and not worry about their overall asset allocation. If this percentage fluctuates wildly and unpredictably, so be it. Efforts to maintain a less volatile asset allocation would require letting the bond ladder length fluctuate more dramatically.

Increasing equity exposure decreases the guarantee that the plan will work, but provides a chance to meet spending goals that extend beyond what the yield curve can support. By building an income floor at the front end of the portfolio, one has assets dedicated to meeting their spending needs over the short-term horizon, and then the remainder of the portfolio is invested for long-term growth. Assets are dedicated to the purpose they are best suited for: bonds generate predictable cash flows and stocks provide less predictability but more growth potential.

Time segmentation is a probability-based approach

As for the debate between the probability-based and safety-first schools of thought for retirement income planning, I view time segmentation as a hybrid that falls closer to the former. Time segmentation generally relies on the idea of “stocks for the long-run,” as there is a degree of comfort that the growth portfolio will provide sufficient returns to maintain retirement sustainability. According to its advocates, the long-run growth potential of stocks can be expected to materialize in time to keep the bond ladder adequately extended.

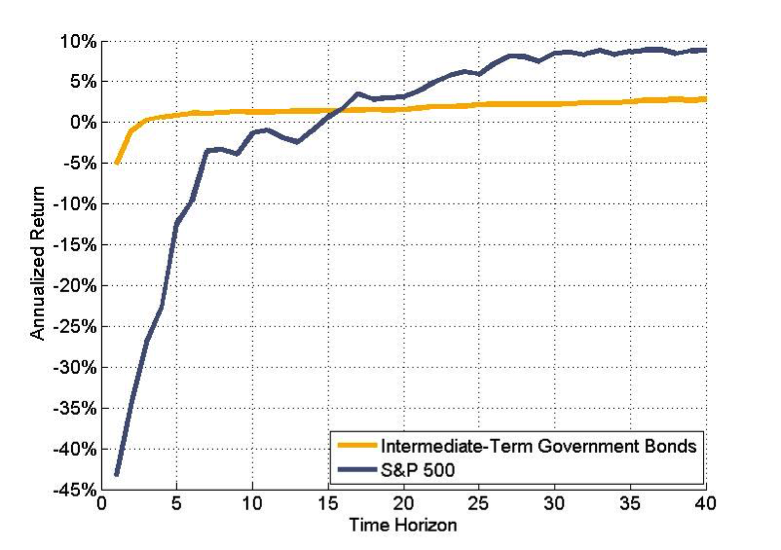

To understand this probability-based point of view, Figure 1 follows the ideas of Huxley and Burns by plotting the historical worst-case annualized nominal returns for large-capitalization U.S. stocks and intermediate-term U.S. government bonds since 1926. Over shorter holding periods, bonds were less exposed to downside risks. Over one year, for instance, the worst case for bonds was a 5.1% drop, while stocks fell by 43.3% in their worst year. Over any historical three-year period, bonds provided a positive annualized return. It took 15 years before stocks historically were always able to provide a positive return. For holding periods of at least 17 years, the historical worst-case annualized performance for stocks exceeds that for bonds. Over 20-year periods, for instance, stocks experienced a worst-case 3.1% annualized return, compared to 1.6% for bonds. For 30-year periods, the worst-case for stocks was 8.5%, compared to 2.2% for bonds. And for 40-year periods, stocks’ worst performance was an 8.9% annualized return, compared to 2.8% for bonds. For historical 40-year periods, even the best case for bonds (8.1%) could not beat the worst case for stocks.

Because probability-based advocates have confidence that the historical record provides sufficient predictability for the future, this explains the view that stocks should be the primary asset to cover retirement expenses over the longer term.

Figure 1

Worst-Case Annualized Nominal Returns for Different Holding Periods

S&P500 and Intermediate-Term Government Bonds, 1926-2016

With this optimistic view about stocks in the long-run, the objective is to maintain a high stock allocation. Prior to constructing a retirement-income bond ladder, the argument goes, the stock allocation should be 100%. Only enough is taken from the growth portfolio to construct the desired bond ladder. Someone with greater risk aversion can lock-in a longer spending stream, which devotes more to bonds, and then allow the remaining stocks to compound for a longer time before needing to be sold. To the extent that this provides an improvement over traditional asset allocation (a total returns portfolio), it helps to devote as much as possible to growth assets, and it helps to avoid having to sell stocks after momentary drops, because nothing will need to be sold until it is necessary to lock-in more spending. Only the minimal amount needed to lock-in spending should go to specific individual bonds, and the rest should be earmarked for growth.

Behavioral benefits of time segmentation

Advocates of time segmentation argue that it can lead to better retiree behavior because it is more easily understood. Time segmentation can be more intuitive than the blended approach of the total-return portfolio as it’s easier for people to understand that certain assets are to be used for different time horizons in retirement. It is a form of mental accounting.

With traditional asset allocation, different asset classes are mixed into a single portfolio, and individuals experience difficulty understanding why they have a particular asset allocation or what the different parts of their portfolio are aiming to do. Bonds are used as a way to dampen volatility, which leaves them behaving as sluggish stocks.

With this lack of understanding of asset allocation, this could make a retiree vulnerable to panic and stock selling after a market decline. The argument is that when retirees instead have a front-end bond ladder, they know there is time for stocks to recover before they need to be sold. This provides the courage to leave stocks alone and to focus on a longer-term investing approach. To the extent that this helps a retiree to stay the course and to avoid panic-driven selling of growth assets after a market decline, this is a strong justification for time segmentation even if it is not necessarily a superior investing strategy for a fully rational investor.

Time segmentation and sequence of returns risk

A selling point for time segmentation is that it avoids short-term sequence of returns risk as the volatile growth assets will not need to be sold immediately after a market drop in order to support retirement spending. The bond ladder does not have to be replenished every year. The retiree can wait for markets to recover before selling stocks in order to extend the bond ladder.

However, this point is controversial. The bond ladder must be extended at some point. That could trigger sequence risk. We must determine whether dynamic asset allocation is what is responsible for time-segmentation outcomes. But first, it is worthwhile to explore sequence risk for individual bonds and bond funds a bit more, since this point is often confused during retirement.

The value of the bond ladder fluctuates over time with changing interest rates, but this is immaterial to the success of the plan if the bonds are held to maturity. At maturity they pay the full principal, and earlier unrealized gains or losses are immaterial. Investors financing a retirement goal can happily ignore the fluctuating value of their individual bonds, knowing that the desired cash flows will be provided from bond coupon payments and the return of principal at maturity. When laddered bonds are held to maturity, cash flows are known and there is no realized interest-rate risk. In fact, rising interest rates could even help with issues such as reducing the overall IRS required minimum distribution (RMD) amounts for bonds in tax-deferred accounts.

With a bond fund, the concept of duration implies an investor is made whole after a rate increase once a time period matching the fund’s duration has passed, because that investor is able to re-investment coupon payments at higher interest rates to offset the capital losses on bonds. However, that conclusion assumes the portfolio is not funding a spending goal. If those coupons are being used for spending and if some shares of the bond fund are sold to cover spending, then the bond portfolio will not be able to recover through its ability to reinvest cash flows at a new higher interest rate. Portfolio returns would need to be even higher to offset the loss in ability to fully reinvest funds at higher rates. This makes duration matching for household investors using constant-duration bond funds much more difficult in practice. A few commercial bond fund solutions exist.

Time segmentation does provide a practical way for retirees to duration-match their spending goals. But the idea that time segmentation reduces sequence risk is less clear. Time segmentation is a probability-based approach in that its advocates are confident that sufficient upside growth will take place before growth assets need to be sold to support spending. The safety-first side reminds us that there is no guarantee this will actually happen. Growth assets may still have to be sold at a loss, depending on when it becomes necessary to rebalance into bonds. The bond ladder may be depleted before the growth portfolio has recovered sufficiently. Sequence risk may still materialize if assets are sold at a loss. We need to investigate empirically the importance of this matter, which I will do in the subsequent articles.

The bottom line

As this is the first of a three-part series, we do not have any firm conclusions yet. I have laid out the case and framework for thinking about time segmentation as a retirement income strategy. Next, Part 2 will formalize three different rules for how to implement time segmentation in practice. Part 3 will then compare time segmentation approaches to total-return investing strategies to determine whether it is a superior investing strategy.

Acknowledgements: I am grateful for helpful feedback on earlier drafts of these columns from Stephen J. Huxley and J. Brent Burns of Asset Dedication.

Wade D. Pfau, Ph.D., CFA, is a professor of retirement income in the Ph.D. program in financial services and retirement planning at The American College in Bryn Mawr, PA. He is also a principal and director at McLean Asset Management and the Chief Planning Scientist for inStream Solutions. He actively blogs at RetirementResearcher.com. See his Google+ profile for more information.

Read more articles by Wade D. Pfau