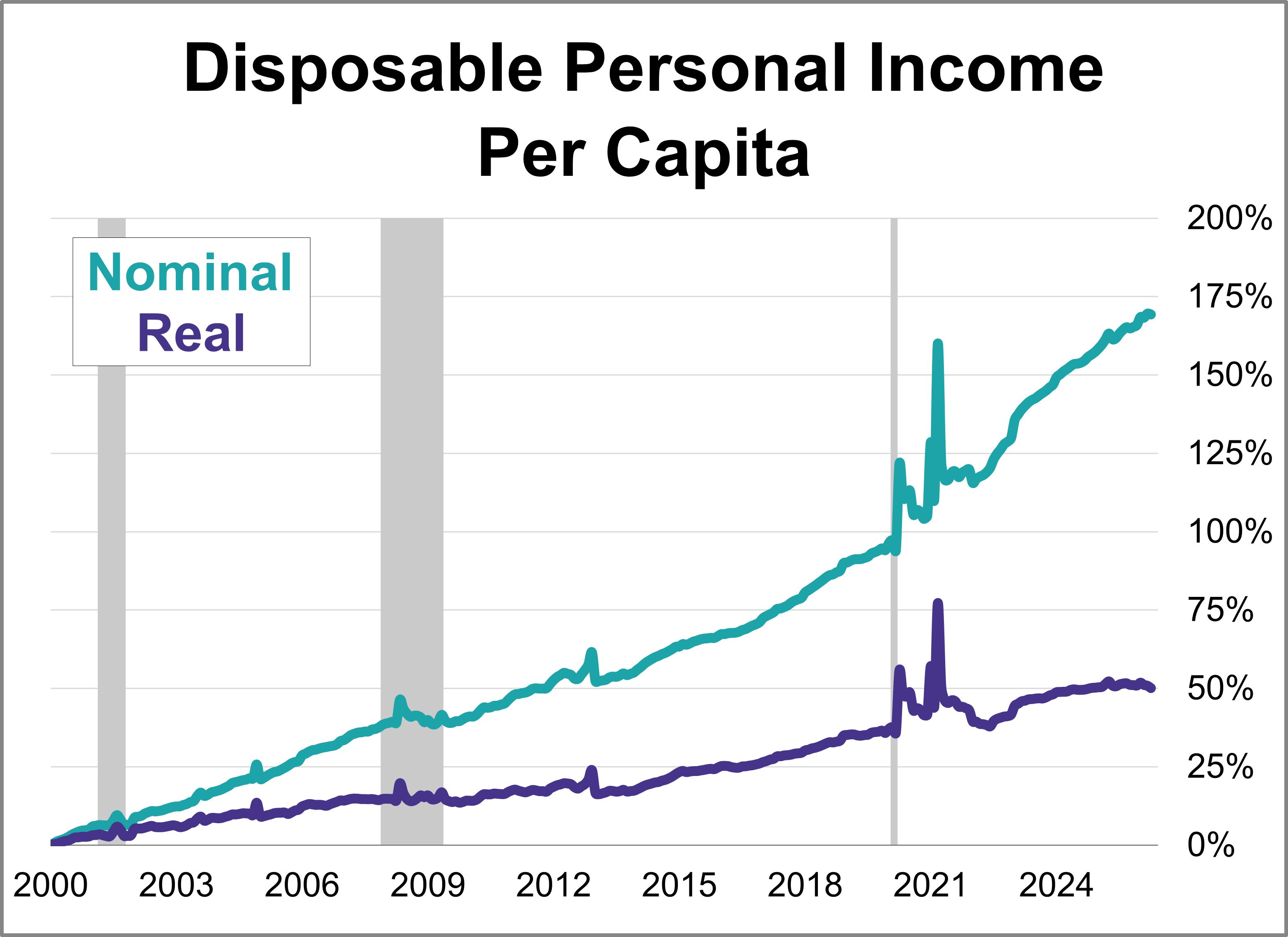

With the release of April's report on personal incomes and outlays, we can now take a closer look at "real" disposable personal income per capita. To two decimal places, disposable income per capita was up down 0.10% month-over-month. But when adjusted for inflation, real disposable income per capita was down 0.50%.

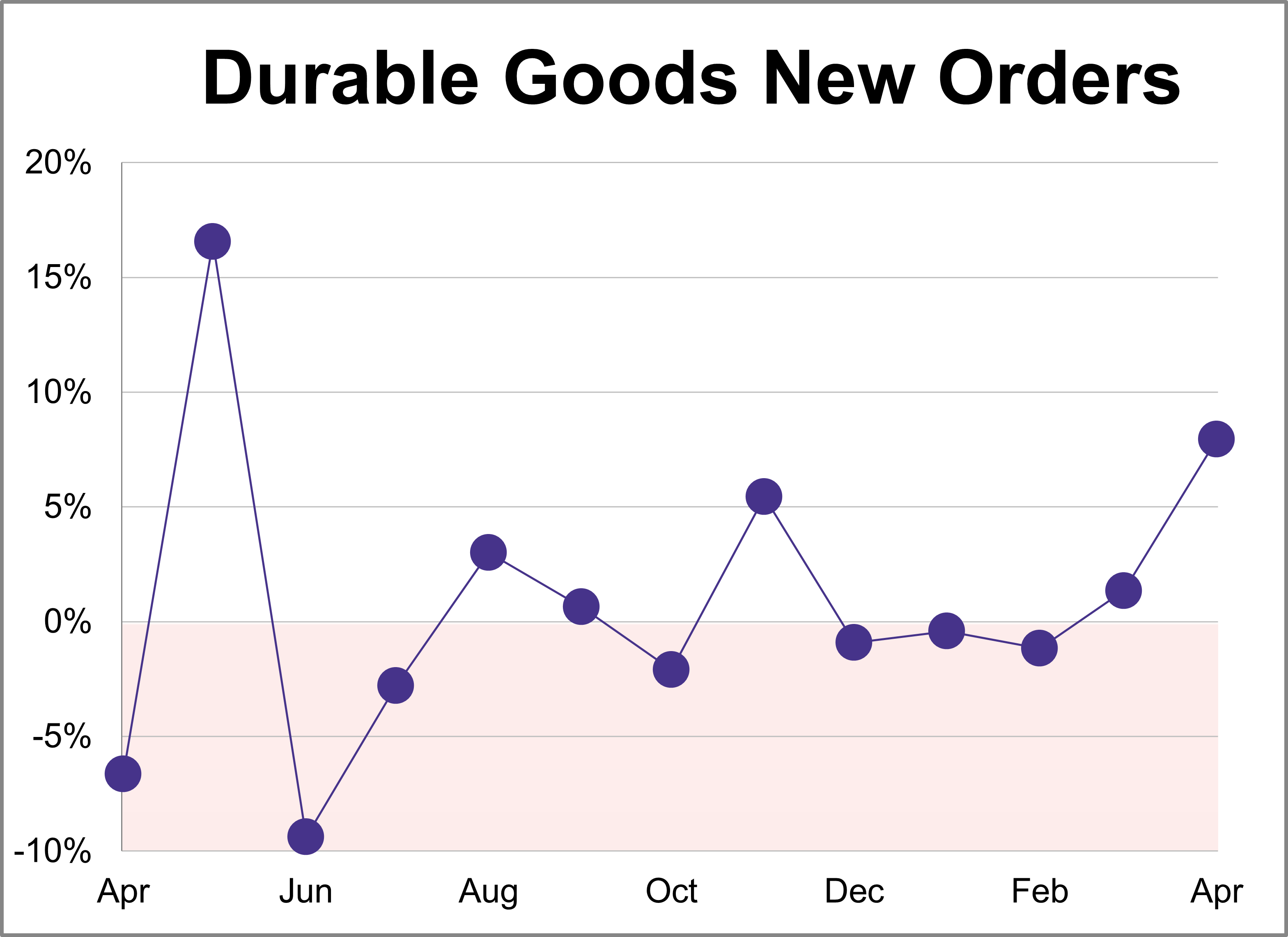

New orders for manufactured durable goods jumped 7.9% in April to $345.96B, almost twice as much as the projected 4.0% monthly growth.

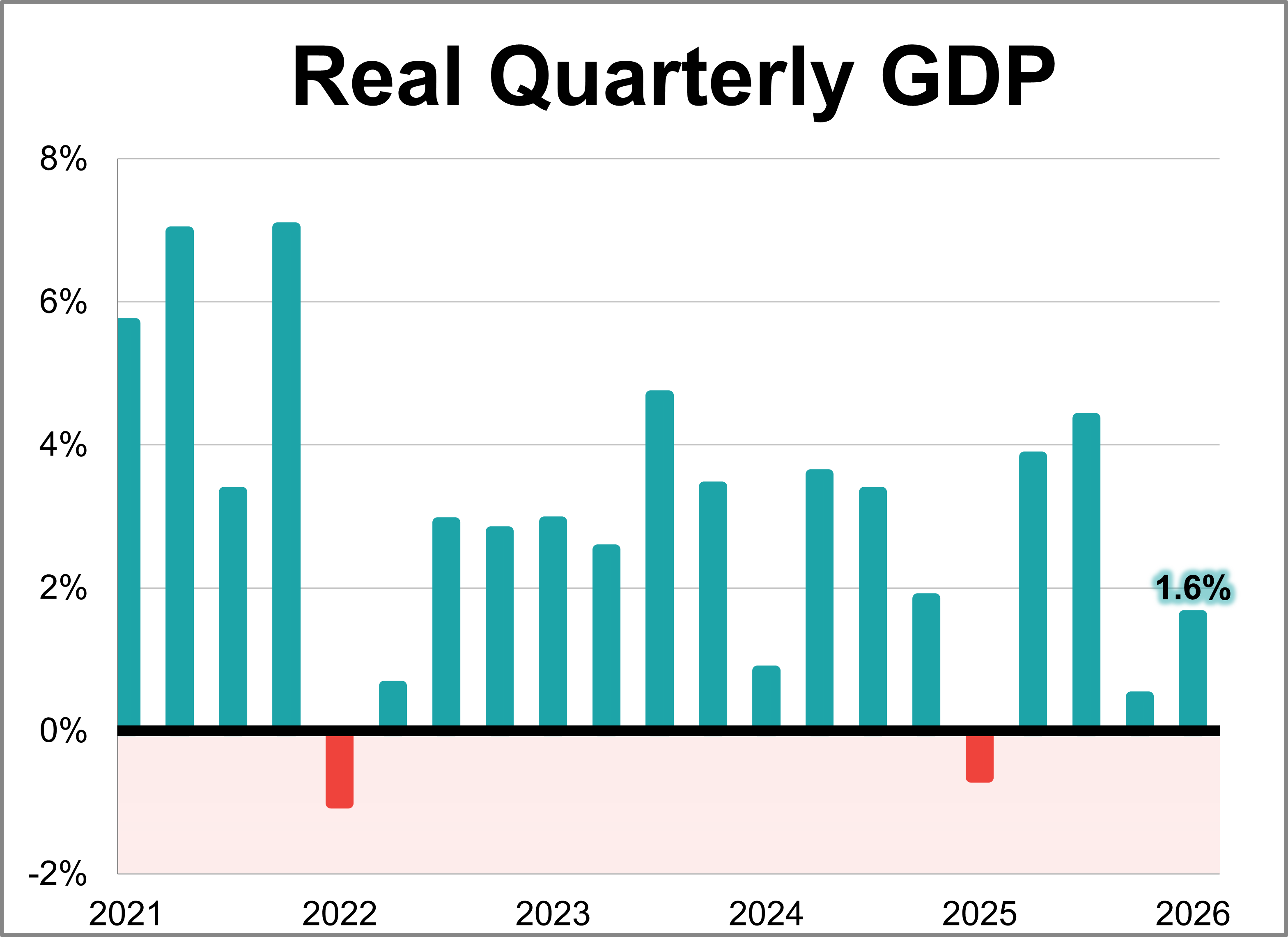

U.S. economic growth rebounded at the beginning of 2026, according to the BEA’s latest estimate. Real GDP rose at 1.6% annual rate in Q1, falling short of the 2.0% forecast but marking an acceleration from the 0.5% final estimate seen in Q4 of last year.

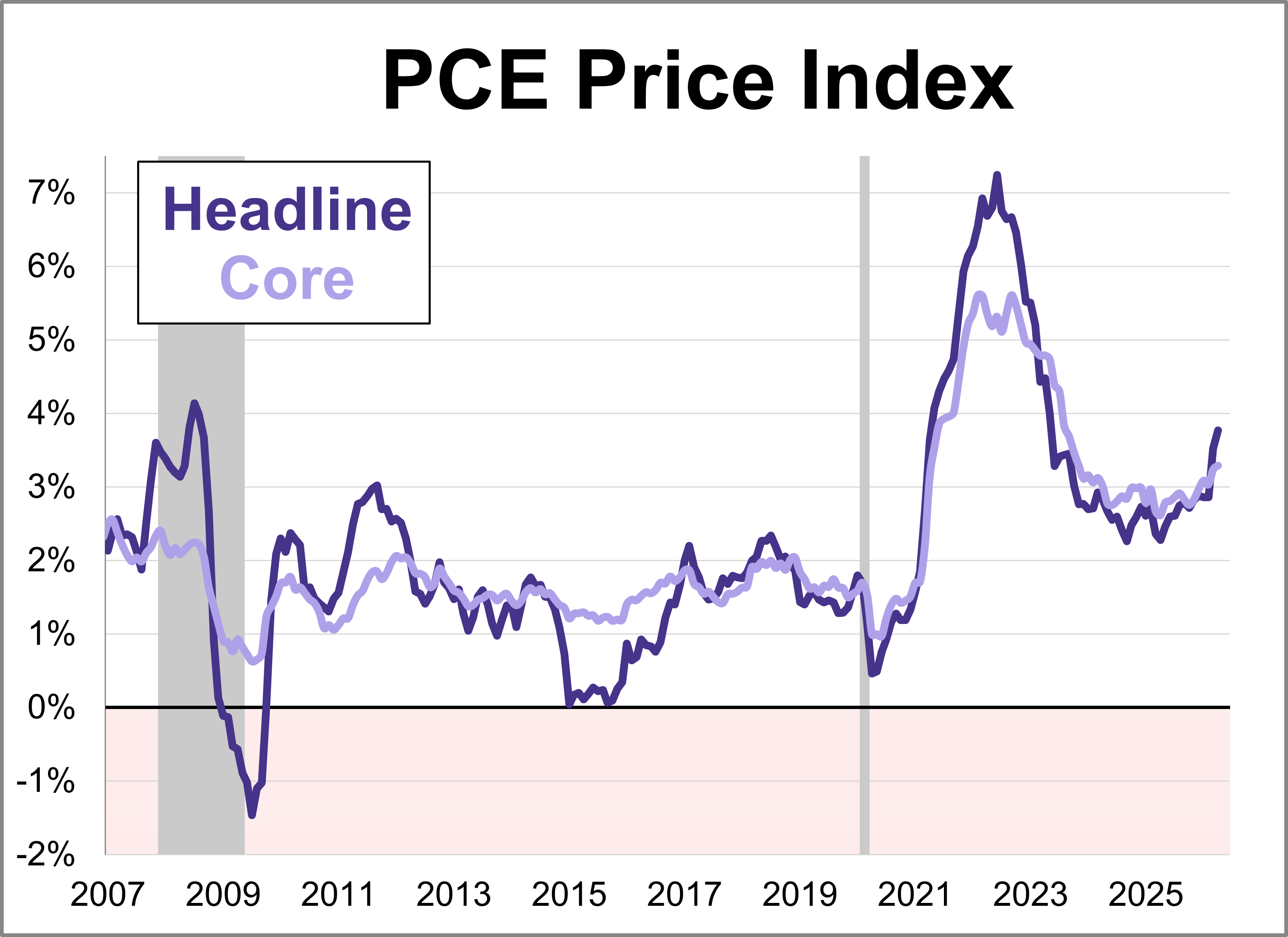

The Federal Reserve’s preferred inflation gauge, the core PCE price index, climbed 3.3% year-over-year in April. This marks the highest level since November 2023 and marks a steady pickup from March's 3.2% reading. On a monthly basis, core prices rose 0.2%.

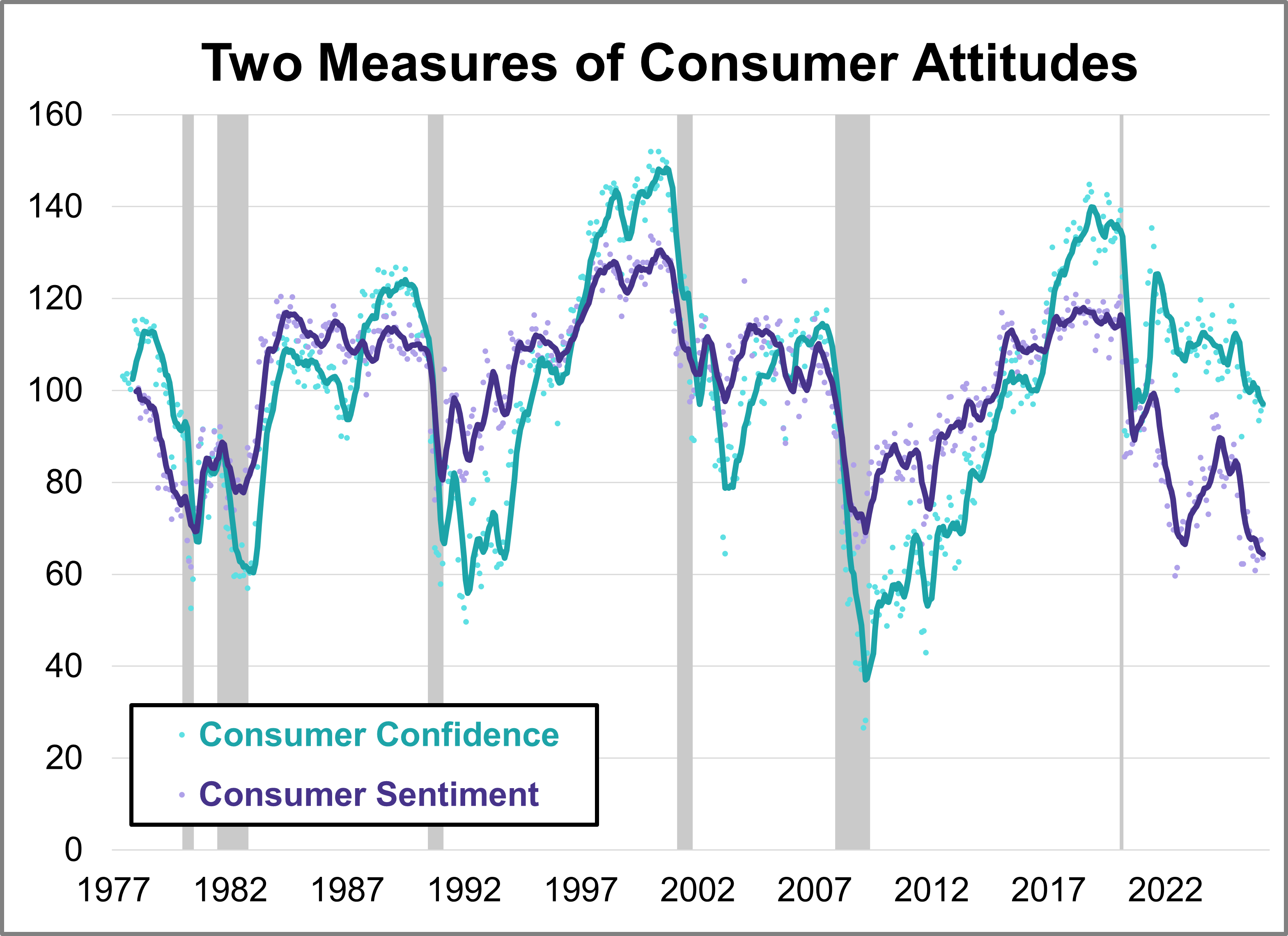

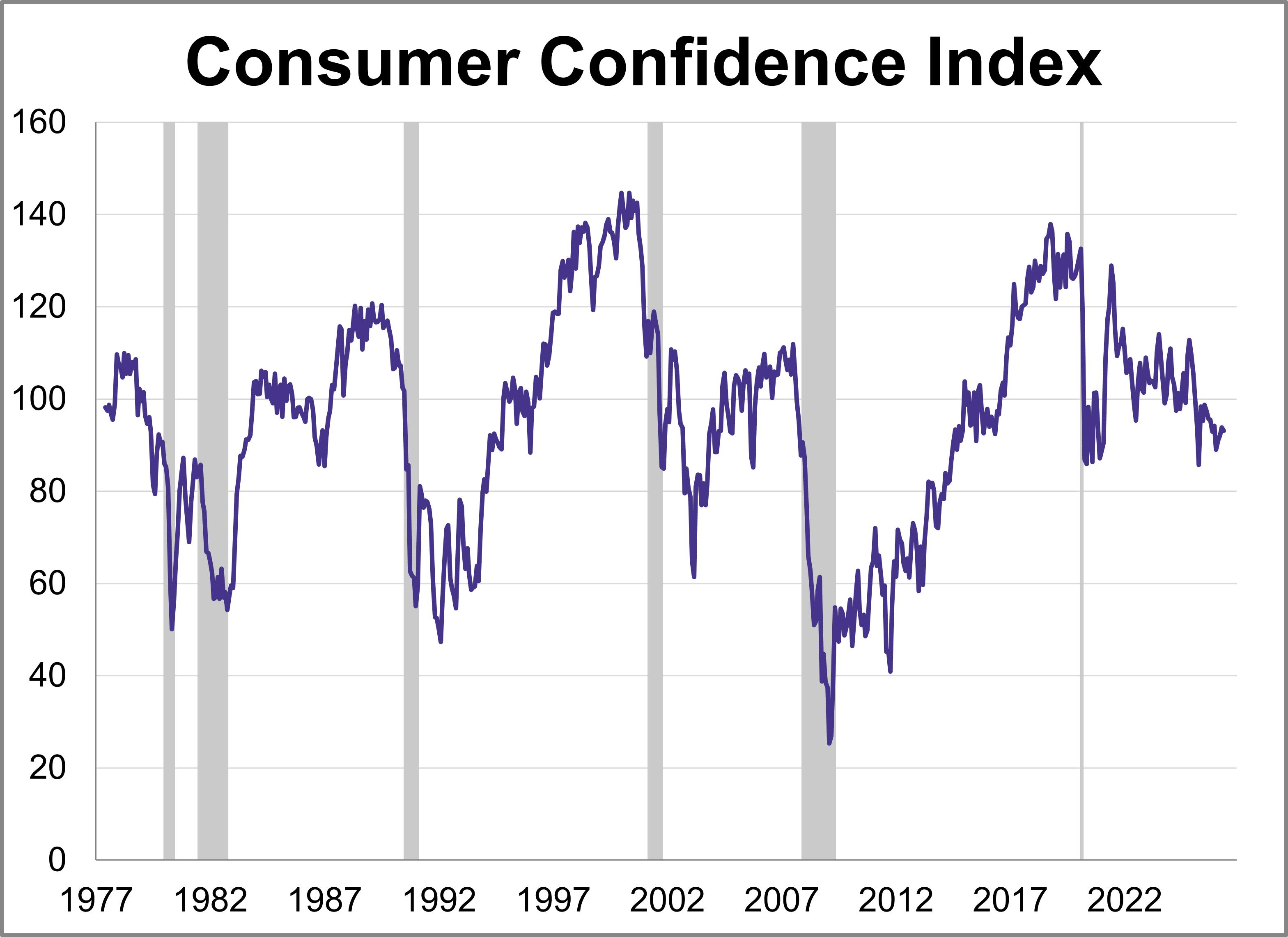

What are consumers thinking about the economy? Their collective mood offers crucial clues for businesses, investors, and policymakers alike. In May, the two leading benchmarks, the University of Michigan’s Consumer Sentiment Index (MCSI) and the Conference Board’s Consumer Confidence Index (CCI), offered similar views with both retreating amid ongoing inflation concerns.

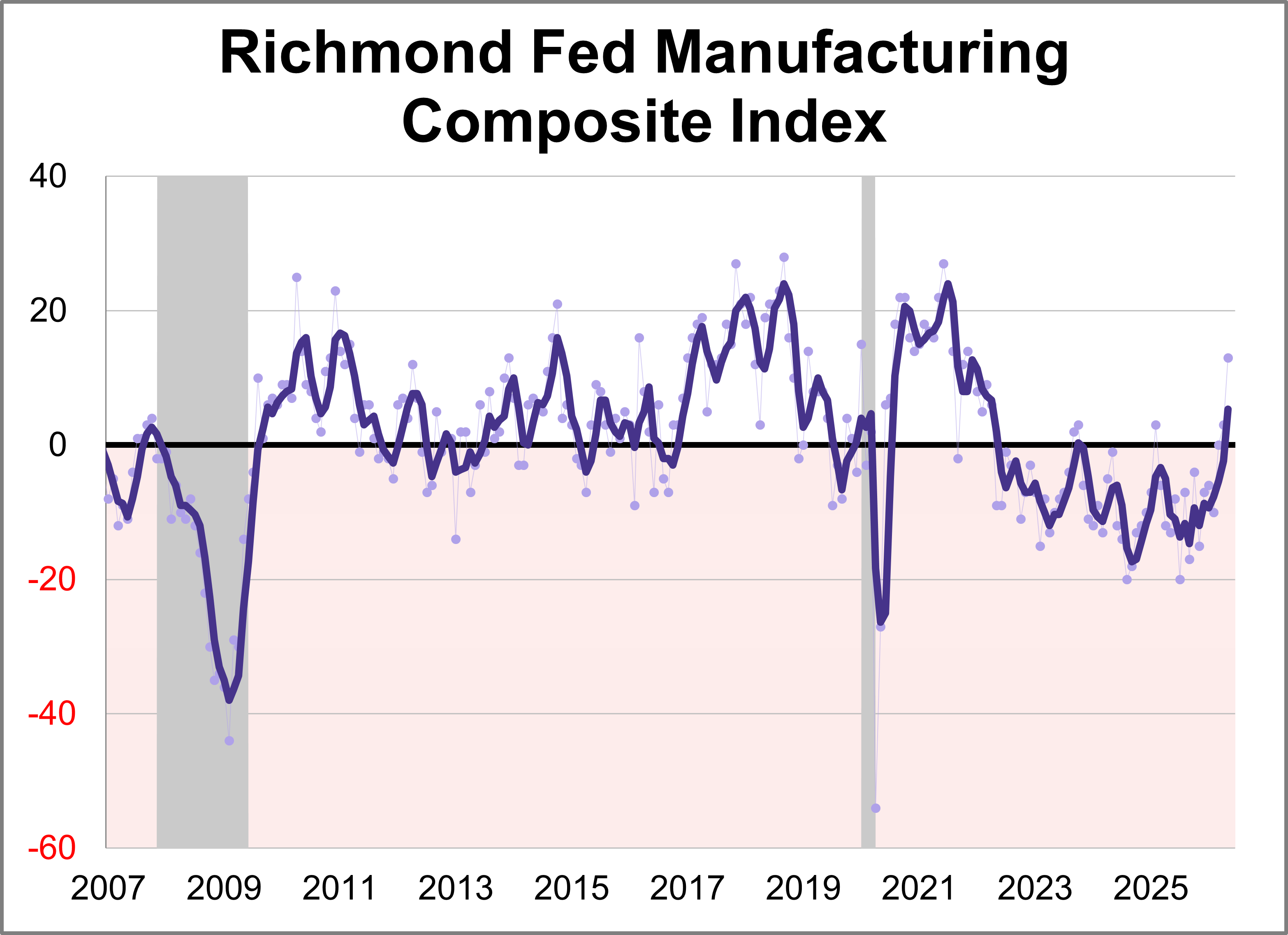

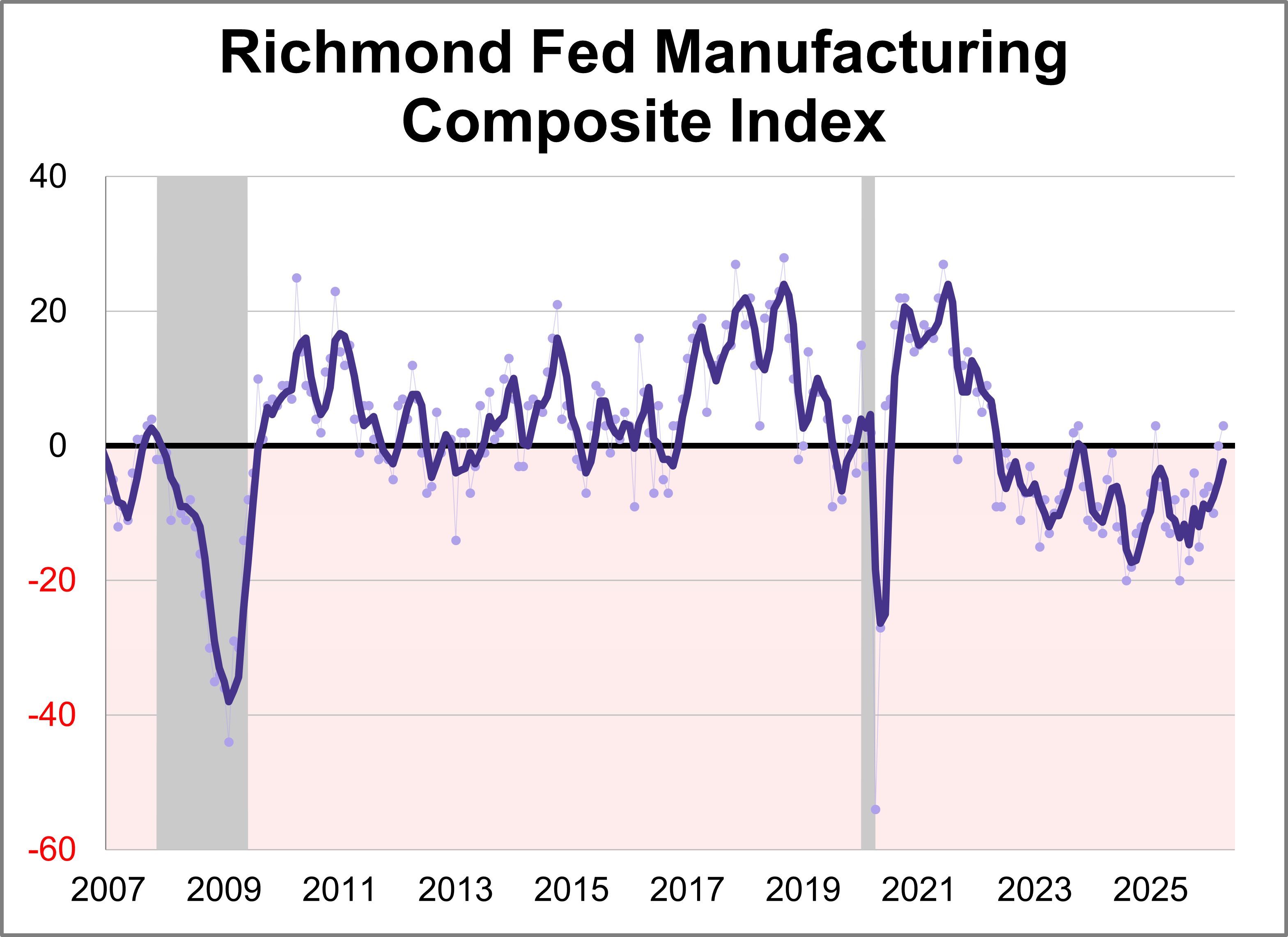

Fifth district manufacturing activity increased in May according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index rose ten points points to 13, marking the highest level in nearly five years. This month's reading was above the forecast of 4.

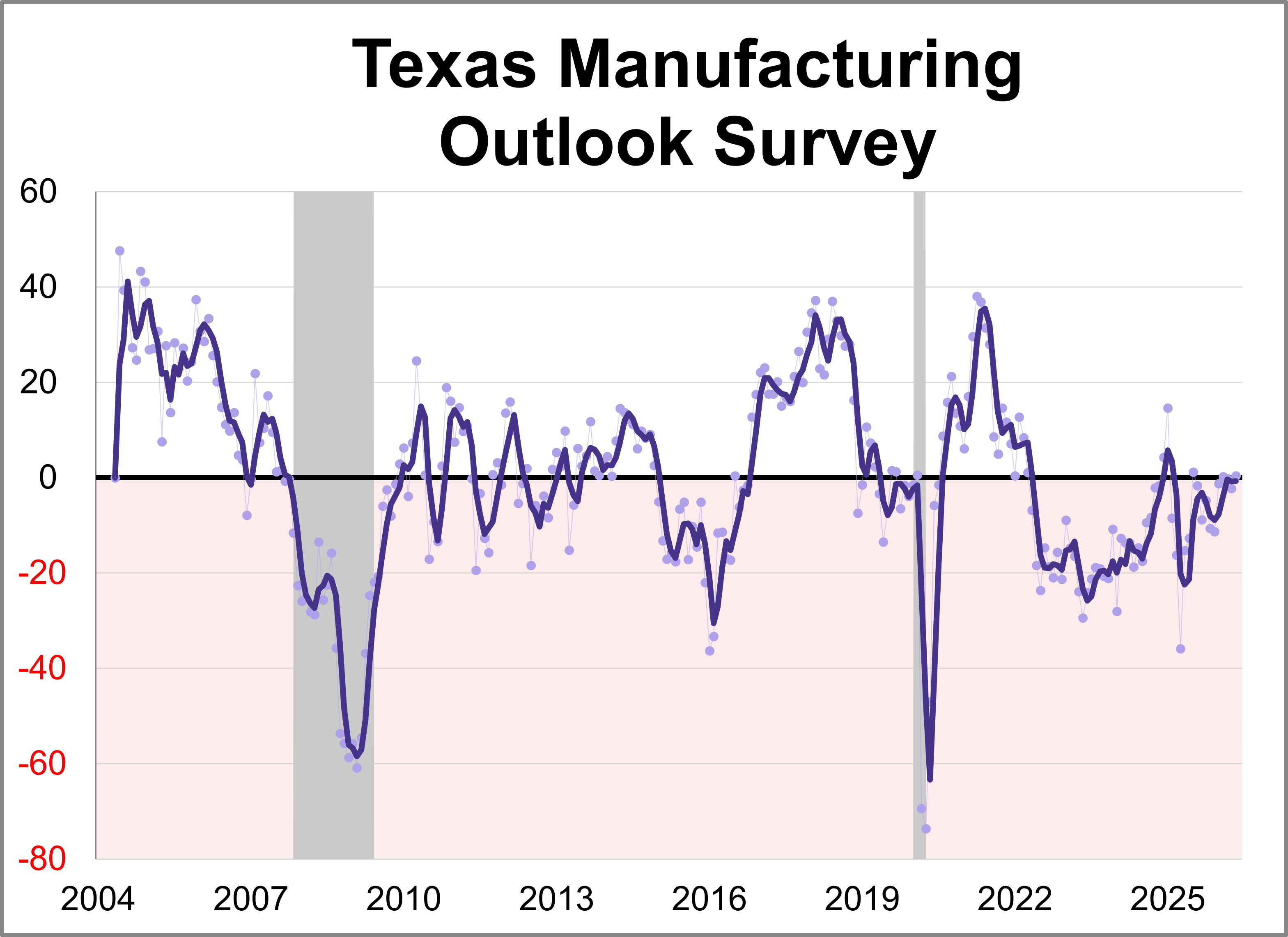

The Dallas Fed released its Texas Manufacturing Outlook Survey (TMOS) for May. The general business activity index rose 2.7 points to 0.4, indicating slower growth of manufacturing activity and stable business conditions perceptions.

The Conference Board's Consumer Confidence Index® fell for the first time in four months in May, dropping 0.7 points to 93.1. Despite the slight dip, the index came in above the forecast of 91.9.

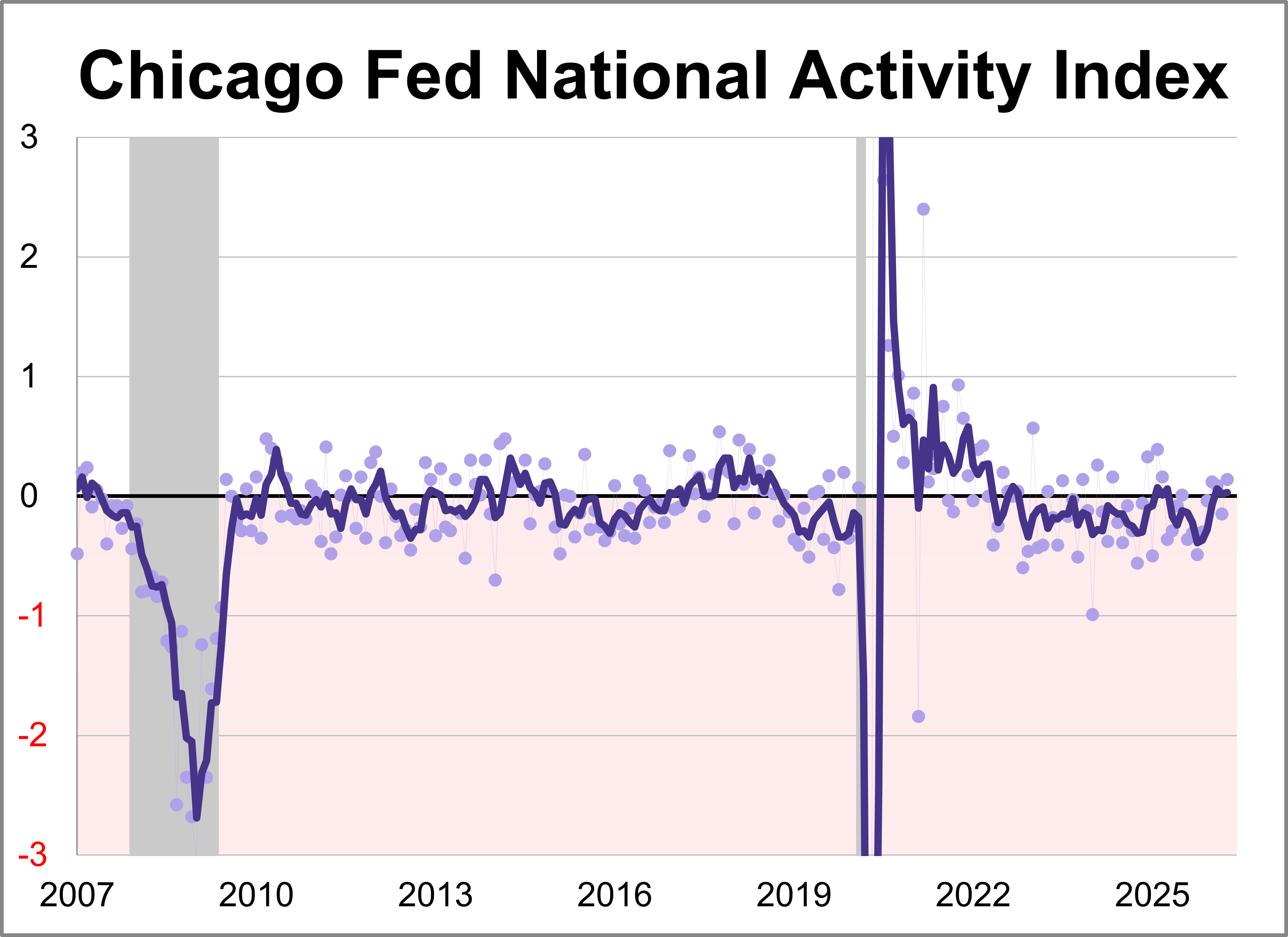

The Chicago Fed National Activity Index (CFNAI) rose to +0.14 in April from -0.15 in March. Two of the four broad categories of indicators used to construct the index increased from March, and two categories made positive contributions.

Home prices fell for the first time in eight months in March according to the S&P Cotality Case-Shiller index, as the housing slowdown intensifies. On a seasonally adjusted basis, the national index dropped 0.2% month-over-month and was up 0.7% year-over-year, the slowest pace since June 2023.

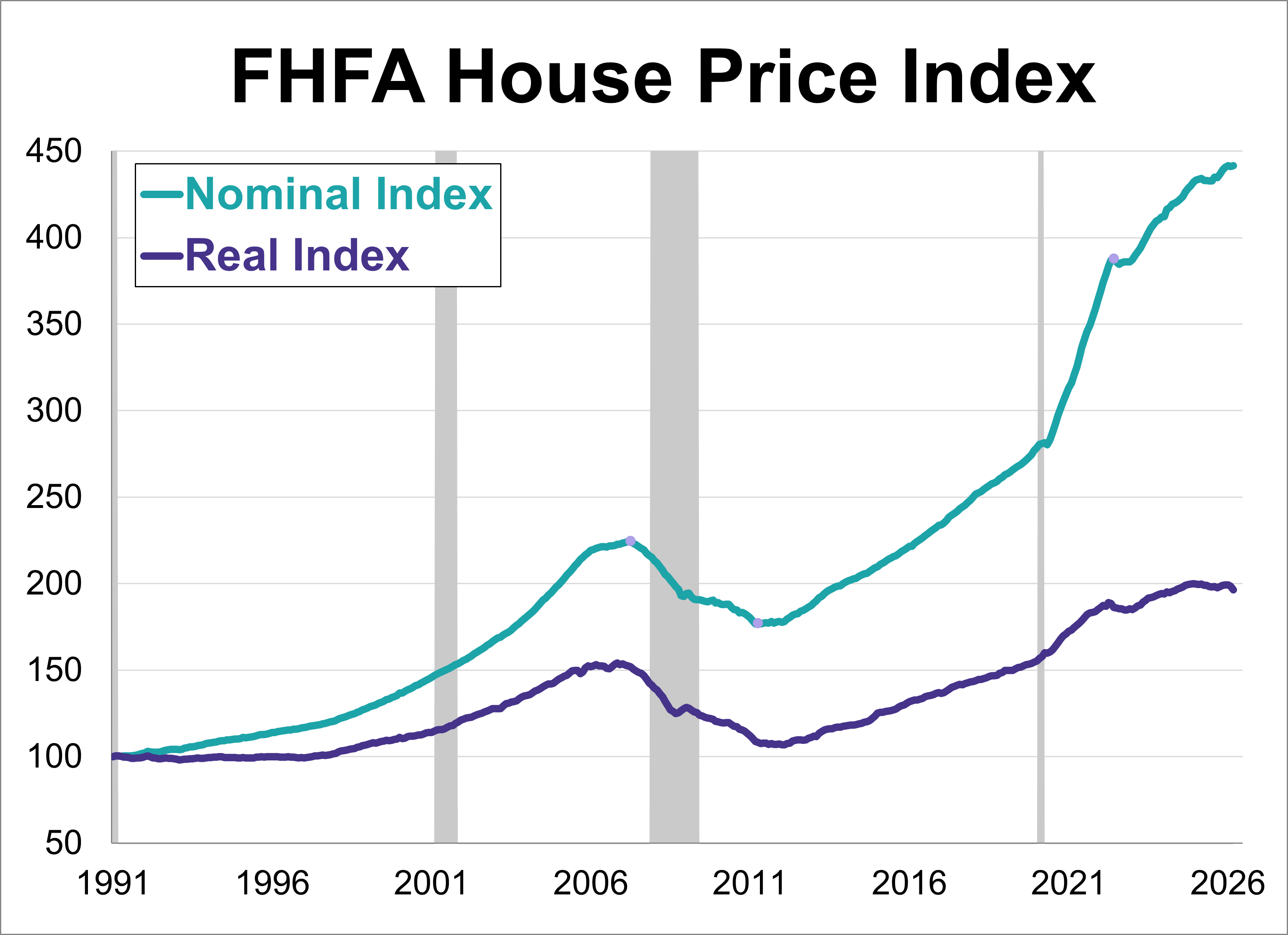

The Federal Housing Finance Agency (FHFA) House Price Index (HPI) reached a new record high in March, rising 0.1% to 441.6.

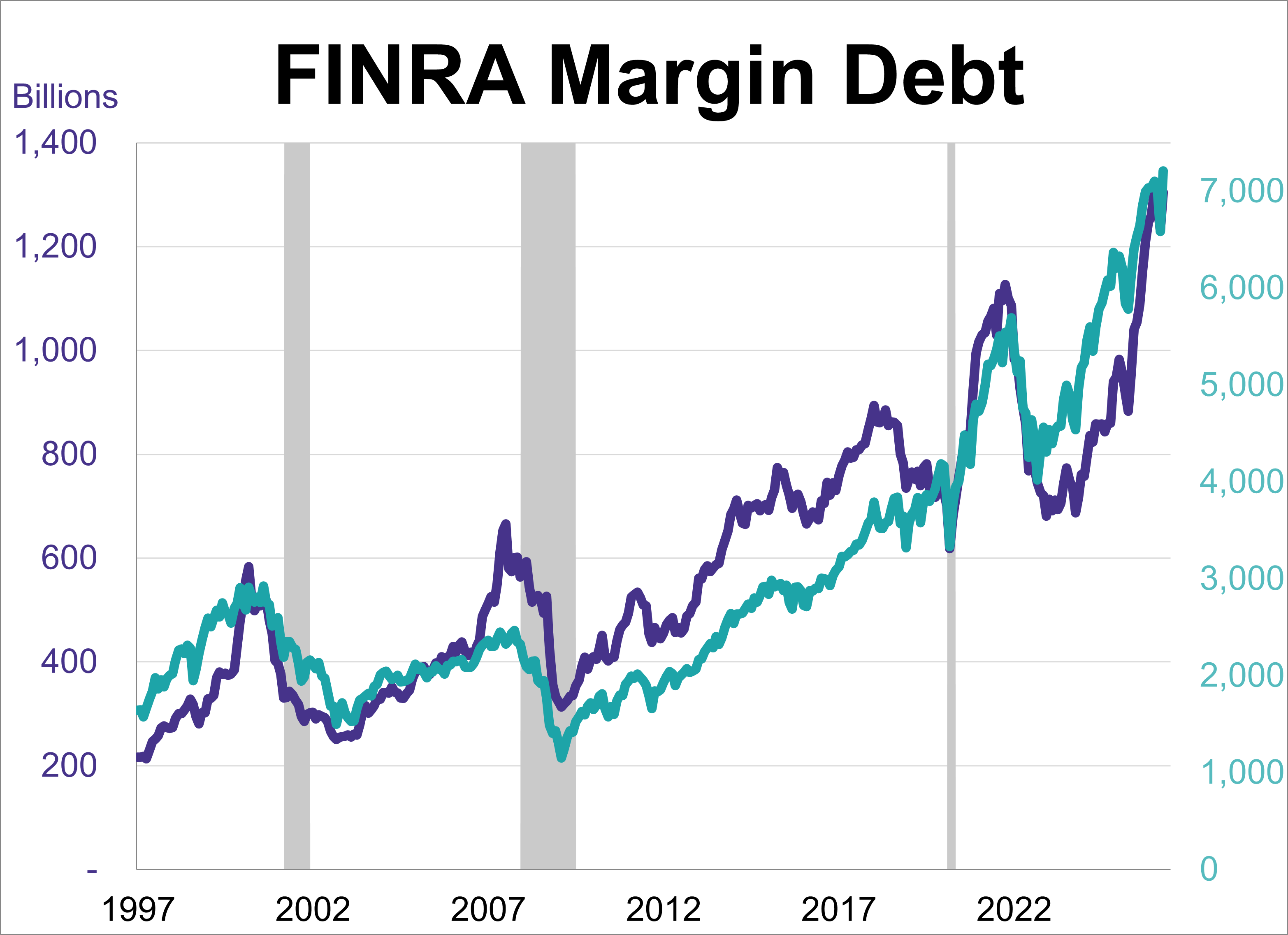

There is currently a stark contrast between everyday consumer confidence and financial market behavior. On one hand, persistent inflation and elevated living costs have driven consumer sentiment to historic lows. On the other hand, financial market participants are exhibiting aggressive risk appetite, with margin debt surging to an all-time high record on the heels of major equity market gains.

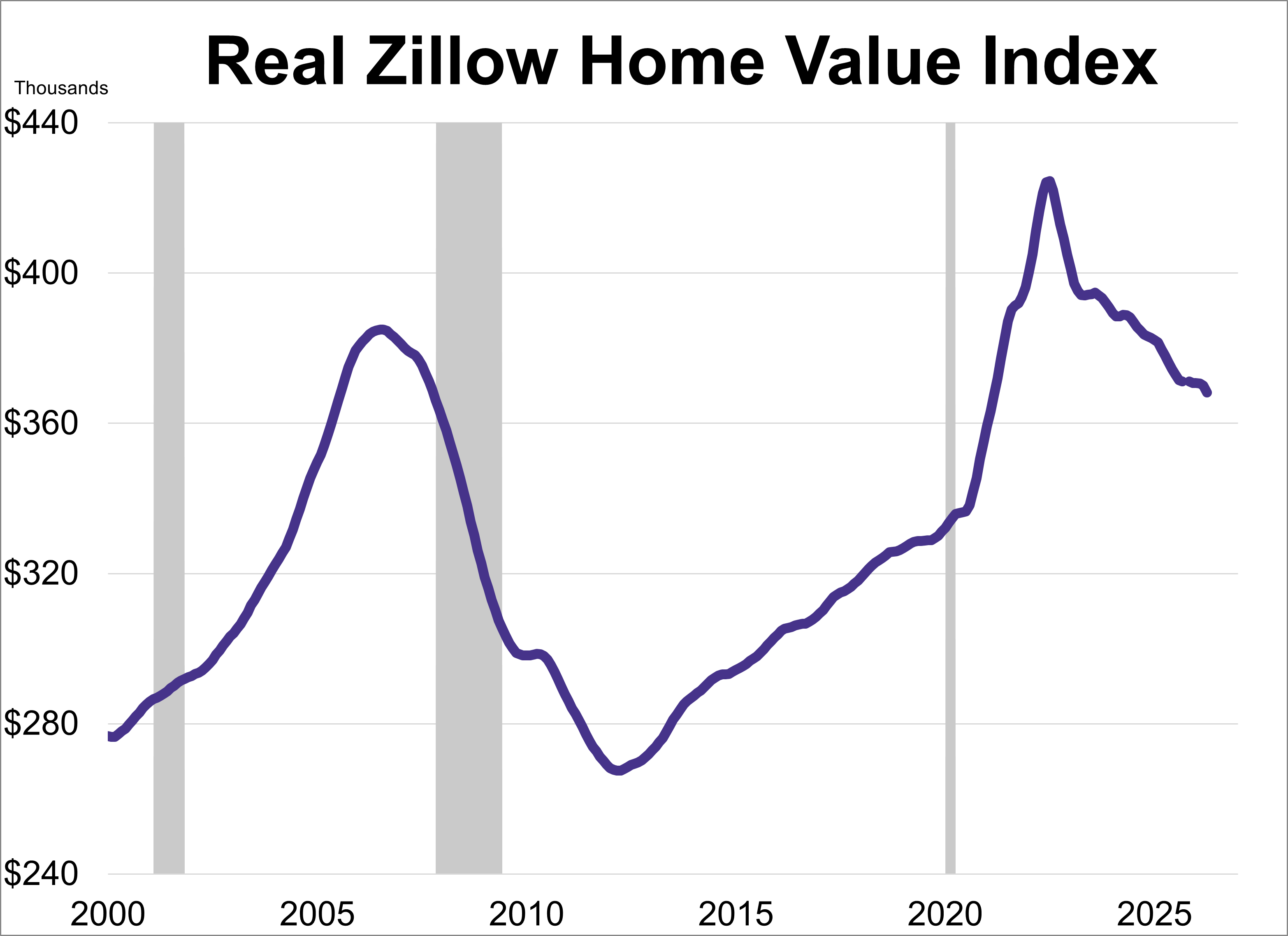

Home values continued their upward trend in April, according to the Zillow Home Value Index. However, after adjusting for inflation, real home values dropped sharply, remaining at their lowest level in over five years.

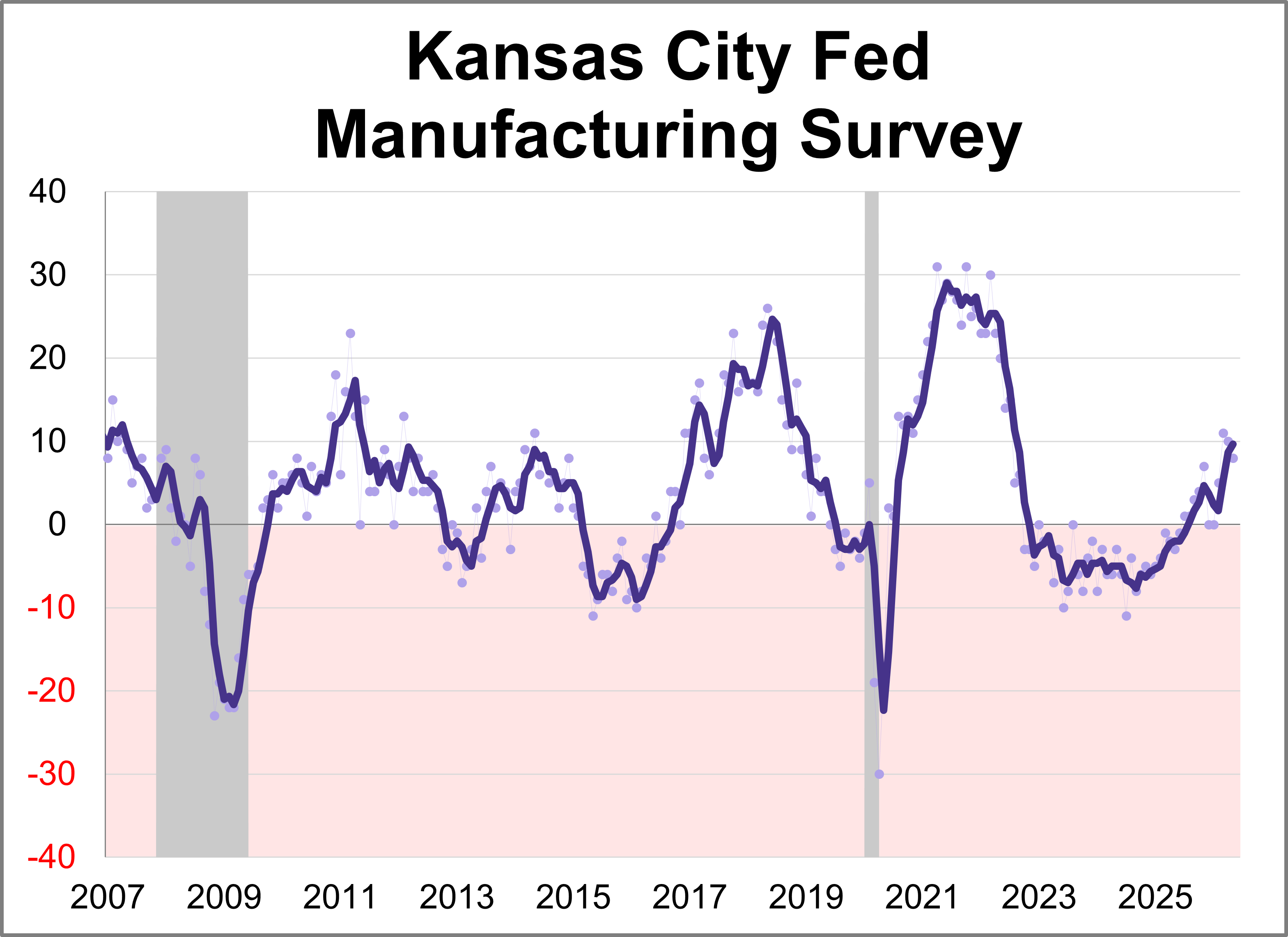

The Kansas City Fed Manufacturing Survey revealed regional activity continued to increase in May. The composite index came in at 8 this month, down slightly from 10 in April but still indicating continued expansion.

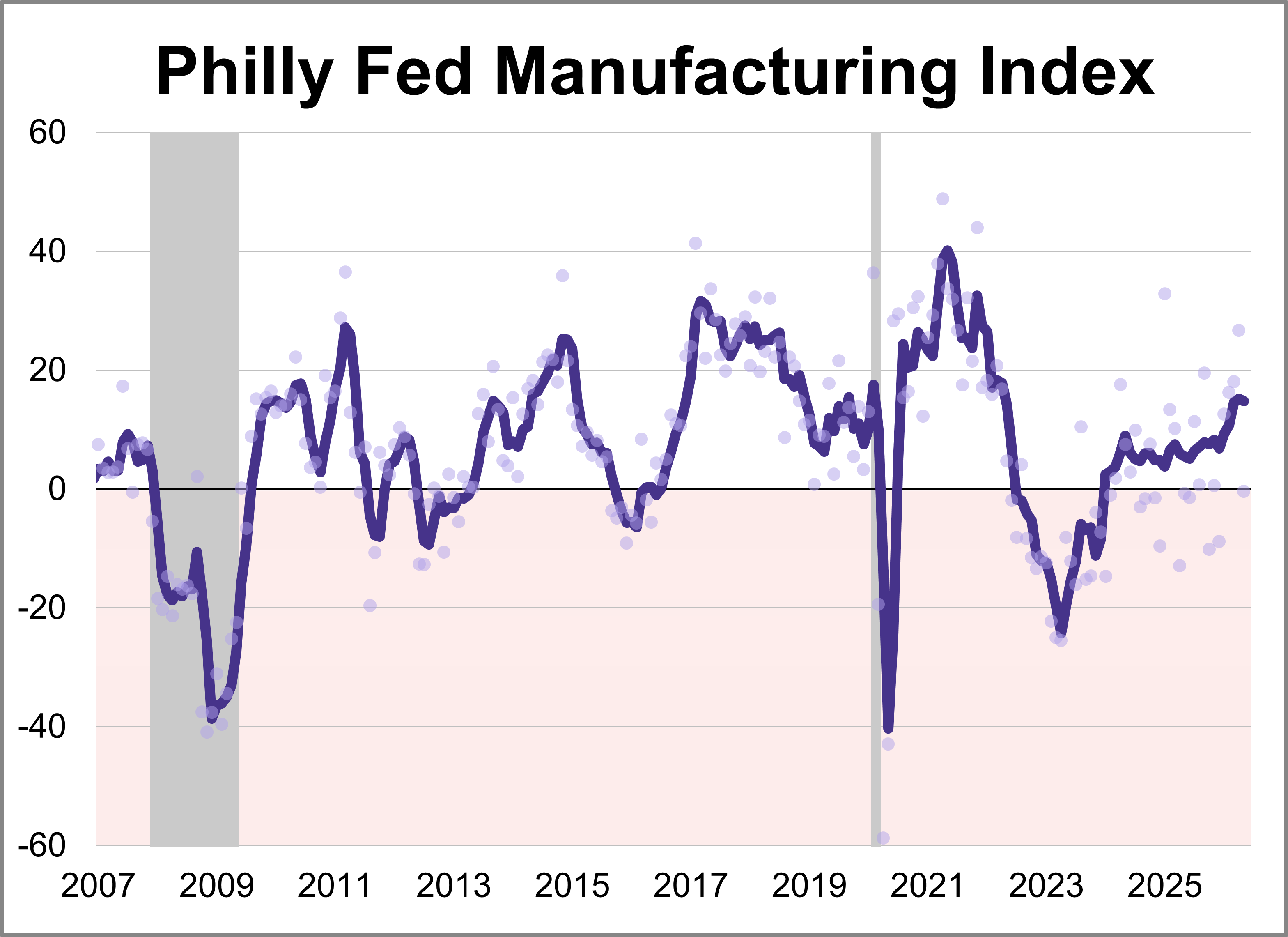

The latest Philadelphia Fed manufacturing index showed activity weakened in May, with the index sinking 27.1 points to -0.4. The latest reading marked the lowest level for the index this year and was worse than the forecast of 17.6.

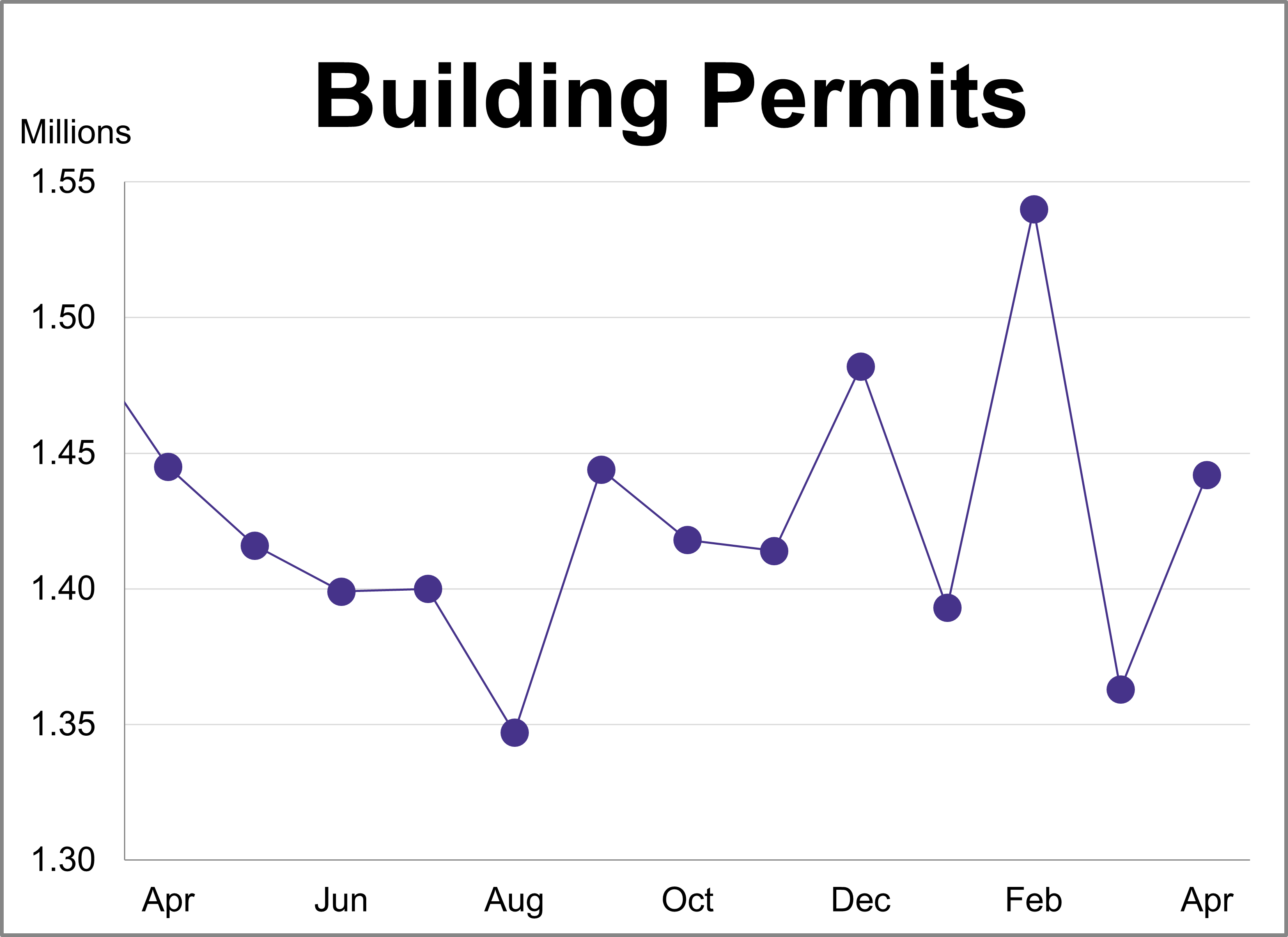

Building permits rose 5.8% to a seasonally adjusted annual rate of 1.442 million. The latest reading exceeded the forecast of 1.380 million.

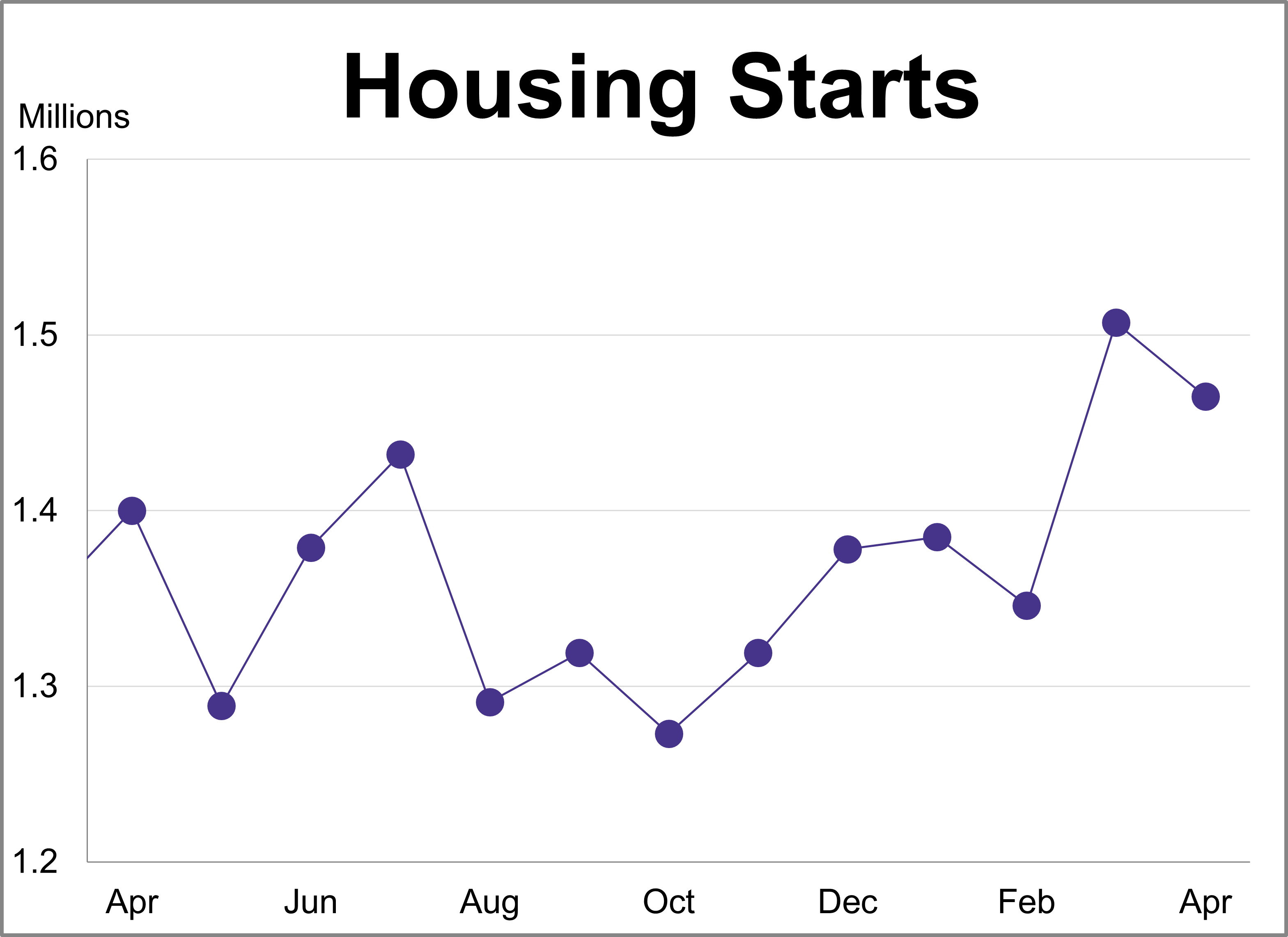

Housing starts fell 2.8% in April to a seasonally adjusted annual rate of 1.465 million. The latest reading exceeded the projected 1.420 million.

Margin debt rose for the first time in three months to a record high in April, coming in at $1.30 trillion. This marked a 6.8% increase from March and a 53.3% rise compared to the previous year.

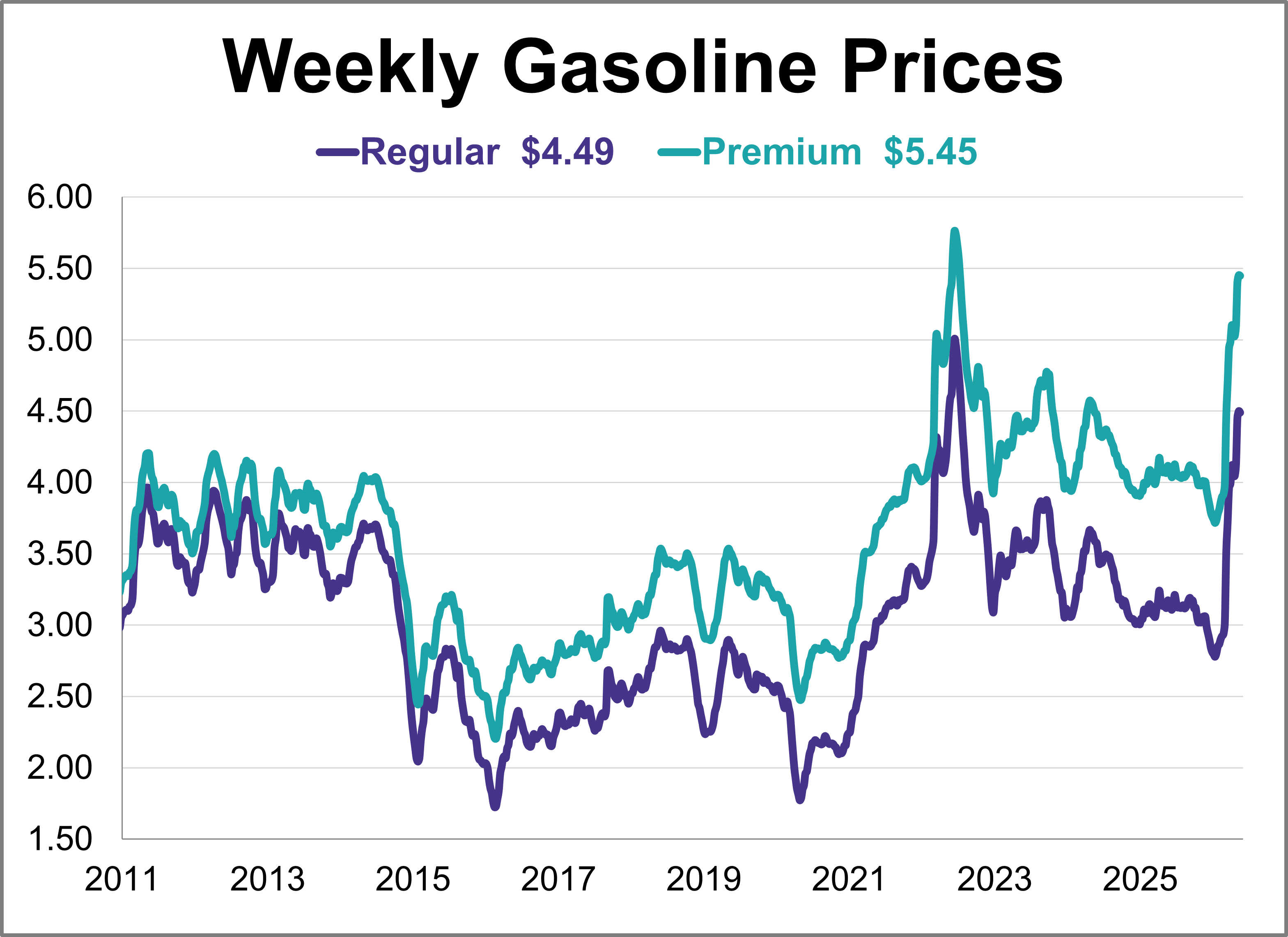

Gas prices were relatively flat this week, remaining at their highest level in nearly four years. As of May 18th, weekly prices were down 1 cent for regular and were unchanged for premium.

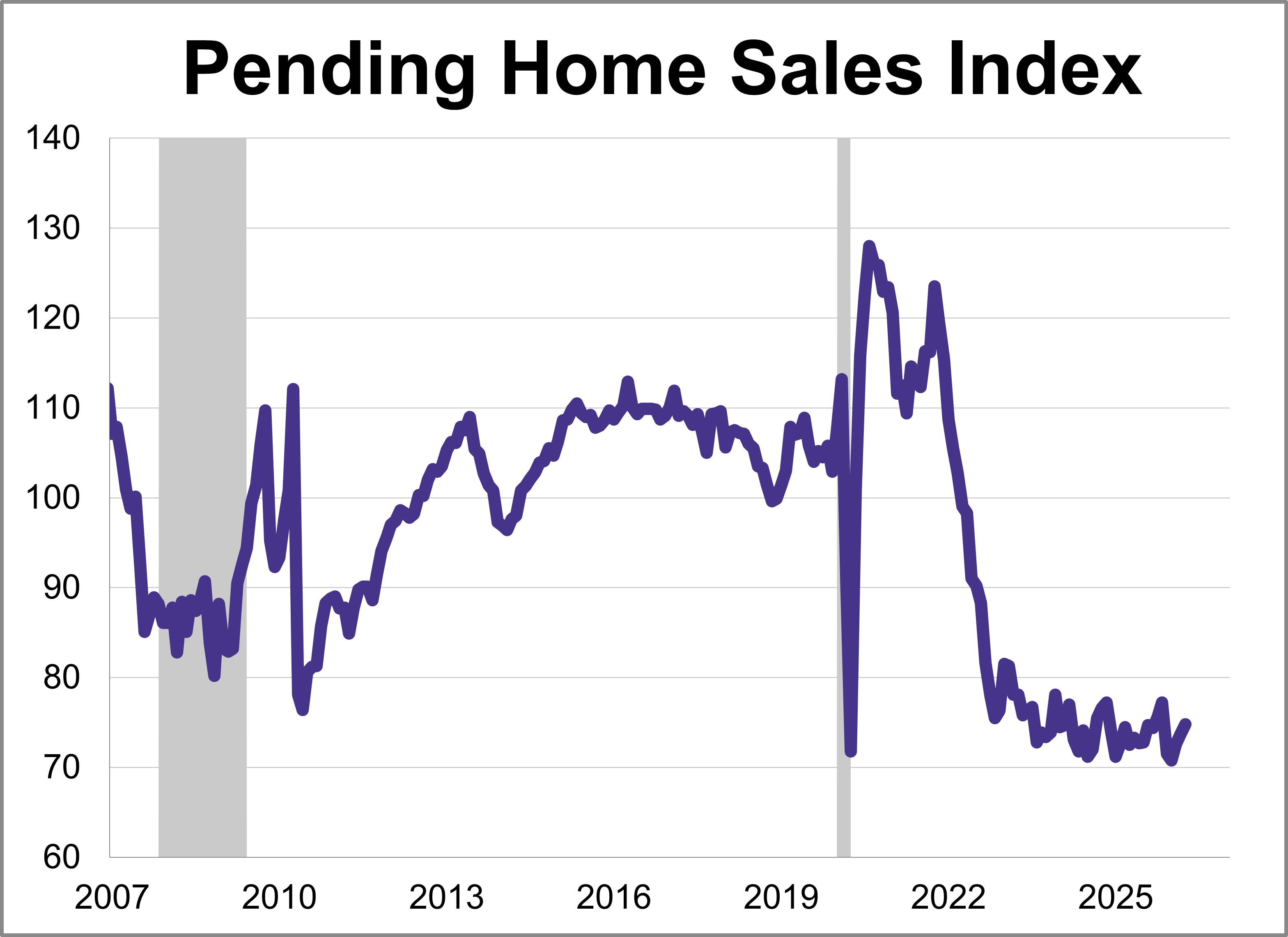

The National Association of Realtors® (NAR) pending home sales index rose 1.4% in April to 74.8, markings its third consecutive increase and highest level since November.

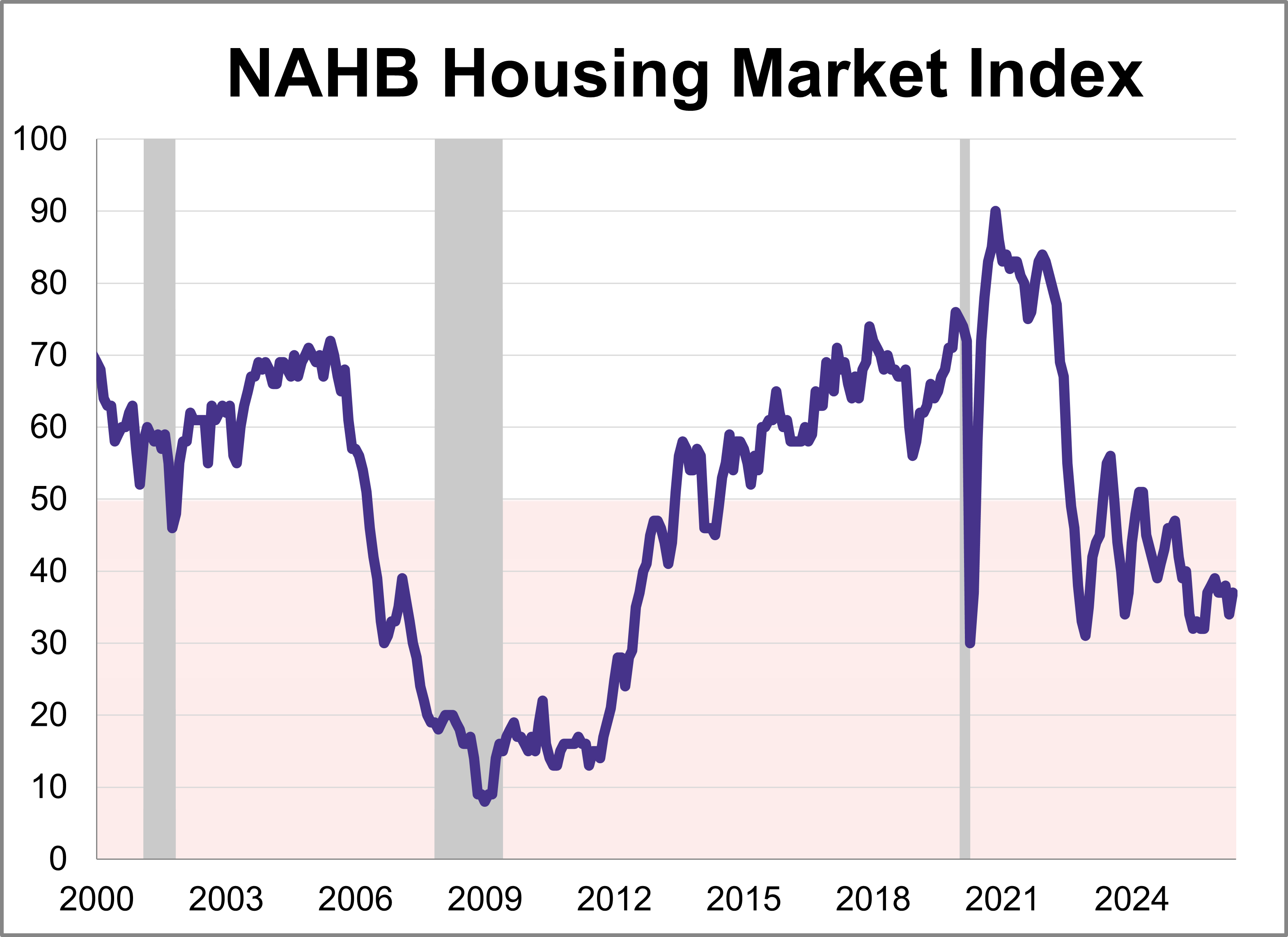

Builder confidence posted a modest gain in May despite persistent affordability challenges and economic uncertainty. The National Association of Home Builders (NAHB) Housing Market Index (HMI) rose 3 points from April to 37 this month, marking the 25th consecutive negative reading.

The U.S. economic landscape in April was defined by a significant rebound in inflation across both consumer and wholesale sectors, complicating the path for future monetary policy.

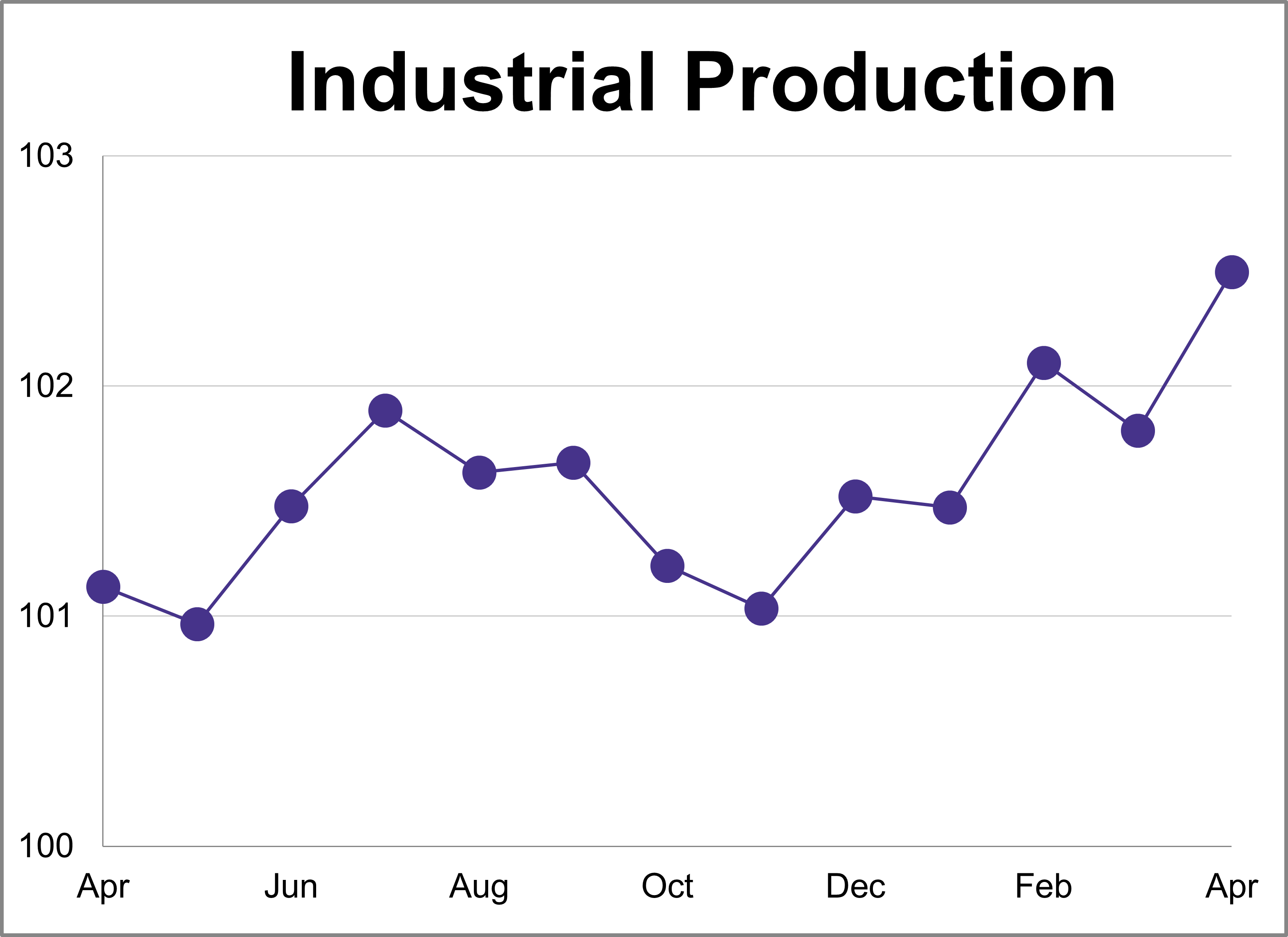

Industrial production rose more than expected in April, increasing 0.7% after a 0.3% decline in March. This was higher than the expected 0.3% growth and marks a 1.4% increase compared to one year ago.

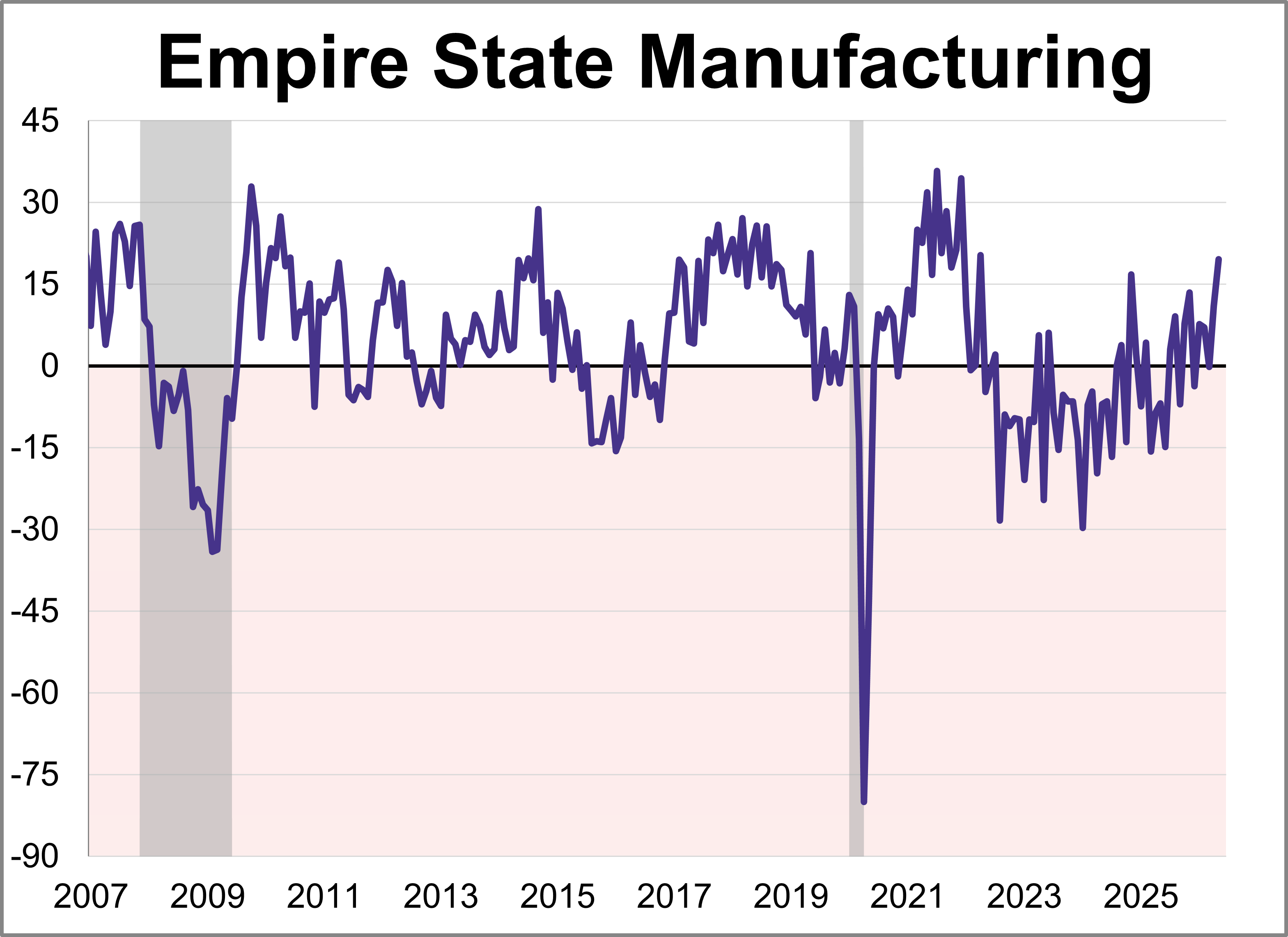

Manufacturing activity grew strongly in New York State, according to the Empire State Manufacturing May survey. The diffusion index for General Business Conditions rose 8.6 points to 19.6, its highest level in over four years.

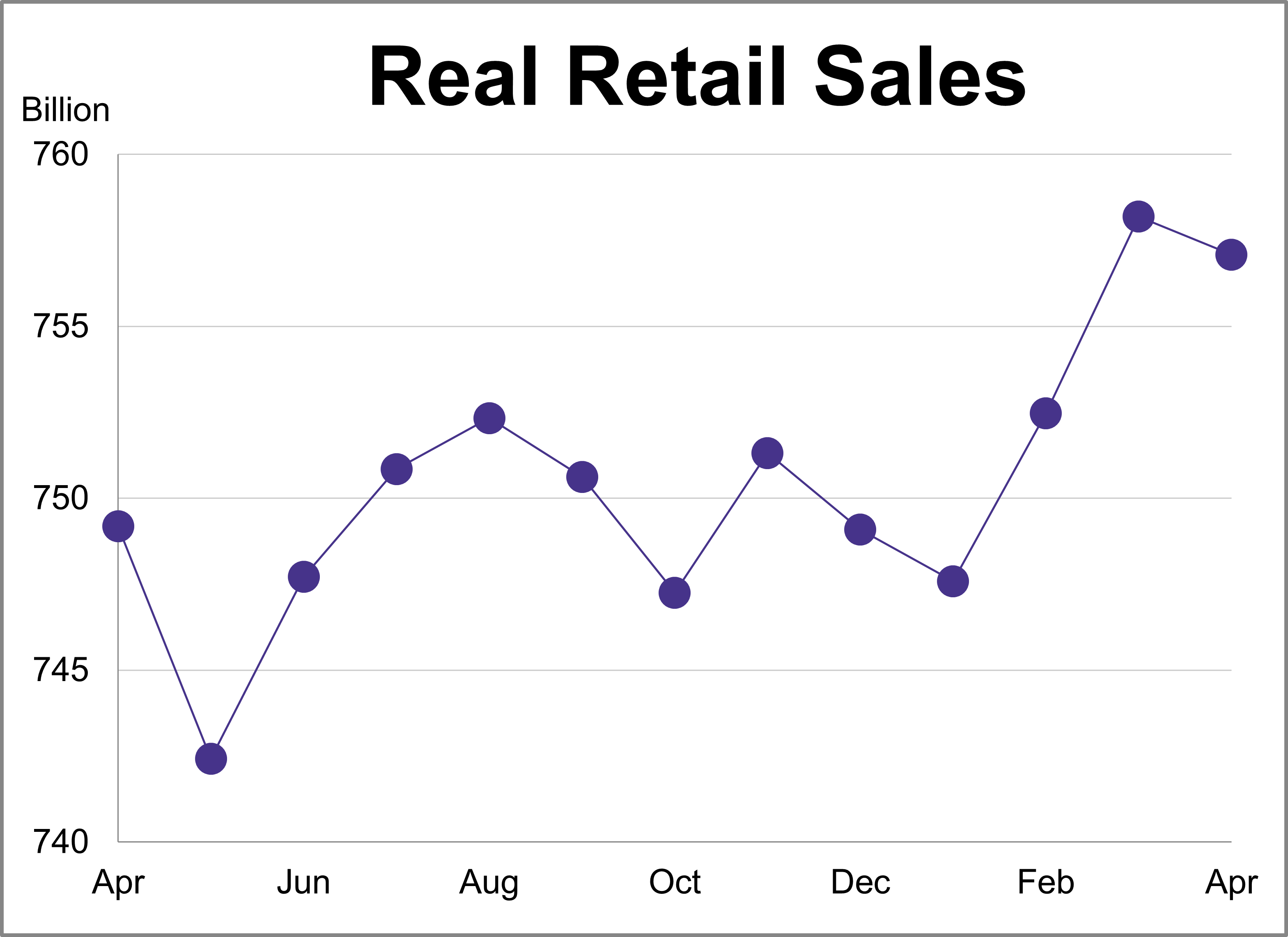

Nominal retail sales were up 0.49% month-over-month and up 4.87% year-over-year in April. However, after adjusting for inflation, real retail sales were down 0.15% month-over-month and up 1.05% year-over-year.

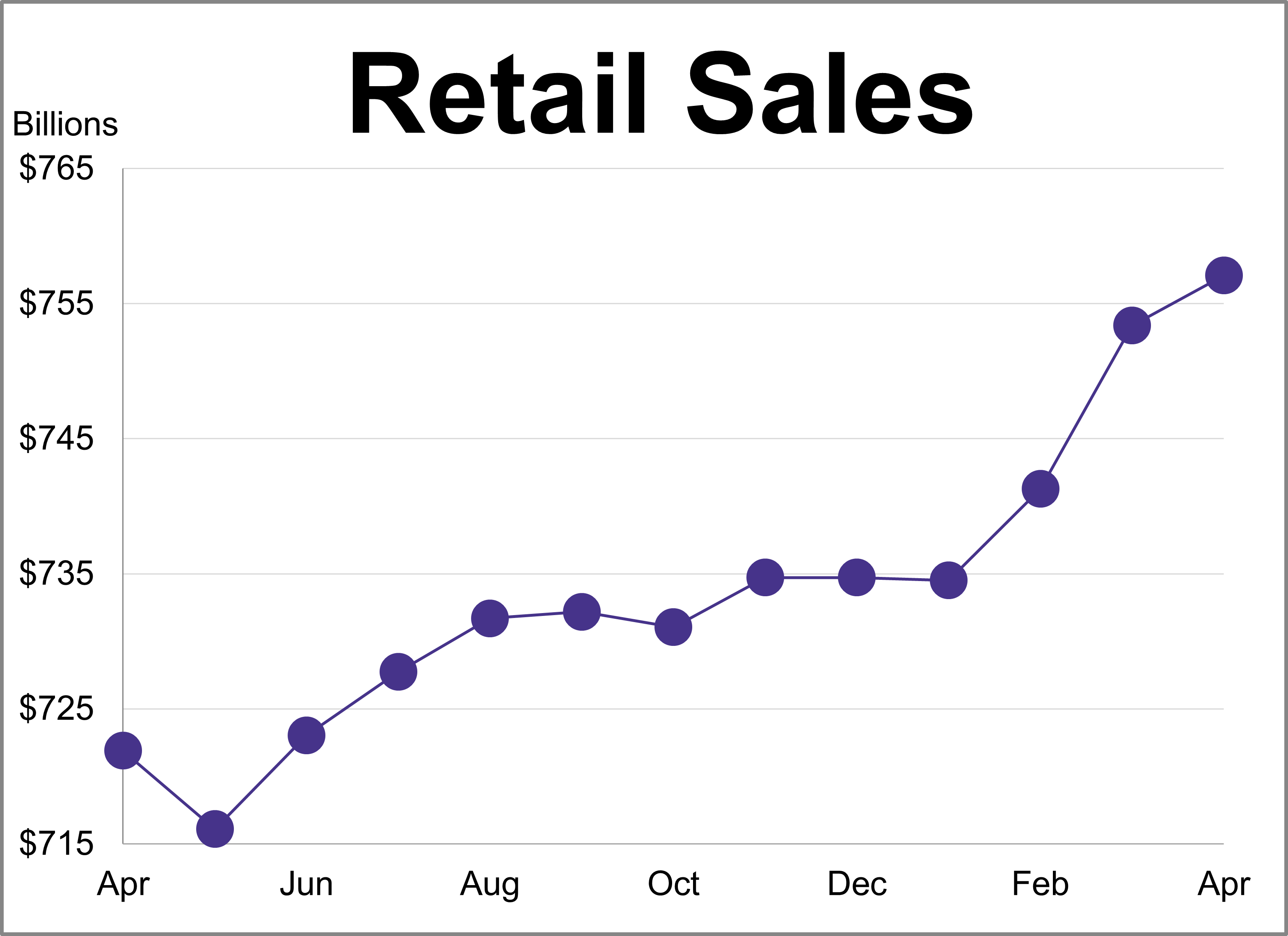

According to the Census Bureau’s Advance Retail Sales Report, consumer spending climbed for the third consecutive month in April. While headline sales rose 0.5% (as expected), this marked a deceleration from March’s 1.6% surge, with much of the gain driven by higher prices at the pump.

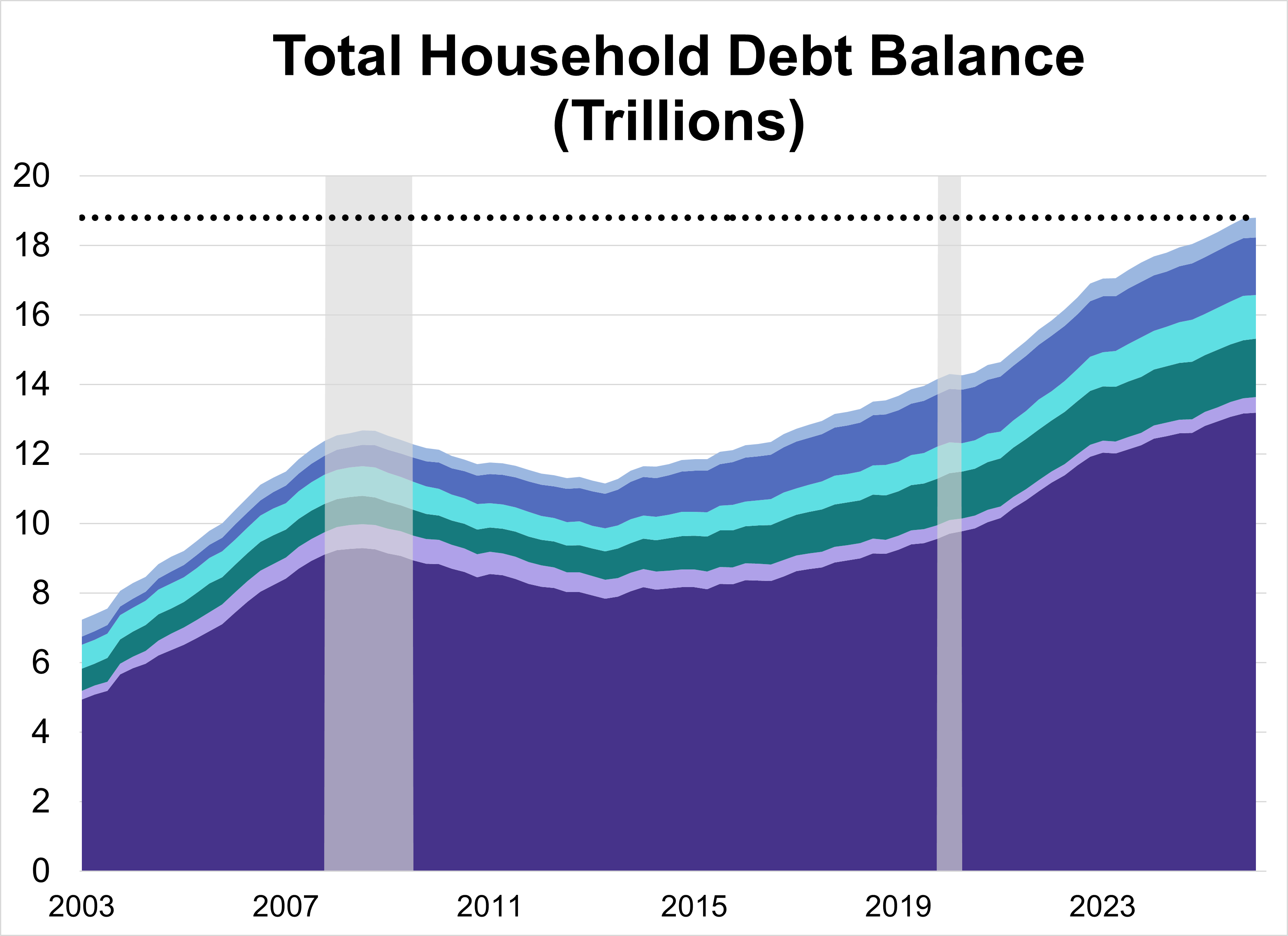

Total U.S. household debt climbed to a record $18.79 trillion in Q1 2026, a modest 0.1% ($18 billion) increase from the previous quarter. The overall rise was driven by increases across a handful of categories, specifically mortgage and auto loan balances.

The U.S. labor market demonstrated remarkable endurance in April, with job gains outpacing expectations and private sector expansion reaching its strongest point in over a year. As the Federal Reserve maintains a steady interest rate policy, the focus now turns to upcoming inflation and retail data to gauge the sustainability of this momentum.

The U.S. economy ended April with mixed signals: steady interest rates and high Fed dissent met persistent, energy-driven inflation. Despite these hurdles, accelerated Q1 growth and rising consumer confidence provided a buffer against ongoing global instability.

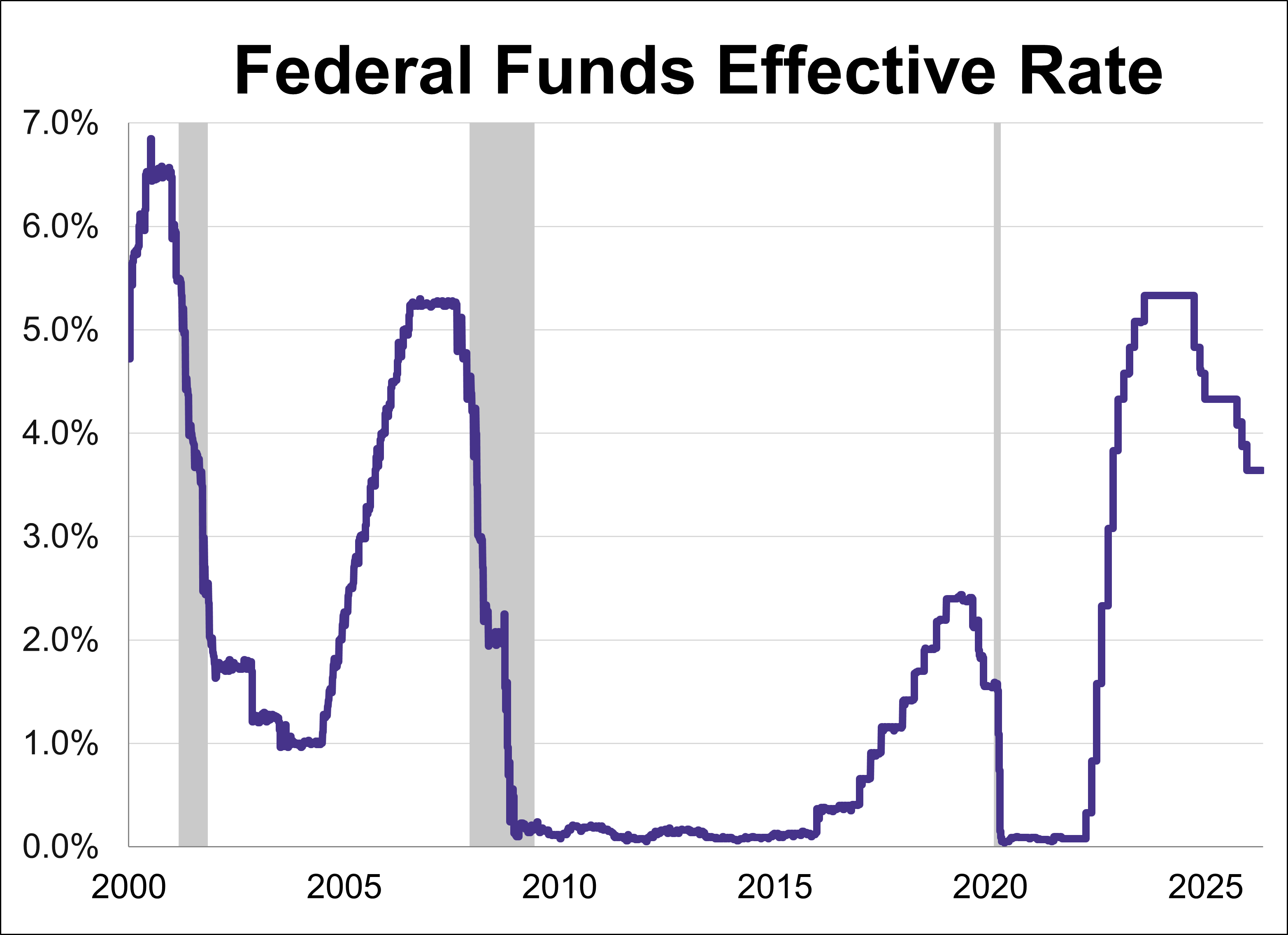

The Federal Reserve concluded its third meeting of the year by holding the federal funds rate (FFR) steady in the 3.50%-3.75% range.

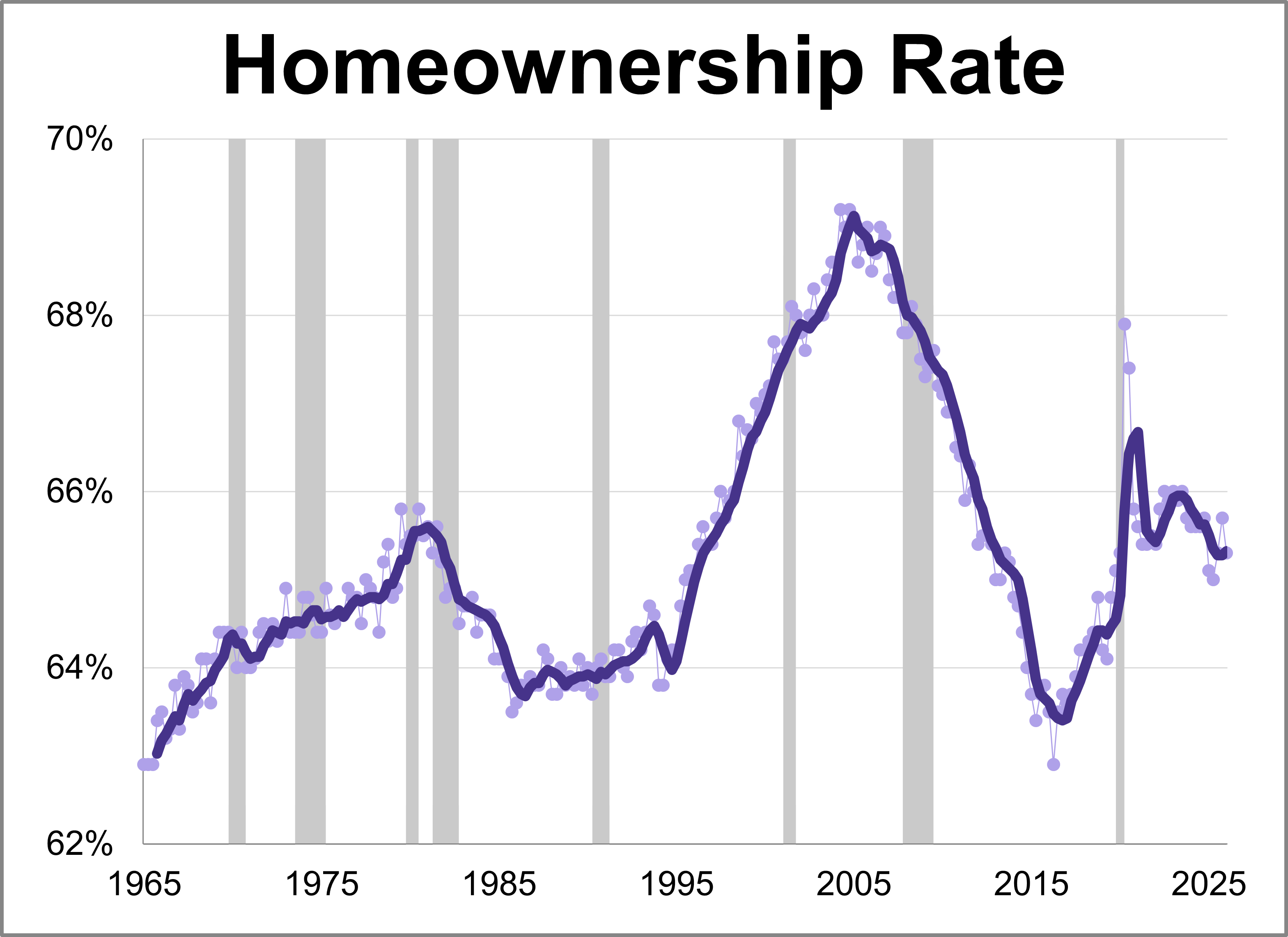

The Census Bureau released its latest quarterly report for Q1 2026 showing the latest homeownership rate is at 65.3%.

Fifth district manufacturing activity increased in April according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index rose three points points to 3, marking the highest level for the index in 20 months. This month's reading was above the forecast of 2.

Last week’s economic data was defined by conflicting signals from the consumer. While retail figures suggest resilience, sentiment levels have plummeted to record lows. Meanwhile, the S&P 500 continued its historic rally as markets prepare for the upcoming Fed decision.

While recent market performance reflects optimism over potential geopolitical de-escalation, underlying economic data reveals a complex landscape of intensifying price pressures and cooling growth. This article examines the major economic news from the week of April 6-10th, 2026.

While recent market performance reflects optimism over potential geopolitical de-escalation, underlying economic data reveals a complex landscape of intensifying price pressures and cooling growth.

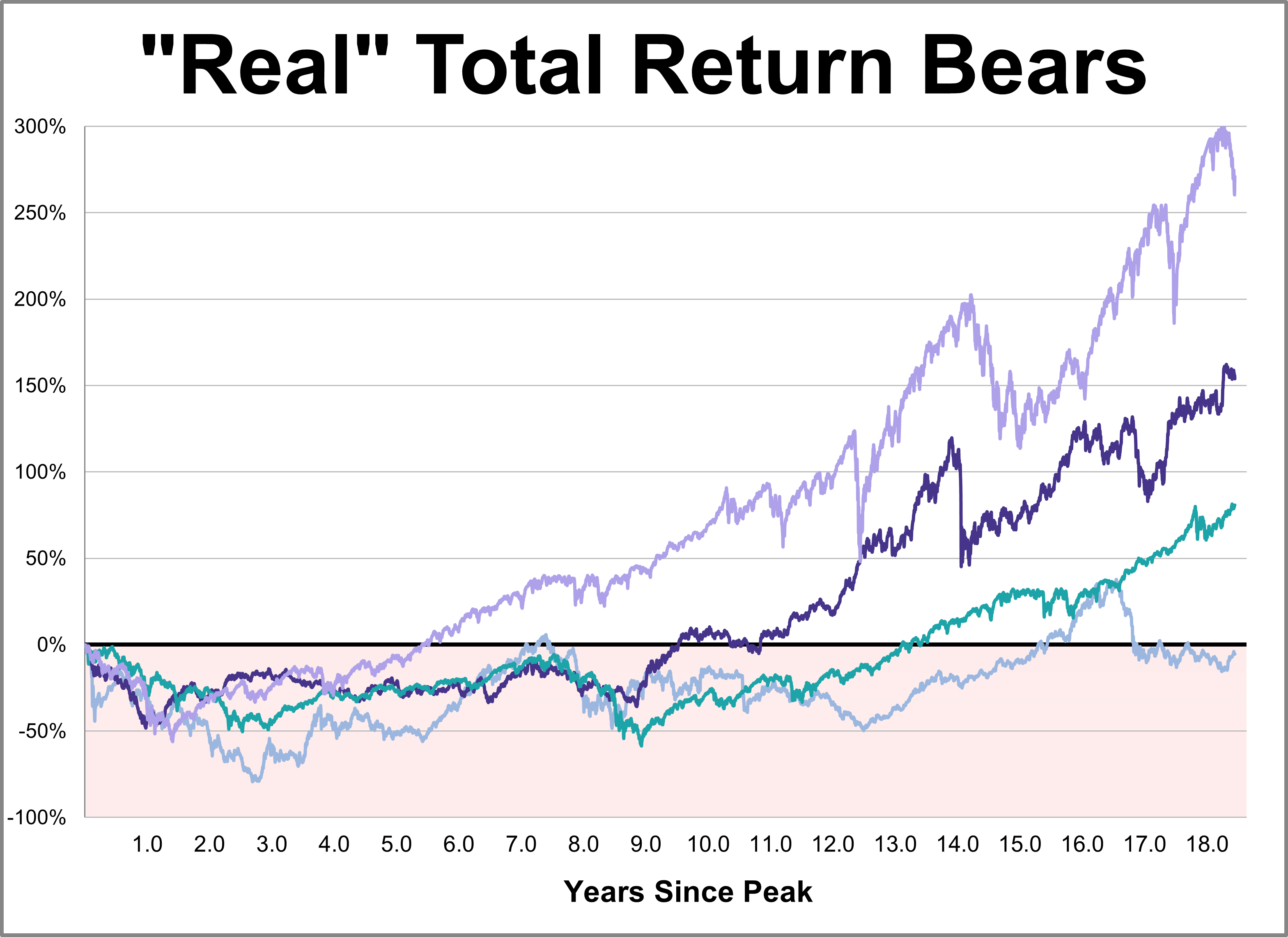

While every market downturn is unique, history offers a crucial lens for understanding recovery. This chart series provides a comprehensive overlay of the Four Bad Bears in U.S. history since the 1929 peak, comparing their recovery paths through the S&P 500's close on March 31, 2026.

Heavily influenced by escalating geopolitical conflicts, last week's economic snapshot reveals a sharp erosion of confidence among consumers and investors alike.

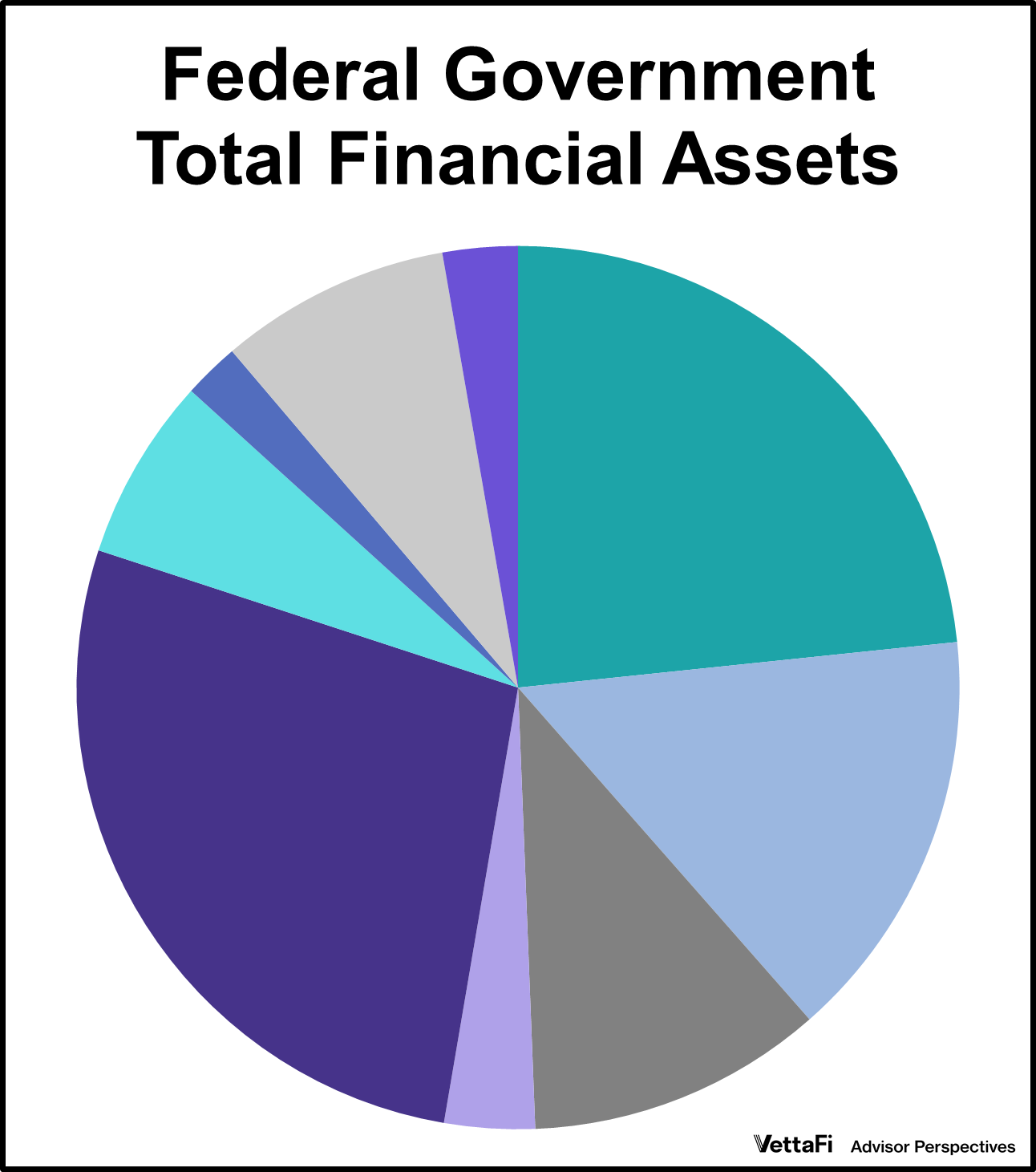

When we think of the U.S. government's finances, we often focus on the massive debt. But what about the assets? What does Uncle Sam actually own, and which asset is the largest?

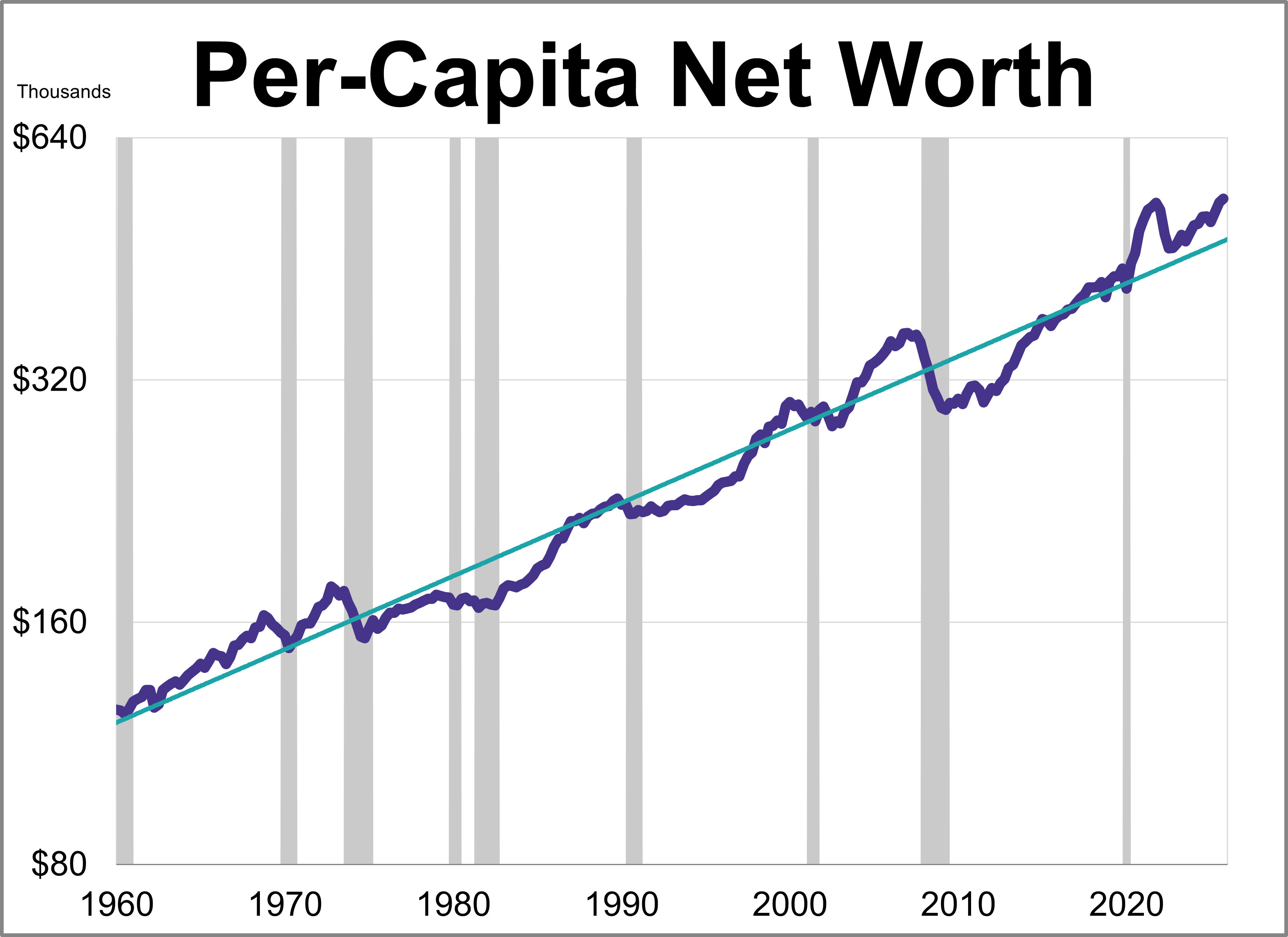

How much wealthier are Americans since the Great Recession? While a look at the headlines shows a staggering 211% increase in household net worth since 2009, adjusting for inflation tells a much different story.

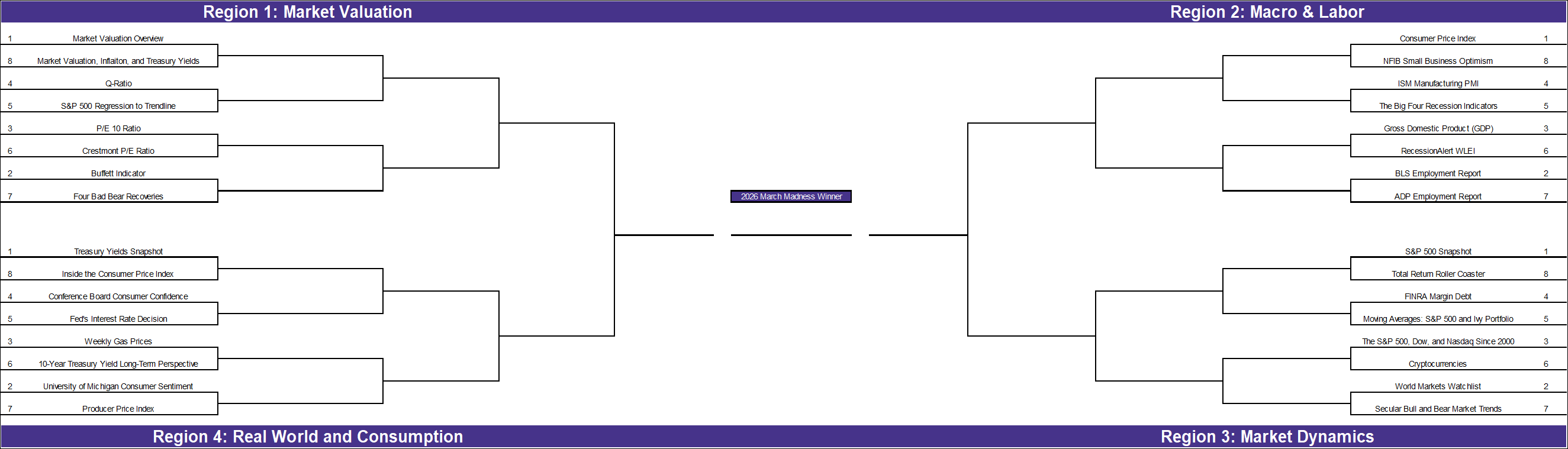

With the NCAA tournament beginning in just a few days, we’ve applied the bracket format to our own research. While economic theory often dictates what should be most important to investors, our reader engagement reveals which topics truly commanded investor attention over the past year.

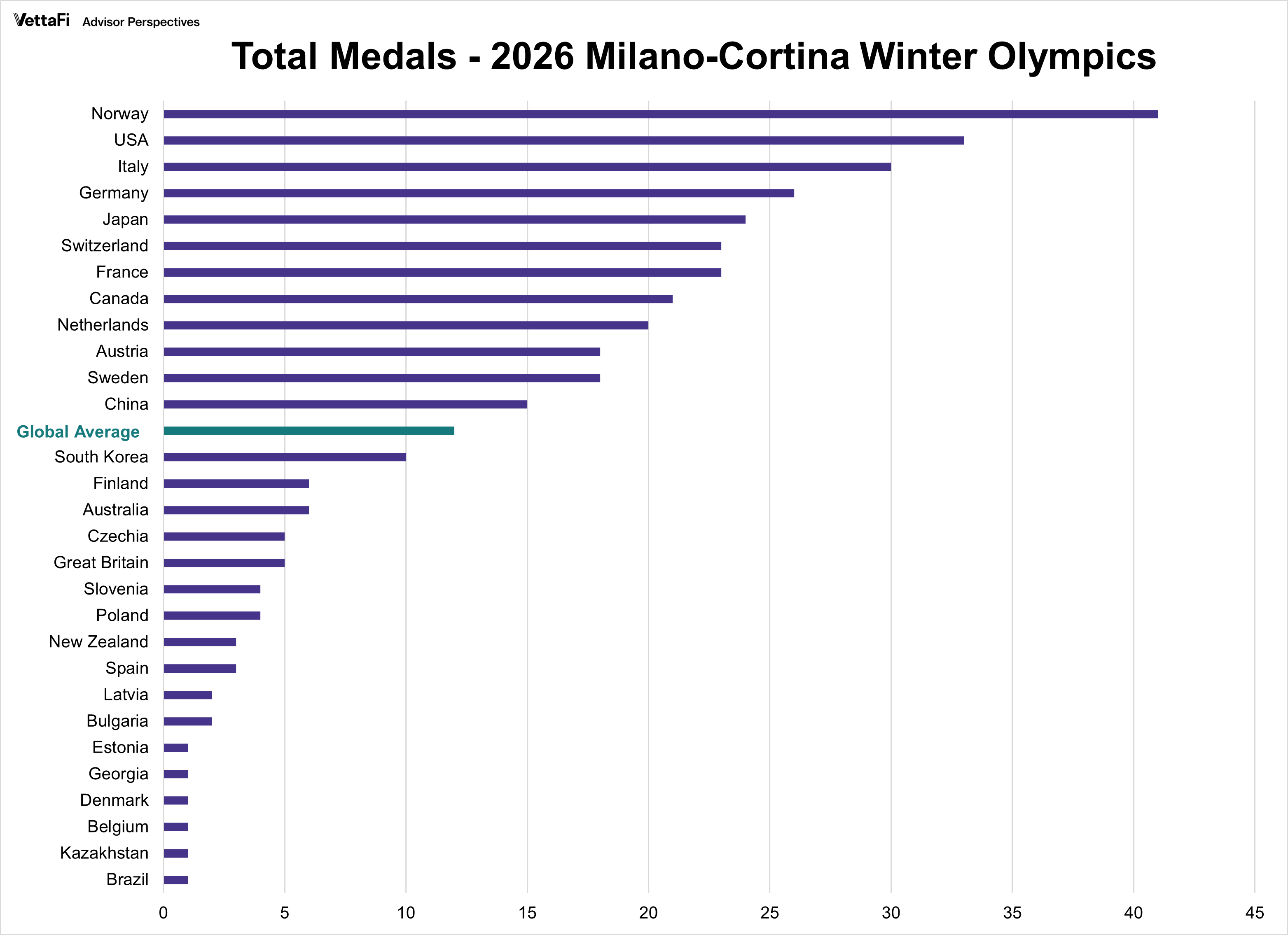

The Milano-Cortina 2026 Winter Games concluded with a familiar hierarchy at the top of the medal table. But in the world of economic indicators, we rarely look at totals without normalizing for scale. The 2026 Winter Games are no different.

The U.S. economy sent conflicting signals last week as a sharp deceleration in growth collided with unexpectedly stubborn inflation.

The U.S. economy began 2026 with a display of unexpected resilience in the labor market and cooling inflation.

The U.S. labor market showed further signs of cooling last week as private sector hiring slowed and job openings reached their lowest levels in over five years.

The final week of January saw a stark divergence between official policy and the American consumer's outlook. While the Federal Reserve maintained a "solid" view of economic growth, the public’s mood plummeted to a decade-low as sticky amid sticky wholesale inflation.

The U.S. economy continues to display a complex mix of resilience and persistence. As markets brace for next week’s FOMC meeting, this snapshot breaks down the latest shifts in GDP, inflation, and consumer behavior.

As the second half of January begins, the U.S. economy presents a picture of cooling inflation and resilient consumer activity.

This video looks at the long term trends of household net worth using the Q3 2025 Z.1 release from the Federal Reserve.

Now that 2025 has come to an end, let’s take a look at the top 10 most-read charts of the year.

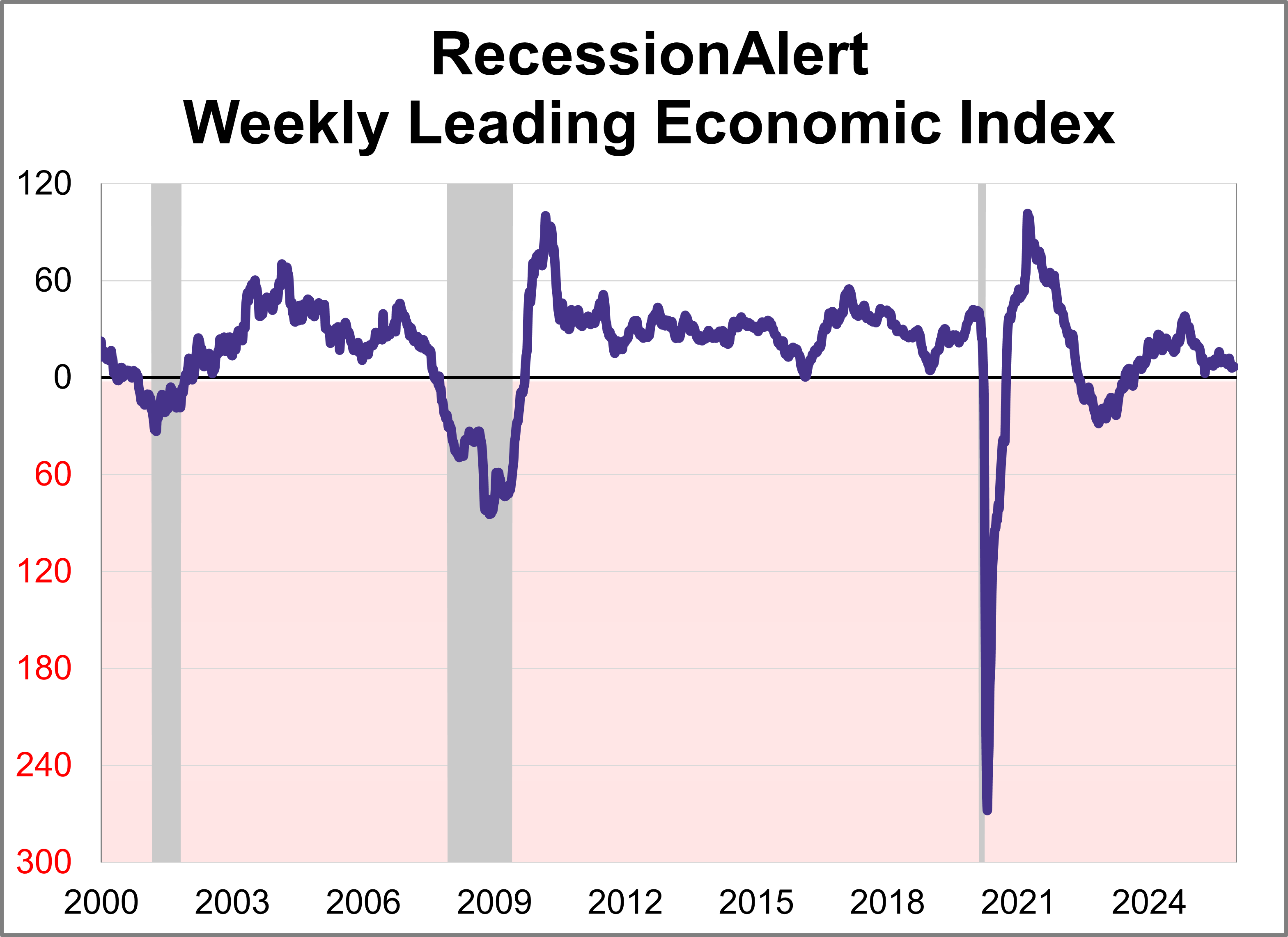

The weekly leading economic index (WLEI) is a composite for the U.S economy that draws from over 20 time-series and groups them into the following six broad categories which are then used to construct an equally weighted average. As of December 12th, the index was at 6.71 with 3 of the 6 components in expansion territory.