Key takeaways

- Pension surplus can create strategic value beyond full funding, supporting future retirement benefits and broader organizational objectives.

- A surplus glidepath balances liability protection with growth by investing surplus assets differently once a plan is comfortably overfunded.

- Any surplus strategy should preserve benefit security first, with additional risk taken only on assets above a defined surplus threshold.

Historically, many in the pension industry viewed funding above the "plan termination level" as having little incremental value. Once a plan reached “plan termination level”, thought of as roughly 110% funding, conventional wisdom suggested additional surplus had little economic value because it is effectively "trapped capital." If excess assets cannot be readily used by the sponsor, why continue taking investment risk?

See more: The Case for Active Small Caps

However, when broader retirement objectives and long-term benefit security are factored, we believe this assumption deserves reconsideration.

Sprouts of industry change

Recent developments have made questions around funding levels more relevant. IBM and Kodak offer examples of how sponsors are beginning to rethink pension surplus. IBM replaced its 401(k) matching contribution beginning in 2024 with a cash balance benefit funded through its reopened defined benefit (DB) plan, while Kodak focused on terminating its overfunded U.S. pension plan and using surplus asset after obligations were satisfied.

For IBM, this shift appears to have contributed to a meaningful change in investment strategy, with fixed income falling from more than 80% of plan assets to roughly 55% over two years. The portfolio is no longer focused solely on locking down liabilities; it appears designed to support surplus growth.

Potential legislation adds another dimension. The Strengthening Benefits Plans Act of 2025 would allow certain DB surplus transfers to defined contribution (DC) plans under specified conditions. That does not make surplus freely available, and while the details matter, it makes the old “trapped capital” assumption less absolute.

These developments point to a broader shift in how sponsors may think about pension assets. Rather than viewing surplus solely as a funding milestone, some organizations are beginning to consider how excess assets might support future retirement benefits, workforce objectives, or broader capital allocation decisions.

From de-risking glidepaths to surplus glidepaths

De-risking glidepaths have been industry standard for years. The basic idea is straightforward: as funded status improves, the plan reduces return-seeking assets and increases liability-hedging assets. This approach offers a smoother landing to a fully funded position without taking excessive risk for plan sponsors determined to hibernate or terminate.

But once we assume that pension surplus has tangible value beyond plan termination funding, the story changes. For sponsors that have spent years improving funded status, reaching a meaningful surplus can create a new set of strategic questions. The investment framework that helped close a funding gap may not be the same framework best suited for managing excess assets once that goal has been achieved.

For overfunded plans, particularly those that are frozen (i.e., no future benefit accruals), risk tolerance may increase as surplus grows. A plan that de-risked as funded status improved may eventually begin to re-risk once a sufficient surplus cushion has been built. We call this a surplus glidepath.

Surplus investing can be thought of as a bifurcated portfolio: the liability-hedging assets continue to protect the benefit promise, while the surplus assets can be managed with a more total-return mindset. The objective is not to abandon liability driven investing (LDI). Rather, it is to preserve the core liability hedge while recognizing that surplus dollars may have a different risk/reward profile than assets needed to secure promised benefits.

Why the risk/reward trade-off changes

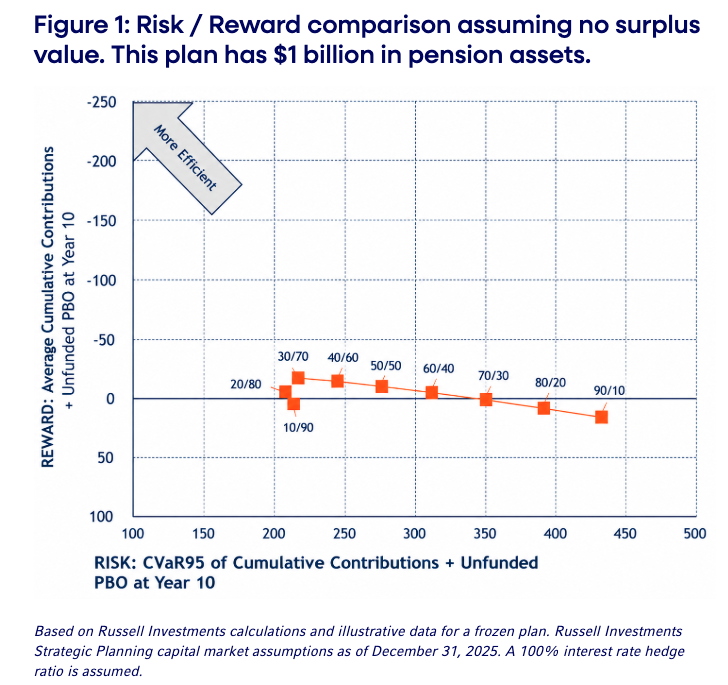

Consider a plan that is 110% funded. If we assume no value to surplus then the most efficient portfolio (when minimizing contributions and downside funded status) will usually be one that preserves funded status with limited additional risk. As shown in Figure 1, we consider the total cumulative contributions to reach full funding as a measurement of portfolio efficiency. On that basis, the optimal portfolio would be a 20/80 (i.e., 20% return-seeking, 80% liability-hedging) or 30/70 since the surplus upside is ignored while the downside remains very real.

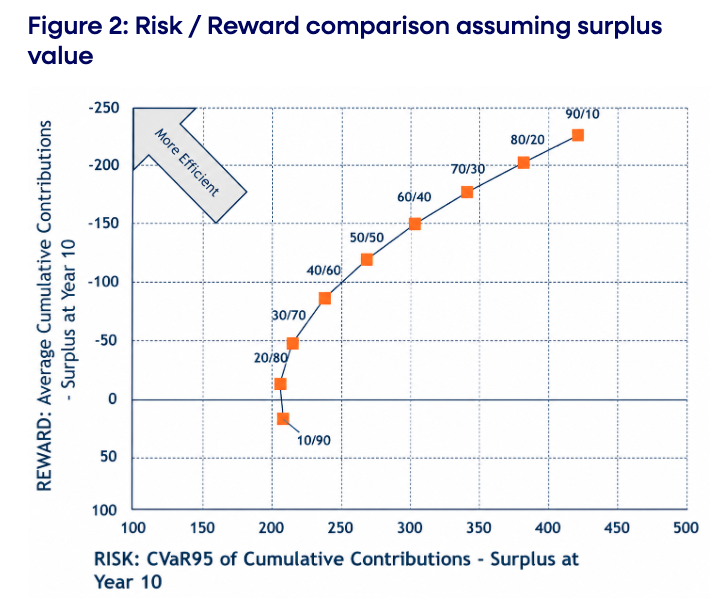

However, if surplus is assumed to have full value, the risk/reward trade-off changes as the metric that matters shifts to include the value of future surplus as an offset to contributions paid. The downside risk does not disappear, but higher allocations to return-seeking assets may offer meaningful upside. As funded status improves further, that tradeoff becomes more apparent, as shown in Figure 2. Note that we assume 100% utility in the surplus. This analysis could be adjusted to account for a smaller portion (e.g., 50% after tax reversion).

The key point is not that overfunded plan sponsors should simply turn risk back on. Rather, higher allocations to return-seeking assets may become more efficient uses of capital when surplus has economic value. From a plan sponsor perspective, this could mean additional flexibility for a variety of potential uses, including re-opening the DB plan, funding new benefits, or potentially funding DC nonelective contributions if legislation allows. For some of these uses, like offering new benefits, the surplus is 100% useable. For other cases – like after-tax asset reversions post-plan termination – the utility will be lower.

What a surplus glidepath might look like

In practice, a surplus glidepath may resemble a valley-shaped policy. Return-seeking exposure declines as the plan moves from underfunded to fully funded, then begins to rise modestly once a meaningful surplus cushion has been established.

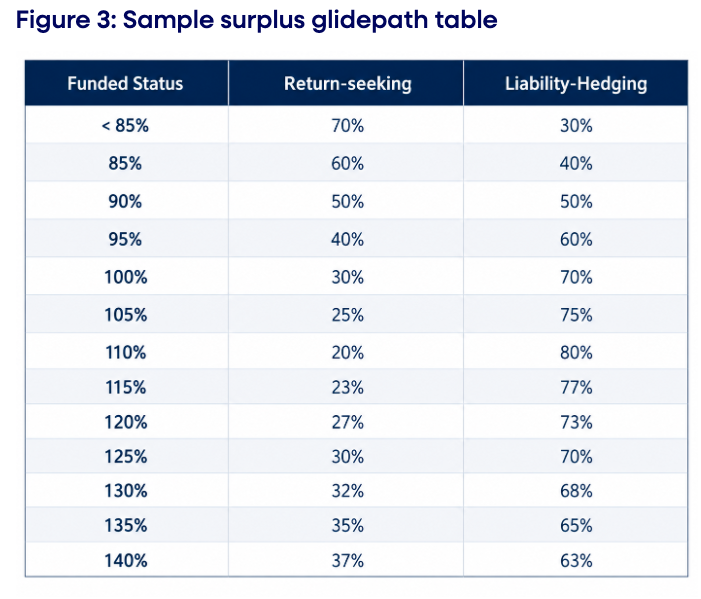

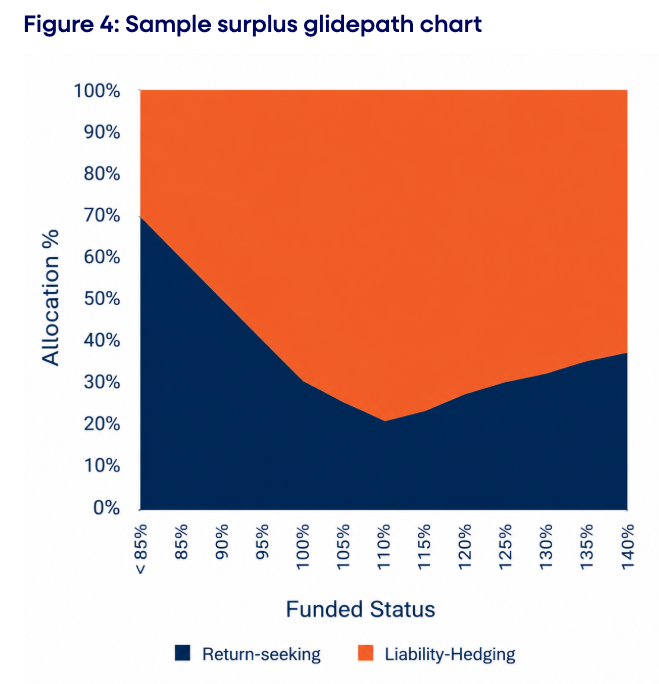

For example, a plan might reduce return-seeking assets from 70% at a funded status below 85%, to 20% at 110% funded. From there, the glidepath may evolve as LDI assets are held equal to liabilities, and any assets in excess are treated from an asset-only lens. Assuming all those assets are return seeking, the exposure gradually increases, as shown in Figures 3 and 4.

The logic is intuitive. When the plan is underfunded, the sponsor needs return potential to close the gap. As the deficit shrinks, preserving funded status becomes more important. But once the plan has a meaningful surplus, the plan may be able to take additional risk with surplus assets while still maintaining a strong liability hedge.

Many variations in this concept are possible. Sponsors may treat surplus assets in a more diversified manner (e.g., 60/40 portfolio) given the goals for using the surplus. Or they might consider a full liability hedge (i.e., 100% hedge ratio) sufficient even if the dollar amount of LDI assets does not equal the liabilities. The portfolio ought to be structured to meet the plan sponsor’s needs. We will explore these possibilities further in future pieces.

Through surplus investing, we are not rejecting the concept of de-risking. In fact, we are taking a more holistic view of risk by acknowledging risk tolerance changes as funded status improves. And this change does not necessarily stop once the plan is funded to plan termination levels.

Prudent re-risking

The term “re-risking” is convenient, but it can be misleading. It should not imply that participant benefits are being put in jeopardy. The plan assets exist first and foremost for “providing benefit to participants and their beneficiaries”, and any surplus strategy should begin with that fiduciary foundation.

For that reason, we advocate for prudent liability hedging. Any increased allocation to return-seeking assets should occur only after the plan has reached a clearly defined surplus threshold, and it should be implemented incrementally. The sponsor should also maintain sufficient assets to adequately hedge liability-related risks under a range of market environments.

This distinction matters. Surplus investing is about recognizing the need to secure accrued benefits; then assets above that level may have different roles in the overall strategy.

Dual objective portfolios?

At first glance, surplus investing appears to create a dual-objective portfolio: one objective for participants and another for the sponsor. That framing should be handled carefully.

In practice, the objective remains rooted in participant benefit security. The discussion is not whether to protect accrued benefits, but how to thoughtfully manage assets that may exist above the level required to support those obligations.

Asset allocation decisions are fiduciary functions. Fiduciaries are responsible for acting in the best interest of participants and their beneficiaries. Incidental benefits to the sponsor may be permissible, but not at the expense of the plan participants. A well-designed surplus strategy should therefore begin by preserving benefit security through a robust liability hedge, then consider how surplus assets might be invested.

The practical implementation should be disciplined. For example, sponsors should define the surplus threshold (e.g., 110% funded), an interest rate risk hedge target (e.g., 100%), a surplus glidepath, liquidity needs, etc. These decisions should be well-documented.

Surplus investing

We envision that a surplus portfolio would be a well-diversified blend of asset classes, prioritizing investments that offer attractive risk-adjusted returns. The focus of the allocations would be on return-seeking assets, including public equities, high yield fixed income, listed real assets, and select hedge fund strategies.

Sponsors should prioritize well-managed volatility over the highest growth possible. Private assets, such as real estate and private credit, can be important additions for plans with longer time horizons. However, allocations to less liquid investments should be sized carefully, particularly for plans that may use surplus for benefit enhancement, DC contributions, risk transfer or eventual plan termination. In that sense, the surplus portfolio should be growth-oriented, but not unconstrained.

Pension investor implications

For years, the pension industry treated surplus as having limited strategic value. That view made sense when surplus was assumed to offer little practical benefit beyond securing accrued obligations.

Today, however, several developments are prompting sponsors to revisit that assumption. Funded status has improved across much of the defined benefit landscape, some sponsors are exploring new ways to utilize pension surplus, and policymakers are considering whether surplus assets could play a broader role in supporting retirement benefits.

That does not eliminate fiduciary constraints, but it does suggest traditional de-risking glidepath may not be the end of the story. If pension surplus has value, sponsors should consider whether their investment policy reflects that value. For some plans, the answer may still be hibernation or termination. For others, a surplus glidepath may offer a more flexible framework: lock down the benefits promised, then grow surplus assets with a prudent process and disciplined understanding of risk.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

The information, analyses and opinions set forth herein are intended to serve as general information only and should not be relied upon by any individual or entity as advice or recommendations specific to that individual entity. Anyone using this material should consult with their own attorney, accountant, financial or tax adviser or consultants on whom they rely for investment advice specific to their own circumstances.

Products and services described on this website are intended for United States residents only. Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained on this website should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional. Persons outside the United States may find more information about products and services available within their jurisdictions by going to Russell Investments' Worldwide site.

Russell Investments is committed to ensuring digital accessibility for people with disabilities. We are continually improving the user experience for everyone, and applying the relevant accessibility standards.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates Management, L.P., with a significant minority stake held by funds managed by Reverence Capital Partners, L.P. Certain of Russell Investments' employees and Hamilton Lane Advisors, LLC also hold minority, non-controlling, ownership stakes.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

© Russell Investments Group, LLC. 1995-2026. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

© Russell Investments

Read more commentaries by Russell Investments