We have been asked to stop republishing ECRI data by the organization. Stay tuned while we find a way to resume!

This article was originally written by Doug Short. From 2016-2022, it was improved upon and updated by Jill Mislinski. Starting in January 2023, AP Charts pages will be maintained by Jennifer Nash at Advisor Perspectives/VettaFi.

Today's release of the publicly available data from ECRI puts the WLI at 145.6, up from the previous week's figure. The WLIg is at -10.3, up from last week and the WLI YoY is at -4.92%, down slightly from last week.

Below is a chart of ECRI's smoothed year-over-year percent change since 2000 of their weekly leading index.

Appendix: A Closer Look at the ECRI Index

The first chart below shows the history of the Weekly Leading Index and highlights its current level.

For a better understanding of the relationship of the WLI level to recessions, the next chart shows the data series in terms of the percent-off the previous peak. In other words, new weekly highs register at 100%, with subsequent declines plotted accordingly.

As the chart above illustrates, only once has a recession ended without the index level achieving a new high -- the two recessions, commonly referred to as a "double-dip," in the early 1980s. We've exceeded the previously longest stretch between highs, which was from February 1973 to April 1978. But the index level rose steadily from the trough at the end of the 1973-1975 recession to reach its new high in 1978. The pattern in ECRI's indictor is quite different, and this has no doubt been a key factor in their business cycle analysis.

The WLIg Metric

The best known of ECRI's indexes is their growth calculation on the WLI. For a close look at this index in recent months, here's a snapshot of the data since 2000.

Now let's step back and examine the complete series available to the public, which dates from 1967. ECRI's WLIg metric has had a respectable record for forecasting recessions and rebounds therefrom. The next chart shows the correlation between the WLI, GDP, and recessions.

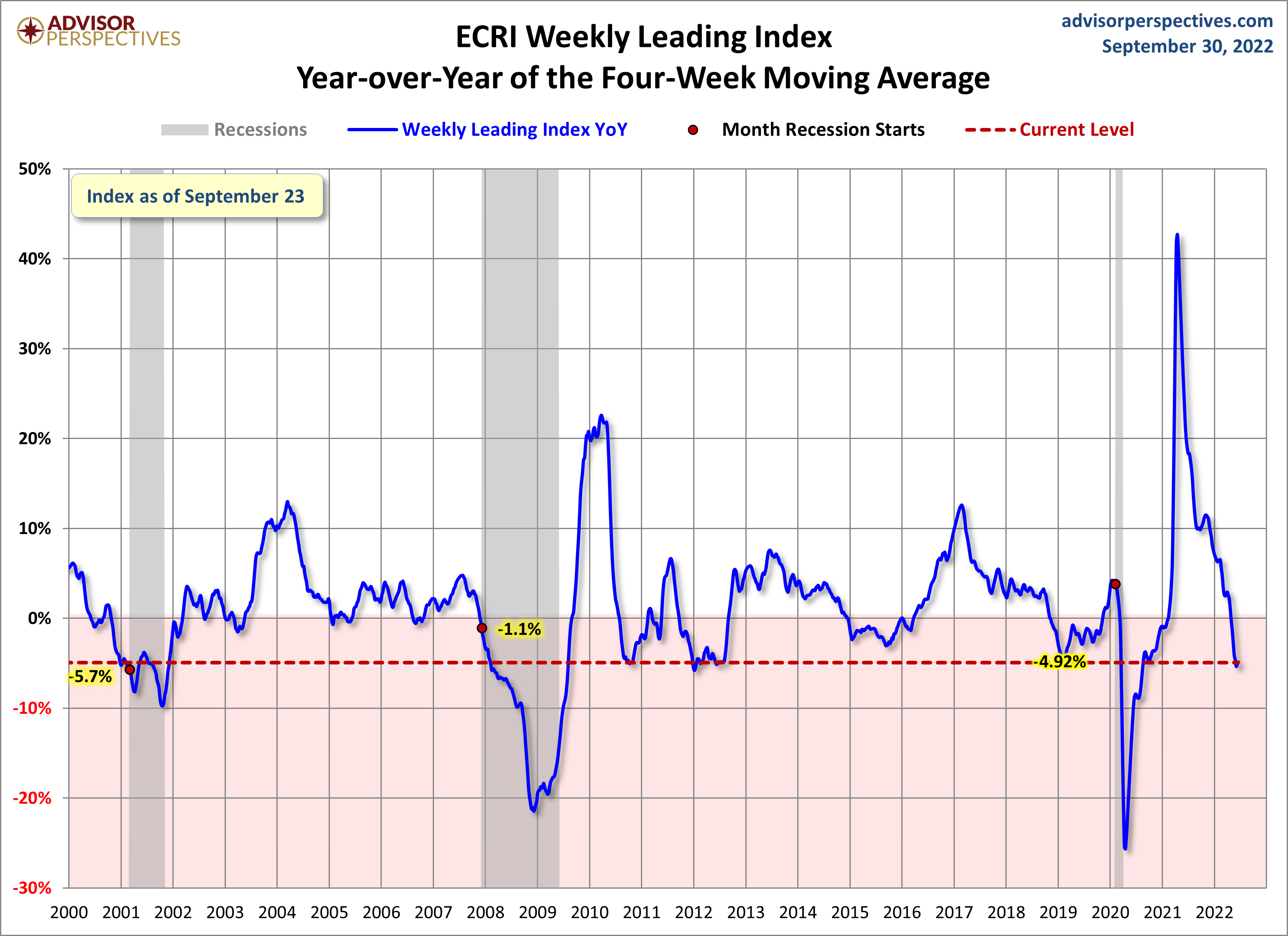

Year-over-Year Growth in the WLI

Here is a snapshot of the year-over-year growth of the WLI rather than ECRI's previously favored method of calculating the WLIg series from the underlying WLI (see the endnote below). Specifically, the chart immediately below is the year-over-year change in the 4-week moving average of the WLI. The red dots highlight the YoY value for the month when recessions began.

The WLI YoY is at -4.92%, down slightly from last week. The latest level is higher than at the start of two of the last eight recessions.

Note: How to Calculate the Growth series from the Weekly Leading Index

ECRI's weekly Excel spreadsheet includes the WLI and the Growth series, but the latter is a series of values without the underlying calculations. After a collaborative effort by Franz Lischka, Georg Vrba, Dwaine van Vuuren and Kishor Bhatia to model the calculation, Georg discovered the actual formula in a 1999 article published by Anirvan Banerji, the Chief Research Officer at ECRI: " The three Ps: simple tools for monitoring economic cycles - pronounced, pervasive and persistent economic indicators."

Here is the formula:

"MA1" = 4 week moving average of the WLI

"MA2" = moving average of MA1 over the preceding 52 weeks

"n"= 52/26.5

"m"= 100

WLIg = [m*(MA1/MA2)^n] - m

Read more updates by Jen Nash