The Federal Open Market Committee (FOMC) meets this week in what will be Kevin Warsh’s first meeting as Chair of the Federal Reserve. President Trump has been vocal about wanting to see lower yields and general consensus is that Warsh was his pick due to Warsh’s general lean towards lower rates. The economy that Chair Warsh inherits makes the path to lower rates much more difficult than it might have been at the time that he was nominated by President Trump (January 30th). Over the past few months, inflation has pushed steadily higher while the labor market has remained strong. With the Fed’s objectives of maintaining a strong labor market while aiming for 2% inflation, the playbook based on the recent trends in economic data point more towards higher rates rather than lower rates.

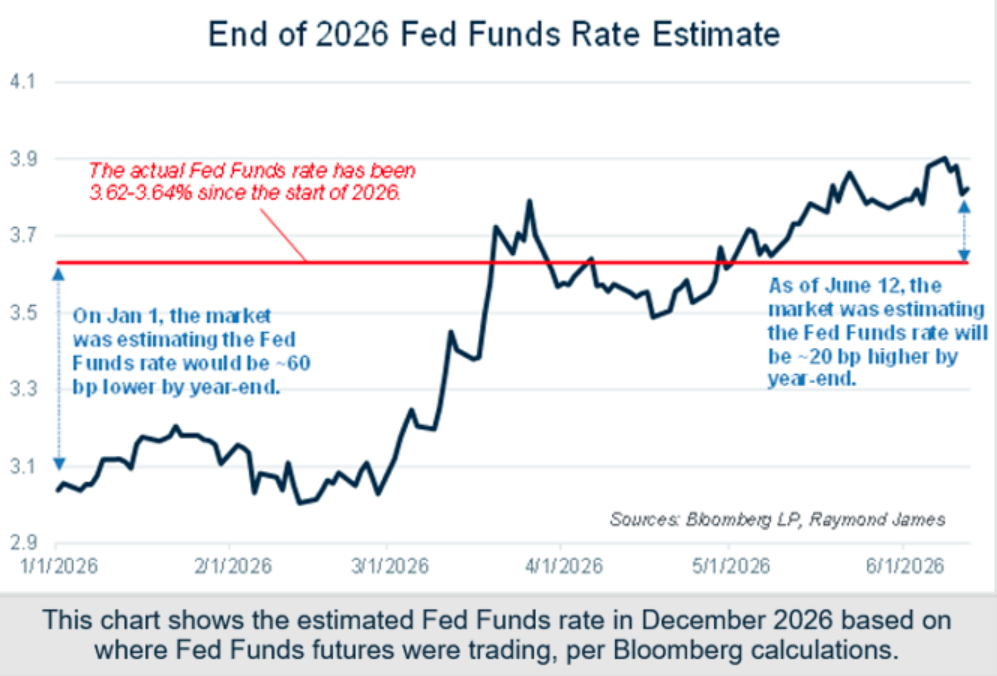

The chart above provides a summary of both the inflation picture and the labor market picture and how things have changed so far in 2026. Headline CPI has risen from 2.4% to 4.2% while Core CPI, which excludes food and energy prices, has risen from 2.5% to 2.9%. Inflation started the year already above the Fed’s 2% goal and has moved steadily away from their target since then. At the same time, the Change in Nonfarm Payrolls (using the 3-month average to smooth out the month-to-month volatility) has improved by a considerable margin. As the chart below highlights, the market has reacted to the data as expected.

At the start of the year, the market was pricing in two 25-basis point cuts to the Fed Funds rate by the end of the year as the year-end estimate for the Fed Funds rate was in the low 3% range for the first few months of the year when the actual rate was 3.64%. Since early March, the estimated year-end rate has moved higher and currently sits at 3.82%, which implies a rate hike by year-end. The FOMC member narrative shift is a consequence of persistent inflationary trends and calming labor market data.

If Kevin Warsh was hoping to take his seat as leader of the Fed and immediately start cutting rates, his hopes have likely been dashed. A more likely outcome is that we will see no changes to the Fed Funds rate in the near-term as Warsh settles into his new role and the FOMC waits for the global macroeconomic picture to hopefully calm down and provide a clearer picture of the direction moving forward. Chair Warsh’s first meeting might still provide some insight into potential changes at the Fed. He has stated his preference for less forward-guidance, fewer forecasts, and less communication from the Fed, as well a desire to scale back the balance sheet. Warsh is scheduled to hold a press conference following the FOMC meeting on Wednesday, which is the first opportunity the market will have to start gaining insights into any changes that might be coming down the road. Keeping in mind that FOMC policy is determined by a committee vote, Warsh will likely spend his initial months as leader of the Fed trying to convince his fellow board members to come around to his views rather than coming out and starkly contrasting consensus opinions on day one. For fixed income investors, Wednesday will hopefully provide valuable insight into what a Warsh-led Fed is going to look like.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® and power of personal® are registered trademarks of Raymond James Financial, Inc.