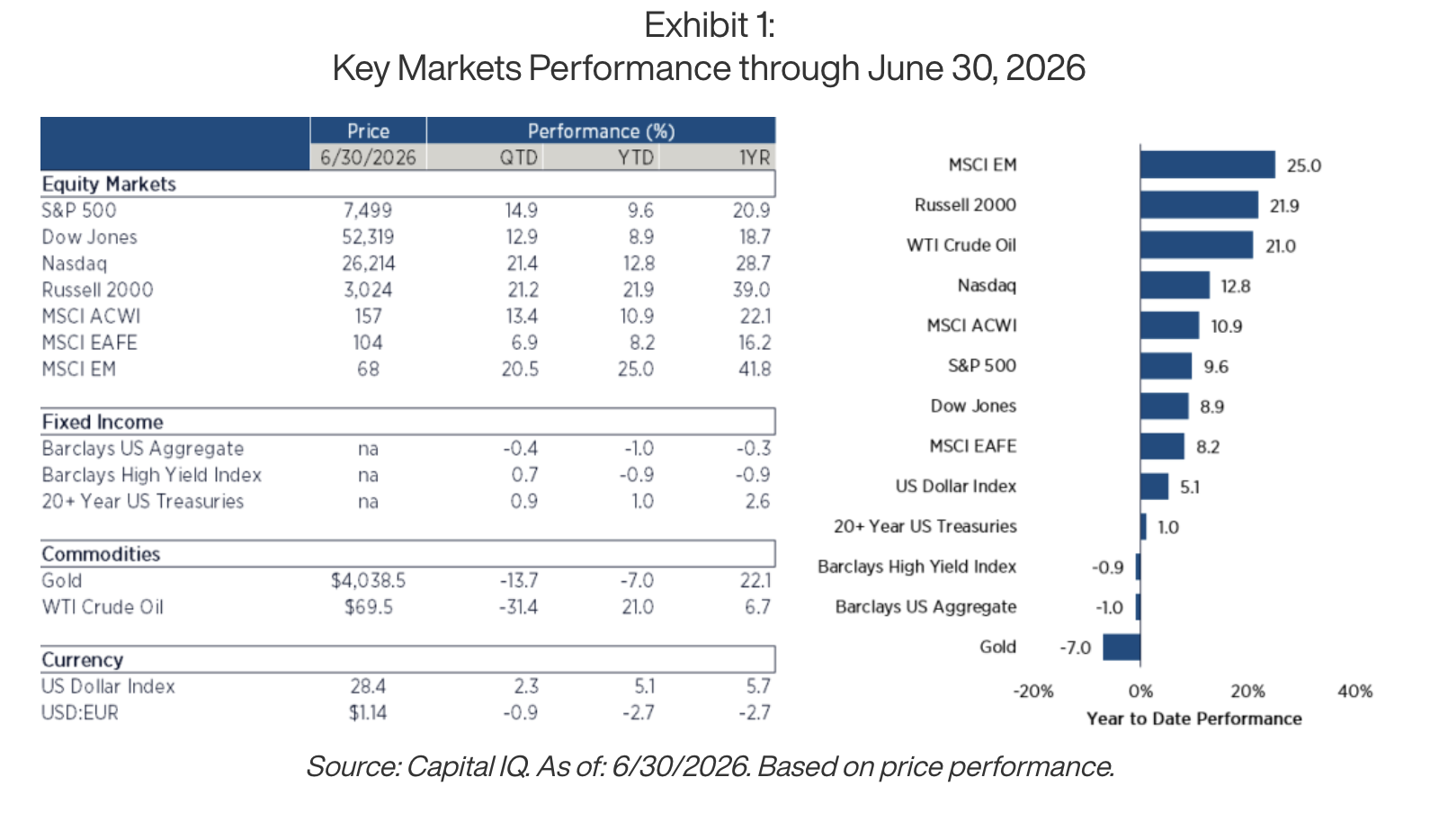

Stocks staged a powerful recovery in Q2. The S&P 500 gained 15% and closed near record highs as oil round-tripped back to pre-conflict levels, AI enthusiasm returned, and the rally broadened well beyond the handful of names that led the market for three years.

KEY POINTS

The Quarter Oil Changed Everything

-

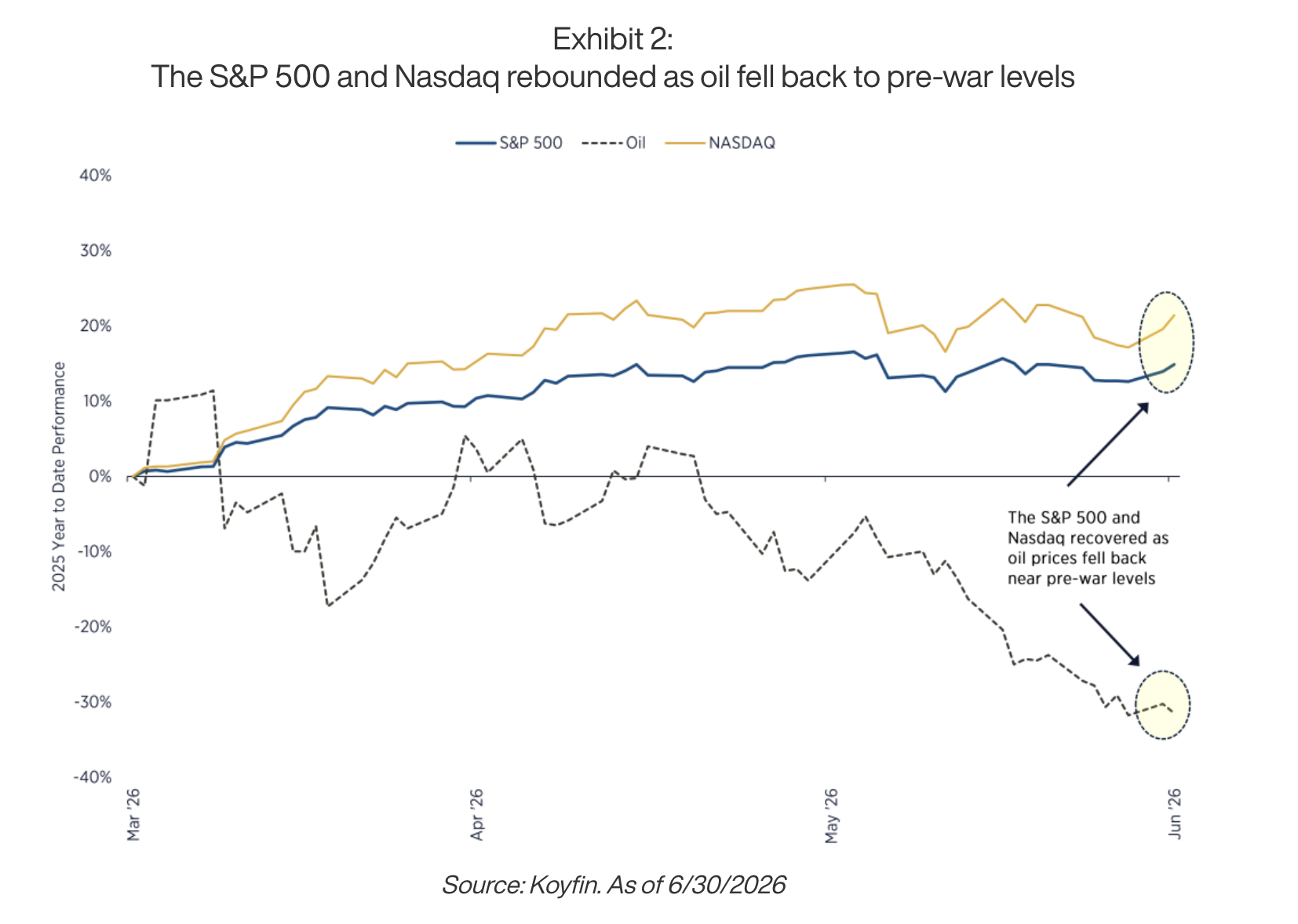

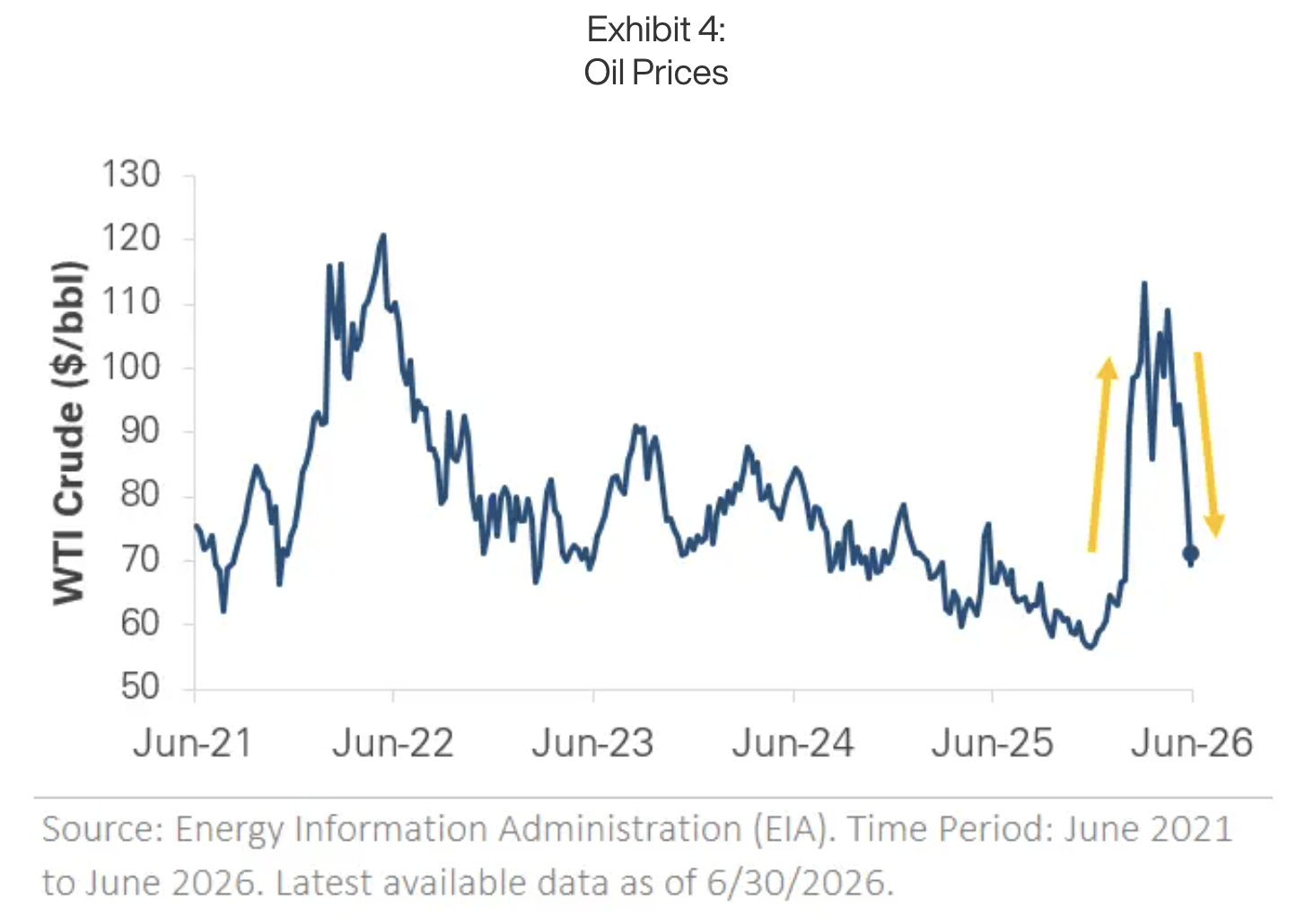

Oil round-tripped. Crude spiked near $115 before falling back to roughly $70 as a ceasefire took hold. The Q1 shock we said would resolve did, and inflation’s main driver is now fading.

-

The Fed flipped. May inflation hit a three-year high of 4.2%, pushing the Fed from cutting to openly weighing a hike. Near-term rate relief hinges on the next two inflation prints.

-

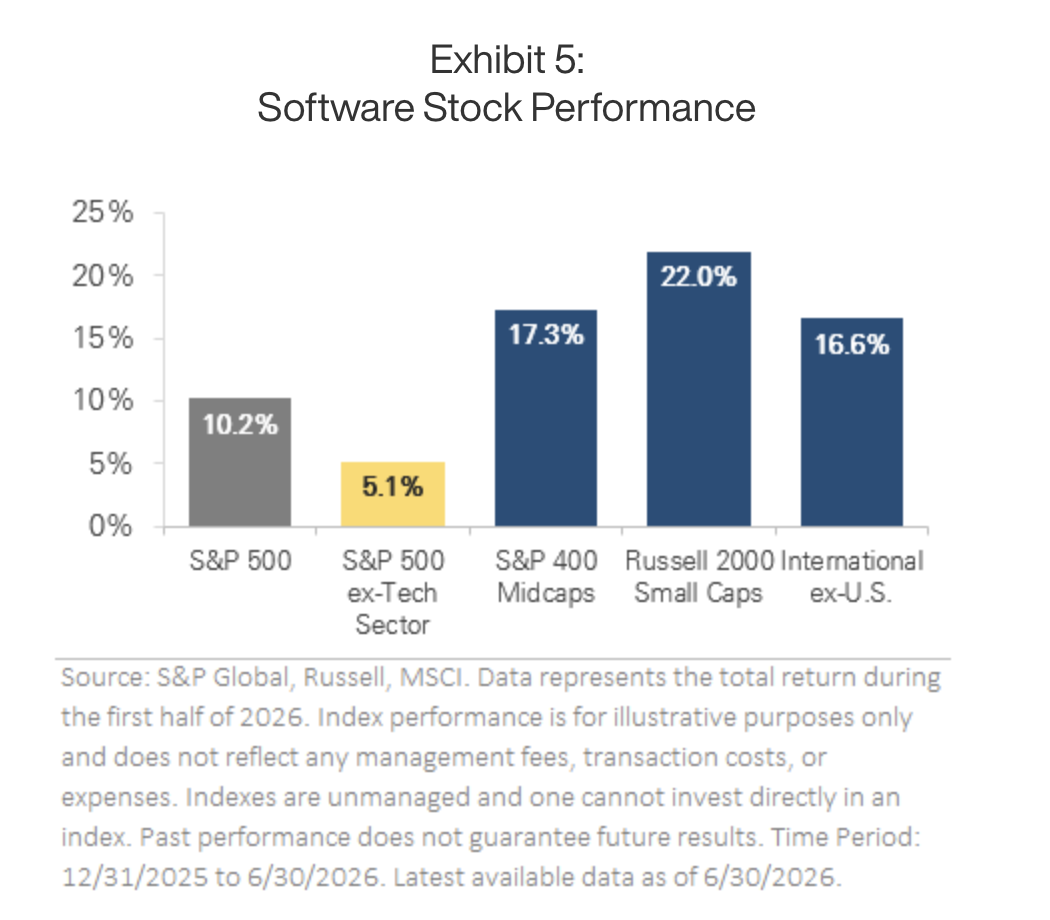

Breadth broadened. Small caps (+22%), mid caps (+17%), and international (+17%) all beat the S&P 500 this year, giving investors a more balanced market that finally rewards diversification over concentration.

-

AI leadership rotated. Semiconductors posted their best quarter in nearly 30 years (+88%), but the gains flowed to memory and picks-and-shovels names while several Mag 7 stocks lagged. The market is now paying for AI payoff, not AI promise.

-

Earnings kept climbing. The companies leading the buildout are reporting record results and growing backlogs. The fundamentals still support the advance, even with expectations running high.

The Other Side of the Shock

Last quarter we wrote that the oil shock looked like a geopolitical event working through valuations rather than a fundamental breakdown, and that those tend to resolve. One quarter later, it did. Oil round-tripped from its April peak near $115 back to roughly $70, a ceasefire took hold, and stocks didn’t just steady themselves. They ripped. The S&P 500 gained 15%, its best quarter since the pandemic-recovery snapback in 2020, and finished near record highs.

What we didn’t fully anticipate was how the recovery would arrive. This wasn’t the same market that fell in Q1 simply rebounding. Enthusiasm for artificial intelligence came roaring back, semiconductors had their strongest quarter in almost 30 years, and, in the part that matters most for portfolios, the breadth of the market expanded (i.e. gains spread out to more stocks). Small caps, mid caps, and international stocks all outpaced the S&P 500 on the year.

See more: Markets: What to Watch Midway Through 2026

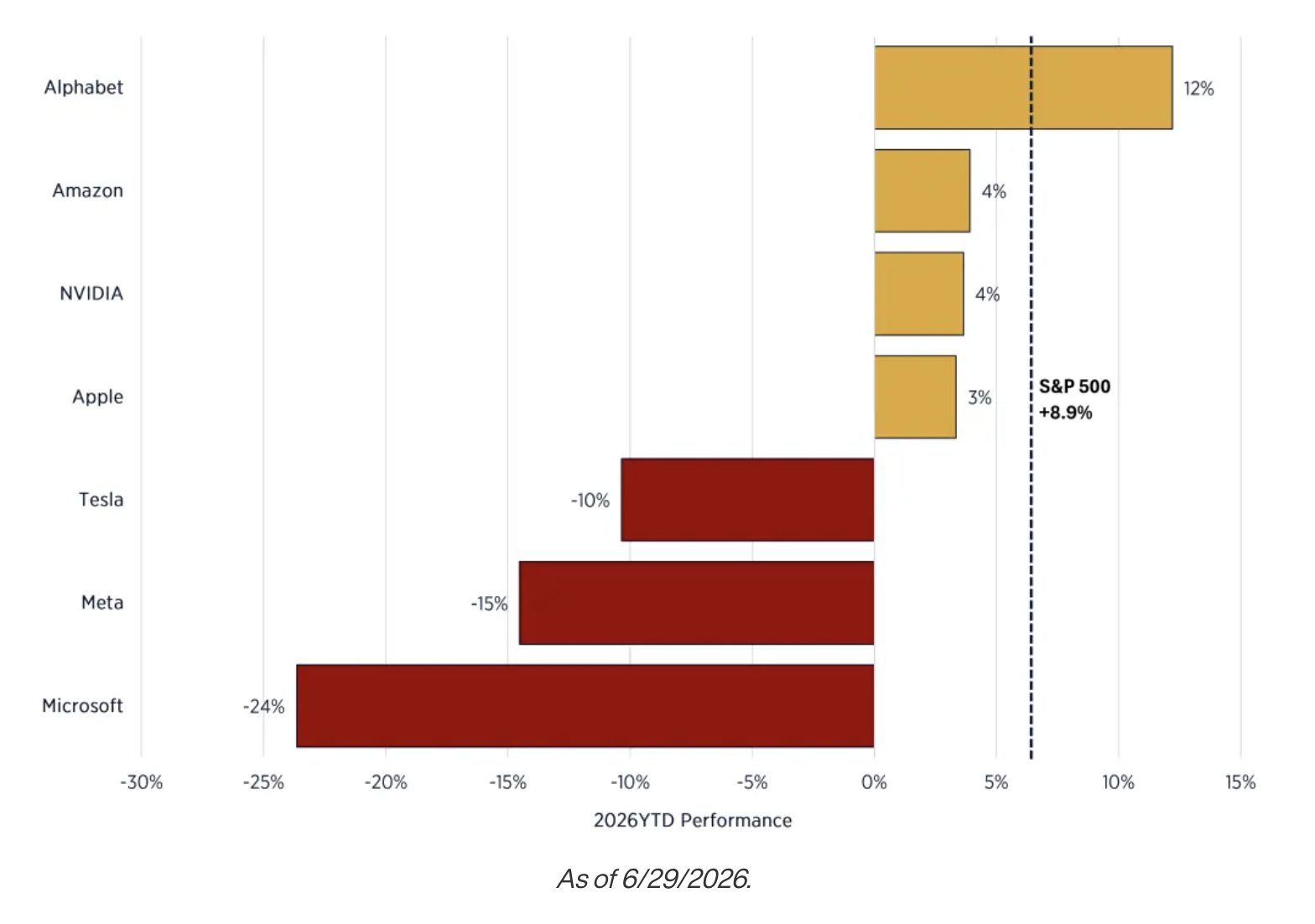

The twist is that even the AI trade broadened. For three years, “the AI trade” and “the Mag 7” were treated as one and the same. In Q2 they came apart. As we detailed in our recent note on the memory rotation, the quarter’s biggest AI winners weren’t the mega-caps at all (that group was roughly flat on the year) but the companies actually supplying the buildout. Leadership rotated, quietly, and most portfolios anchored to the same seven names felt it (See: Mag 7, Memory and Semiconductors: The Quiet Market Rotation).

Looking ahead, we remain constructive. The key macro driver we’ve watched all year, oil into inflation into Fed policy, is starting to ease as energy prices normalize, and earnings estimates are still rising underneath it all. But a quarter this strong also prices in a lot of good news. Given the rotation we’ve seen this quarter we’d rather own that optimism through a diversified portfolio than through the handful of names carrying the highest expectations.

The Economy and Markets: S&P 500, Inflation, and the Fed in Q2 2026

-

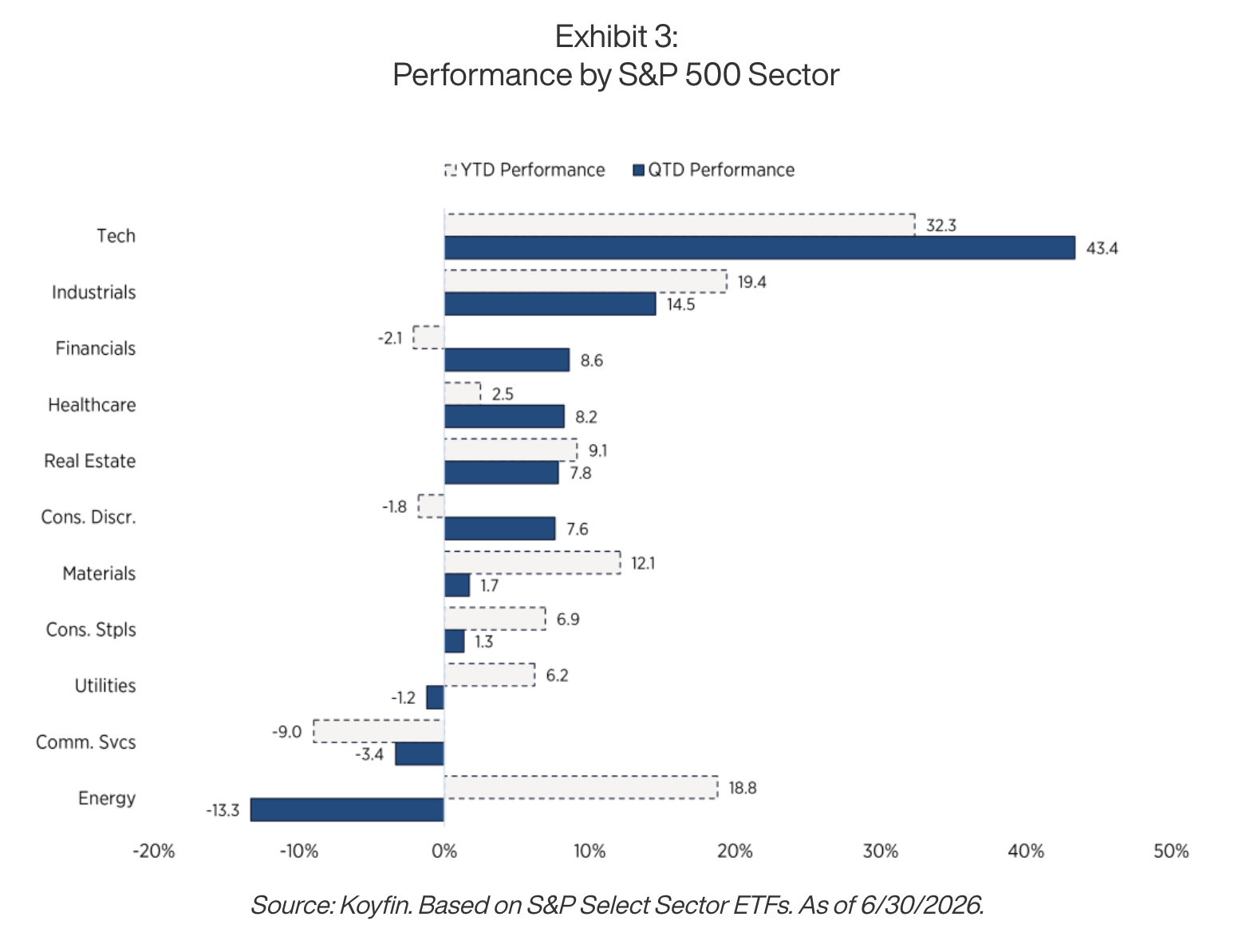

Equities rebounded hard and broadly. The S&P 500 gained 15%, its strongest quarter since Q2 2020, with the Nasdaq up over 21% (the Nasdaq 100 was up nearly 28%) and the Dow up over 13%. Nine of eleven sectors finished higher. Technology led at an over 43% gain, and was the only sector to beat the index, while Energy fell 13% as oil unwound, the lone sector in the red.

-

Oil round-tripped, and inflation followed it up before it could follow it down. Crude peaked near $115 in April as the conflict disrupted supply through the Strait of Hormuz, then fell back to roughly $70 by quarter-end on the ceasefire. That spring spike still pushed May consumer prices up 4.2% year-over-year, a three-year high, with more than half of the monthly increase tied to energy. Strip energy out and the underlying rate was +2.9%, a sign the jump was an oil story, not a broad one.

-

The Fed leaned the other way. Coming into the year, markets expected two or three rate cuts. By the end of Q2 they were pricing a possible hike this fall. The Federal Reserve held steady at both meetings but signaled its next move could be up rather than down. Because the May inflation reading captured oil near its peak, and oil has since normalized, we expect the inflation pressure that drove the Fed’s shift to fade in the months ahead.

TIMELY TOPICS

The Rotation Beneath the Rally

The headline out of Q2 was a monster tech quarter. Semiconductors returned +88%, their best three months in nearly 30 years, rivaled only by the late-1990s internet boom.

But the more important story for portfolios wasn’t the size of the tech move. It was how much of the market participated. The S&P 500 has gained over 10% this year, yet strip out the technology sector and that number falls to just 5%. Meanwhile the parts of the market that were supposed to be “also-rans” put up double-digit returns: mid caps and international stocks each returned roughly +17%, and small caps gained +22%.

Several fundamentals explain why the rest of the market finally kept pace. Smaller companies carry more floating-rate debt, so the Fed’s earlier rate cuts flowed straight to their bottom line as interest savings. They’re also more tied to the domestic economy, which has stayed resilient. Today’s economy is far less energy-dependent than the 1970s, so this year’s oil shock did far less damage than past crises. And after years of trailing, smaller and international companies simply looked cheaper, and their improving earnings made that gap harder to ignore. This looks less like a temporary rotation and more like a structural rebalancing of leadership.

The same broadening showed up inside the AI trade itself, which is the part we’d flag for clients. As we covered in our recent piece on the semiconductor and memory rotation, the quarter’s biggest AI winners weren’t the Magnificent Seven (that basket was essentially flat on the year) but the “picks-and-shovels” suppliers underneath the buildout. Memory chipmakers led the way as AI demand created a genuine supply shortage, sending prices sharply higher and the memory complex up triple digits. Even within the Mag 7, the dispersion was striking: a couple of names posted double-digit gains while others fell double digits on worries that their capital spending isn’t converting to revenue fast enough. In other words, the market started paying for demonstrated AI payoff rather than projected payoff.

The takeaway isn’t to chase memory stocks after a 100%-plus run, since those cycles turn hard when new supply eventually arrives, and chasing a trade that’s already tripled is its own kind of mistake. The point is that leadership rotates without announcing itself, and a portfolio built to lean toward genuine strength across company sizes, styles, and geographies doesn’t have to guess which name leads next. For two years diversification felt like a drag.

This year it’s been the point, and that’s exactly why we build portfolios the way we do.

Second-Half 2026 Investment Outlook: What to Watch

The single thread that tied the first half of the year together, oil into inflation into Fed policy, carries into Q3. In our view, with crude back near where it started, the main driver of higher inflation has already begun to fade. The question is whether the cooling shows up in the next couple of inflation reports. If it does, it takes real pressure off the Federal Reserve. If it doesn’t, the Fed’s cautious posture, and a possible hike, is likely to persist. The next few prints will go a long way toward answering what the Fed does next.

The second thread is the durability of the AI buildout. The spending behind it is enormous. Five of the largest tech companies are projected to invest roughly $724 billion this year and nearly $900 billion next year, up from about $416 billion in 2025. Increasingly, that spending is funded by issuing new debt and equity, which means it eventually has to convert into real profits to justify the scale. The late-June pullback in technology was a useful reminder of how quickly prices can swing when expectations are this high.

And the last is whether the market’s broadening holds or leadership narrows back to a handful of names. As of this writing, participation is wide and the backdrop is healthier than the narrow, top-heavy markets of the past few years, but broadenings have narrowed before, and this one is worth watching.

Near-term, we’ll be watching earnings. The companies leading the buildout are posting record results and growing backlogs, and estimates across the broader market are still rising. Looking back at the first half of the year markets have absorbed: a war, an energy shock, inflation at a three-year high, and a Fed leaning toward a hike. Through it all the market continued to make new highs, and companies continued to generate growing earnings. We can’t know exactly how the open questions resolve, but a diversified portfolio and a long-term perspective remain the most reliable way through them. We remain constructive heading into the back half of the year.

Please read important Defiant Capital Group disclosures here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group