Key takeaways

- A more complex market backdrop is creating a stronger case for active U.S. small cap investing.

- Structural inefficiencies in small caps continue to create opportunities for active stock selection.

- A diversified multi-manager approach can improve diversification and reduce implementation risk.

A new market regime

For much of the last decade, investing felt relatively one dimensional. Falling inflation, near zero interest rates and abundant liquidity rewarded long duration growth assets, compressed dispersion and made passive exposure difficult to challenge.

See more: Execution Efficiency Redefines Fixed Income Transitions

Today, markets are facing a more complicated regime where economic growth remains resilient, inflation proves sticky and interest rates may stay structurally higher for longer. Equity markets and bond yields have risen together at various points, creating a backdrop that can feel contradictory relative to traditional market playbooks.

However, that combination may not be as unusual as it first appears.

Constructive conditions for small caps

When rates rise because growth expectations are improving, equities can often perform well alongside higher yields. Strong nominal GDP growth, resilient labor markets and improving earnings expectations can offset some of the valuation pressure associated with higher discount rates. At the same time, persistent inflation and geopolitical uncertainty have increased the likelihood that policy rates remain elevated relative to the prior decade.

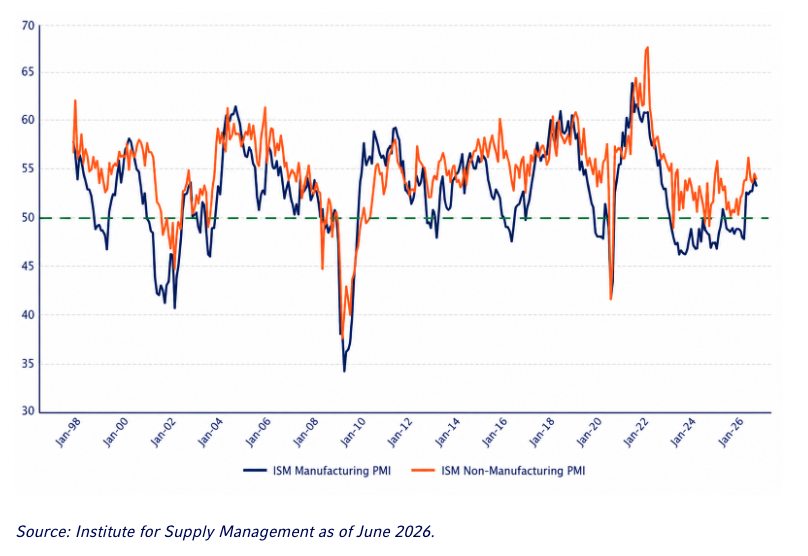

Several macro indicators that have historically been associated with stronger small cap performance also remain constructive. ISM manufacturing and non-manufacturing surveys continue to signal expansionary conditions, small business optimism remains above levels seen through much of 2021 to 2024, and both high yield credit spreads and equity volatility measures have remained relatively contained despite heightened geopolitical uncertainty. While risks remain, the broader macro backdrop continues to support domestic economic resilience rather than recessionary conditions.

That shift may matter more for small caps than many investors appreciate.

Expansionary market conditions

A changing backdrop for small caps

Small cap equities have historically provided differentiated exposure to domestic economic activity, innovation cycles and earlier stage business models that are often underrepresented in large cap indices increasingly dominated by a narrow group of mega cap companies.

At the same time, the opportunity set within public markets has evolved. Companies are remaining private longer than in prior decades, leading some investors to question whether small caps should still represent a strategic allocation within diversified portfolios.

In our view, the public small cap universe remains both economically relevant and structurally inefficient. Thousands of businesses continue to operate across highly specialized industries and niche end markets, many receiving limited institutional attention despite meaningful exposure to important areas of the economy.

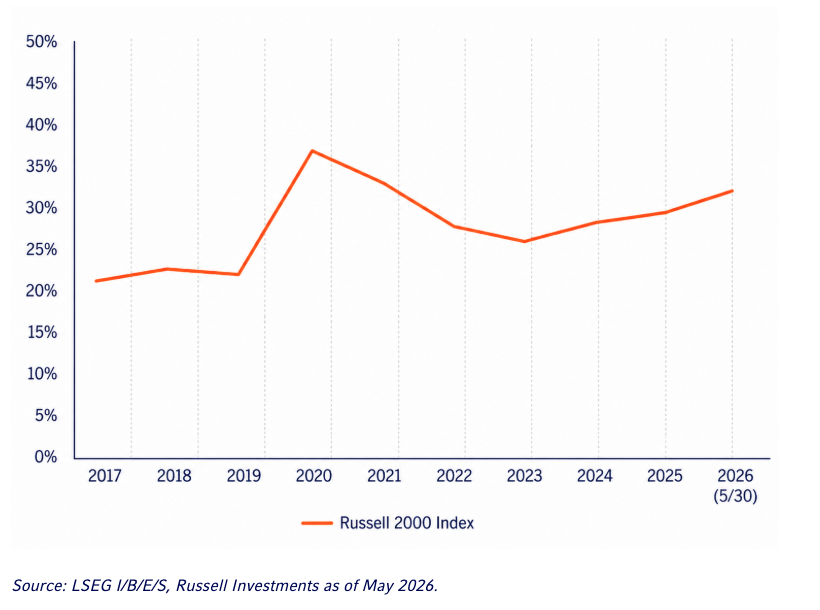

The Russell 2000 Index itself contains a wide range of businesses, from profitable niche leaders and innovative disruptors to companies with weak profitability and meaningful financing needs. A meaningful portion of the index currently consists of unprofitable companies, while many small cap firms maintain greater floating rate debt exposure than their large cap peers.

Unprofitable company exposure (%)

If inflation remains persistent and markets continue to reprice toward a higher for longer rate environment, financing flexibility and balance sheet quality may matter more than they did during the prior cycle. Broad index exposure may not fully distinguish between businesses positioned to benefit from this environment and those more vulnerable to elevated financing costs.

In our view, that does not weaken the case for small caps. Rather, it strengthens the case for active selectivity.

Structural inefficiencies remain compelling

Beyond the macro backdrop, small cap equities continue to exhibit structural inefficiencies that may favor active stock selection.

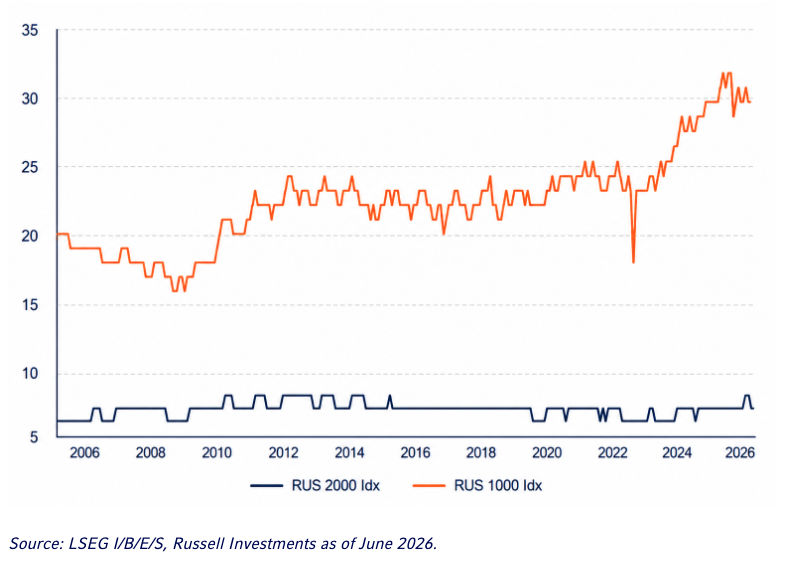

The imbalance in sell side research coverage is striking. While the average number of analysts following Russell 1000 companies has grown to roughly 30 analysts, coverage of Russell 2000 companies has stagnated over the past couple of decades. That means many small cap businesses operate with a fraction of the institutional scrutiny afforded to their large cap peers. In markets where information is less efficiently disseminated, diligent fundamental research can provide a meaningful informational advantage, allowing active managers to uncover opportunities that passive investors and broader market consensus may overlook.

Average number of IBES earnings estimates

At the same time, smaller companies tend to experience higher levels of stock specific volatility. In periods of macro uncertainty or rapid factor rotation, smaller companies can experience sharp price movements that are not always fully supported by changes in fundamentals. For experienced active managers, those dislocations can create opportunities to add value through disciplined security selection and opportunistic portfolio repositioning.

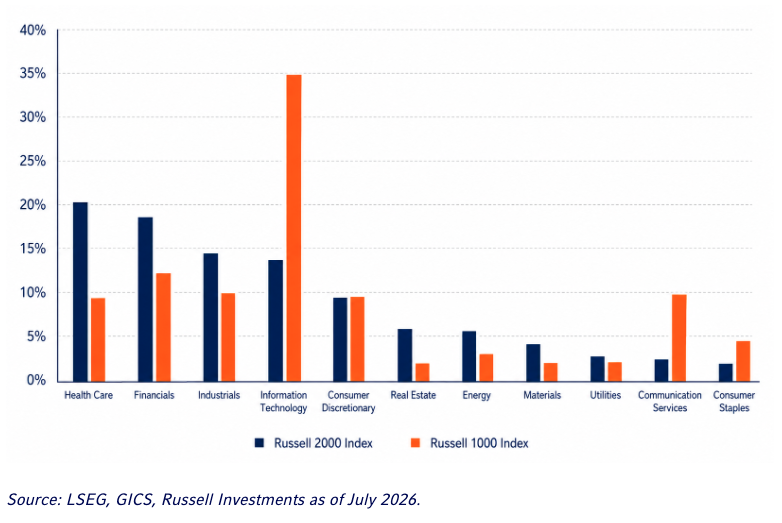

The opportunity set itself also remains highly differentiated. Beneath the surface of the small cap universe are businesses exposed to some of the most dynamic areas of the economy, including: energy infrastructure modernization, semiconductor supply chain expansion, biotechnology innovation, digital industrial automation and specialized transportation networks that support reshoring, industrial investment and the movement of goods across the U.S. economy.

These trends increasingly align with a market environment that appears to be shifting from concentration toward broader competition across sectors, industries and regions.

Sector diversification

Why implementation matters as much as allocation

One challenge investors often face in small caps is that manager outcomes can vary significantly depending on style, market capitalization focus and market regime. A single manager may provide only partial exposure to the broader small cap opportunity set, while also introducing meaningful substyle or manager specific risk.

A diversified multi-manager structure can help reduce reliance on any single investment approach while improving access to a broader opportunity set across quality, value, growth and micro-cap segments. Dedicated micro-cap exposure may further enhance diversification by accessing companies that often receive even less institutional coverage and may offer greater potential for idiosyncratic alpha generation.

Importantly, many active small cap strategies have gradually migrated up market over time. As of May 2026, the weighted average market capitalization of the Morningstar Small Blend category was approximately $7.7 billion versus $3.14 billion for the Russell 2000 Index. In our view, maintaining exposure across the full breadth of the small and micro-cap opportunity set may be an important competitive advantage in a market where inefficiencies remain most pronounced further down the capitalization spectrum.

Specialized sector expertise can also be valuable. For example, small cap health care companies and specifically biotechnology stocks are often driven less by broad market direction and more by company specific developments such as clinical trial outcomes, regulatory decisions and pipeline innovation. Skilled specialist managers may be better positioned to identify opportunities created by temporary dislocations, misunderstood science or overly pessimistic sentiment.

A more favorable backdrop for active management?

One defining characteristic of the post financial crisis era was unusually low dispersion across many areas of the market. Macro liquidity conditions often overwhelmed company fundamentals, making passive exposure increasingly difficult to outperform.

However, going forward, economic resilience, persistent inflation, regionalization, infrastructure investment and the continued buildout of AI related capacity are creating a broader and more competitive market backdrop. These could drive leadership to widen beyond the narrow group of companies that dominated much of the previous cycle.

If market leadership continues to broaden and dispersion across companies and sectors increases, smaller cap, higher quality and more valuation conscious strategies may be increasingly well-positioned. In our view, the combination of structural inefficiencies, differentiated business models and a wider range of potential market winners may create a more supportive environment for active management than investors experienced during much of the prior decade.

Investor implications

For investors seeking exposure to U.S. small caps, the question may no longer simply be whether to allocate to the asset class, but how to access the full breadth of the opportunity set while managing style and implementation risk.

In our view, a diversified active multi-manager approach that combines complementary styles, differentiated micro-cap exposure and specialized sector expertise may offer a compelling way to navigate a more complex market regime.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

The information, analyses and opinions set forth herein are intended to serve as general information only and should not be relied upon by any individual or entity as advice or recommendations specific to that individual entity. Anyone using this material should consult with their own attorney, accountant, financial or tax adviser or consultants on whom they rely for investment advice specific to their own circumstances.

Products and services described on this website are intended for United States residents only. Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained on this website should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional. Persons outside the United States may find more information about products and services available within their jurisdictions by going to Russell Investments' Worldwide site.

Russell Investments is committed to ensuring digital accessibility for people with disabilities. We are continually improving the user experience for everyone, and applying the relevant accessibility standards.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates Management, L.P., with a significant minority stake held by funds managed by Reverence Capital Partners, L.P. Certain of Russell Investments' employees and Hamilton Lane Advisors, LLC also hold minority, non-controlling, ownership stakes.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

© Russell Investments Group, LLC. 1995-2026. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

© Russell Investments

Read more commentaries by Russell Investments