An increasing number of our neighbors are now retired. As they have made that transition, their sensitivity to the costs of living has increased, as has their skepticism over the way that inflation is measured. A common refrain: “I don’t care what the numbers say…things are REALLY expensive these days!”

Our perception of inflation is a personal one, depending on where we are in life and what we are buying. At the macro level, there is a range of perceptions among economists on the correct rate of inflation. The debate over which to focus on may be renewed as Kevin Warsh assumes leadership at the Federal Reserve.

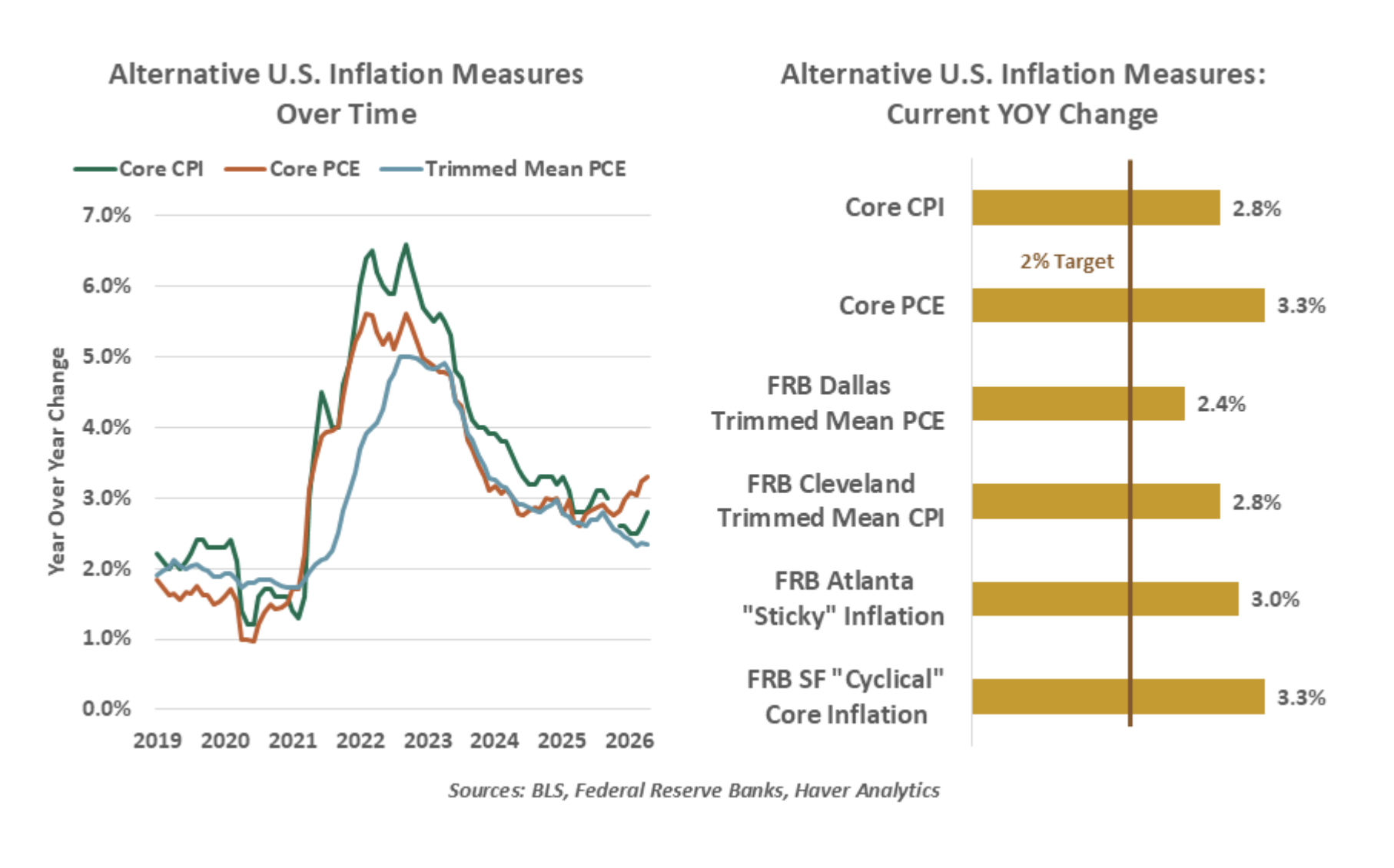

The consumer price index (CPI) and the deflator on personal consumption expenditures (PCE) are the two leading inflation indicators. A comparison of the two can be found here. Policymakers often focus on core measures, which remove food and energy prices, as these components can be volatile and are less sensitive to monetary policy.

Incoming Fed Chair Kevin Warsh, however, has touted “trimmed-mean” inflation measures, which eliminate categories showing the most extreme monthly movements in each direction. The Federal Reserve Bank of Dallas’ trimmed mean index excludes items that show the lowest 25% and the top 30% of price changes.

Since 2019, trimmed mean measures have typically been lower than core rates of change in the CPI and in the PCE deflator. In the most recent readings, the core PCE had increased 3.3% over the past 12 months, while the FRB Dallas trimmed-mean measure was up only 2.4%.

Read more: Trying Tango

Proponents of trimmed-mean measures note that food and energy aren’t the only volatile categories of consumer prices; each month, extremes can be seen in a range of other categories. One-time increases in the price level, such as those resulting from supply shocks, are given less weight. Revisions to trimmed-mean gauges are typically smaller.

Skeptics of the trimmed-mean approach note that it excludes a large fraction of consumer prices, and point to their lagging behavior during the post-pandemic period. Some have expressed concern that Warsh may be “cherry-picking” the metric showing the lowest inflation rate to make a case for easing monetary policy.

My neighbors insist that the inflation rate is at least 5%. No documentation is offered, but no amount of data will dissuade them. My strategy is to avoid the subject…at all costs.

Carl Tannenbaum is the Chief Economist for Northern Trust.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Northern Trust

More Cryptocurrencies Topics >