The big economic number tomorrow will be the Q2 Third Estimate for GDP. The last two quarters are behind us with their real annualized rates of 2.9% in Q4 2017 and 2.3% in Q1. What do economists see in their collective crystal ball for Q2 Third Estimate? Let's take a look at the latest GDP forecasts from the latest Wall Street Journal survey of economists conducted earlier this month.

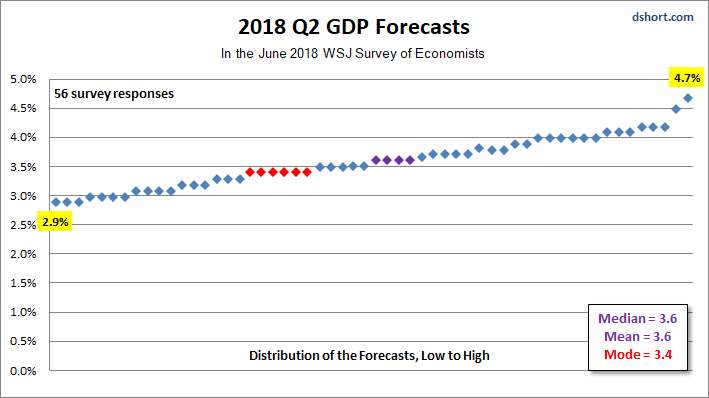

Here's a snapshot of the full array of WSJ opinions about Q2 GDP with highlighted values for the median (middle), mean (average) and mode (most frequent). In the latest forecast the median and mean are identical at 3.6%. The mode was skewed fractionally lower at 3.4% forecast by 6 of the 56 respondents -- that's just about eleven percent of them.

Also of interest is the Atlanta Feds' GDPNow™ forecasting model, which currently puts Q2 GDP at 4.7% as of June 19th, a very high and optimistic estimate in comparison.

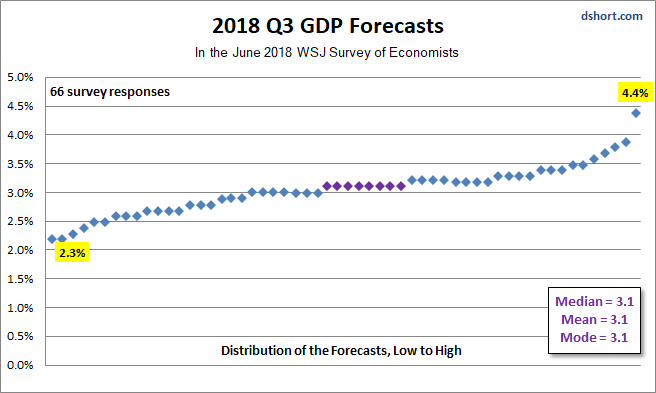

Looking Ahead at Q3 GDP

Tomorrow's release of the Third Estimate for Q2 GDP is, of course, a rear-view mirror look at the economy. The WSJ survey also asks the participants to forecast Q3 GDP.

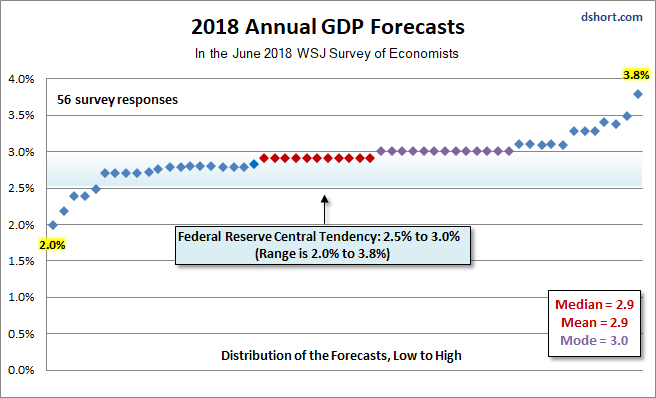

Expectations for Annual GDP

As for the WSJ forecasts for 2018 annual GDP, here is the latest, along with the Fed's economic projection for annual GDP.

Most WSJ survey participants see 2018 ending at a growth rate of 3.0%. Even the most pessimistic of the lot sees 2.0% for the 2018 year-end print, and the median and mean are forecasting 2.9%.

GDP: A Long-Term Historical Context

For a broad historical context for the latest forecasts, here a snapshot of GDP since Uncle Sam began tracking the data quarterly in 1947.

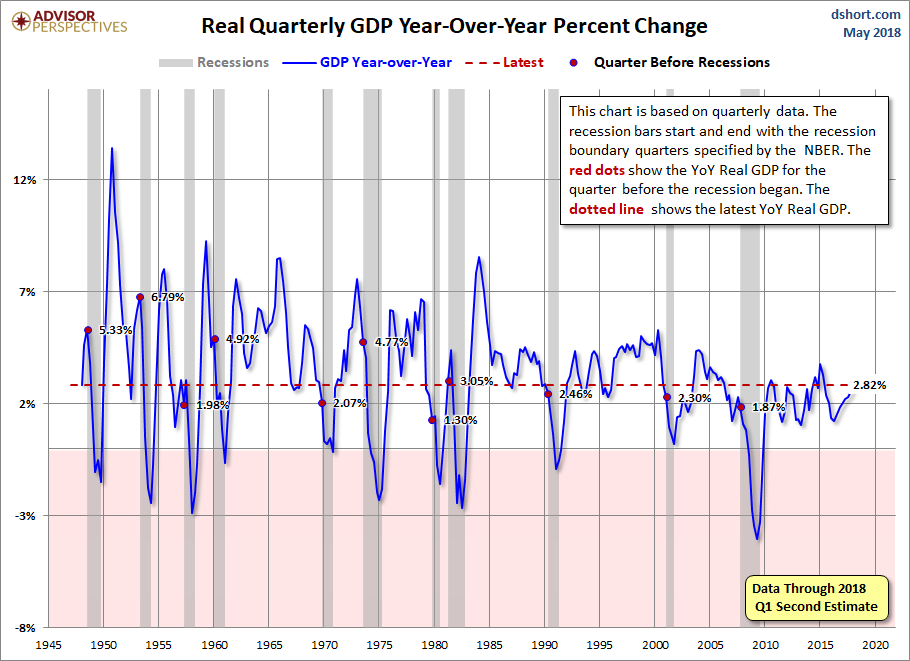

A More Intuitive Look at Quarterly GDP

Let's take one more look at quarterly GDP -- the year-over-year percent change, which is certainly more intuitive than the conventional practice of the Bureau of Economic Analysis of calculating GDP by compounding the quarterly percent change at annual rates (which they explain here). Consider: the four quarters of 2017 GDP using the BEA's preferred method are 1.2%, 3.1%, 3.2% and 2.9%. The year-over-year change in the three quarters is a much less attention-grabbing 2.0%, 2.2%, 2.3% and 2.6%. However, when we use the more intuitive percent change from a year ago, we get a long-term perspective on where we are in the grand scheme of things, one the more closely resembles the regression in the chart above.

Tomorrow we'll find out how the latest Q1 forecasts stack up against the BEA's Third Estimate of the real thing.