On June 12, SpaceX went public with a US$2 trillion valuation—the largest initial public offering (IPO) ever, by far. It has been the most anticipated IPO in more than two decades and likely ushers in a series of high-profile IPOs in the coming months, including for OpenAI and Anthropic. The SpaceX IPO shifts the way that we think about public and private equity.

Elon Musk founded SpaceX in 2002, before Tesla, and has intentionally kept the company private as he’s built the firm and its vertical businesses—Starlink and XAI. Musk recognized that SpaceX couldn’t survive as a public company during the development phase, and since he was able to raise capital, he chose a path different from most young startups during the dot-com era.

The changing dynamics of private equity

While SpaceX is an extreme example, given its size and tenure as a going concern (24 years), it illustrates the shifting dynamics between public and private companies. Over the last two decades, the number of companies in the US publicly traded market has been roughly half its size during previous decades, declining from about 8,000 companies in 1996 to about 4,000 companies in 2025.1 Meanwhile, the number of US private companies has been rising. Today, 87% of all US companies with at least US$100 million in revenue are private.2 This represents approximately 20,000 companies, and globally, there are approximately 100,000 private companies.

Read more: Buyable Pullbacks. Be Prepared.

A second dynamic is that companies are staying private longer. During the dot-com era, the only paths for young companies was to bring their company public via an IPO or be acquired by a larger firm. This allowed founders and senior executives to reap the benefits of building their enterprise and monetizing the opportunity. Today, with the abundance of capital available, companies can choose to remain private longer, and some will never go public.

Staying private allows these young companies to execute their long-term plan, rather than meeting the quarterly demands of shareholders. In the SpaceX example, staying private insulated Musk from public scrutiny when the first three rockets blew up. It also allowed him to build vertical businesses like Starlink and XAI. Building these businesses in the public domain would have been very challenging, if not impossible.

What does this mean for private equity going forward?

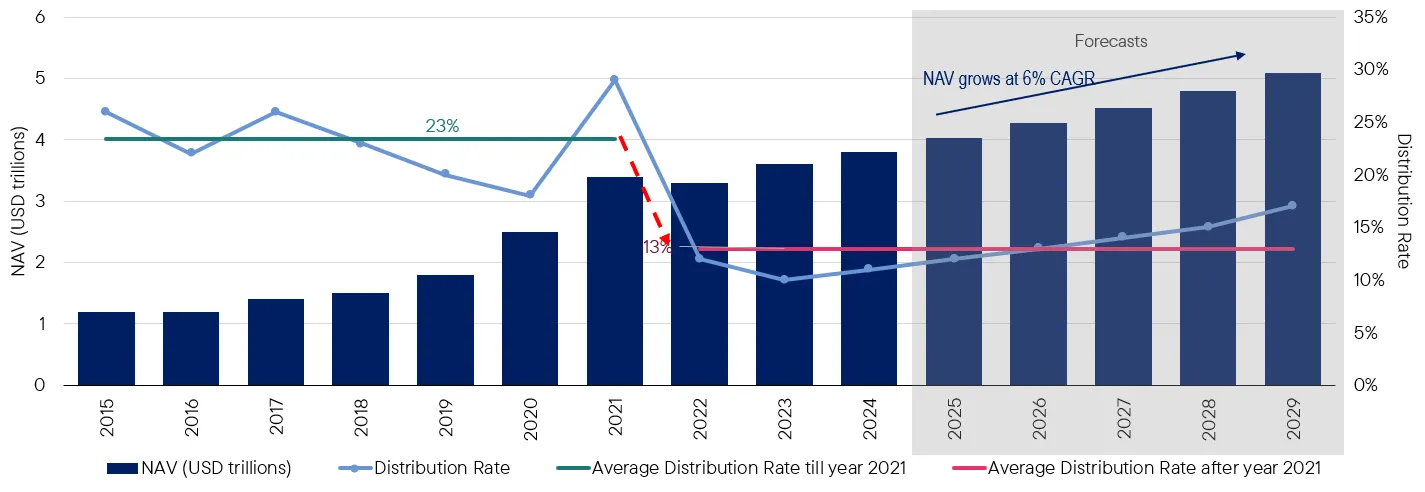

Coming into 2026, we had anticipated a pickup in exits (IPOs and merger and acquisition [M&A] activity). This was delayed due to the Middle Eastern conflict—but there appears to be a robust pipeline of companies going public in the next year or so. More exits mean that more capital is returned to investors in the form of distributions. Since 2021, distributions have been anemic, leading institutions to seek liquidity in the secondaries market.

Exhibit 1: Distributions Have Declined

Distribution Rate and NAV in Global Private Equity

It is important to note that we do not believe secondaries lose their appeal as distributions improve. We continue to believe that institutions will utilize the secondary market to meet their liquidity needs, and we think secondaries represent a core private equity allocation in the wealth channel, due to its structural advantages (it can help shorten the J-curve and time to distribution), and built-in diversification (GP, vintage, geography and stage).

SpaceX and these other high-profile IPOs remind investors about the opportunities in private equity. Much like Google, Apple, Microsoft, and Tesla before them, SpaceX, OpenAI and Anthropic each began with an idea. These ideas were nurtured and refined as private companies. As their businesses grew, and they scaled their operating models, they each chose to take their companies public via an IPO.

The SpaceX IPO serves as a reminder of the convergence of public and private capital. Private companies now have alternatives to an IPO and can often choose the best path for each enterprise. SpaceX will become one of the largest publicly traded companies after its IPO. This was a 24-year journey.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Endnotes

1Sources: US Census Bureau, World Bank, Macrobond. As of December 31, 2025.

1Sources: “Private Market Investing: Staying Private Longer Leads to Opportunity.” Hamilton Lane. April 14, 2022. “The Truth Revealed: The private markets universe is less concentrated and larger today than any other time in history.” Hamilton Lane. March 8, 2023.

Glossary of terms

J-curve: A description of the typical distribution pattern of private equity funds, which often includes negative net returns in the initial years followed by rising positive returns in later years.

GP: General Partner, the individual or entity that manages a private equity or venture capital fund, and is responsible for operations and investment decisions.

Vintage: In private equity, the vintage refers to the year when a fund begins making investments.

Stage: A point in the development and growth of private equity companies, such as early-stage ventures, growth stage, and mature stage.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Investments in alternative strategies may be exposed to potentially significant fluctuations in value.

Diversification does not guarantee a profit or protect against a loss.

Equity securities are subject to price fluctuation and possible loss of principal.

The investment style may become out of favor, which may have a negative impact on performance.

Investments in privately held companies present certain challenges and involve incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity.

Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

The portfolio’s investment strategies incorporate the identification of thematic investment opportunities, and its performance may be negatively impacted if the investment manager does not correctly identify such opportunities or if the theme develops in an unexpected manner. By focusing its investments in information technology-related industries, the portfolio carries much greater risks of adverse developments and price movements in such industries than a portfolio that invests in a wider variety of industries.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

© Franklin Templeton

Read more commentaries by Franklin Templeton