Key points:

- Before the decline over the past week, underneath the surface of markets, data showed record levels of speculation and stretched valuations that possibly contributed to the recent pullback.

- Investor enthusiasm and abundant liquidity have fueled rallies in unprofitable, highly levered stocks, while volatility in October rose alongside equity prices—an inversion of typical market dynamics.

- As markets grow increasingly concentrated in a handful of mega-cap names, liquid alternatives offer investors a way to reduce concentration risk and uncover differentiated sources of return.

Like ducks on a pond, markets often appear calm on the surface while churning furiously underneath. For financial markets, above the surface, attention has focused on equity market valuations and record-tight levels of credit spreads, but a deeper look reveals even more extreme dynamics below. Beneath the smooth surface, data shows that markets had rarely been this stretched, a factor potentially contributing to the past week’s pullback.

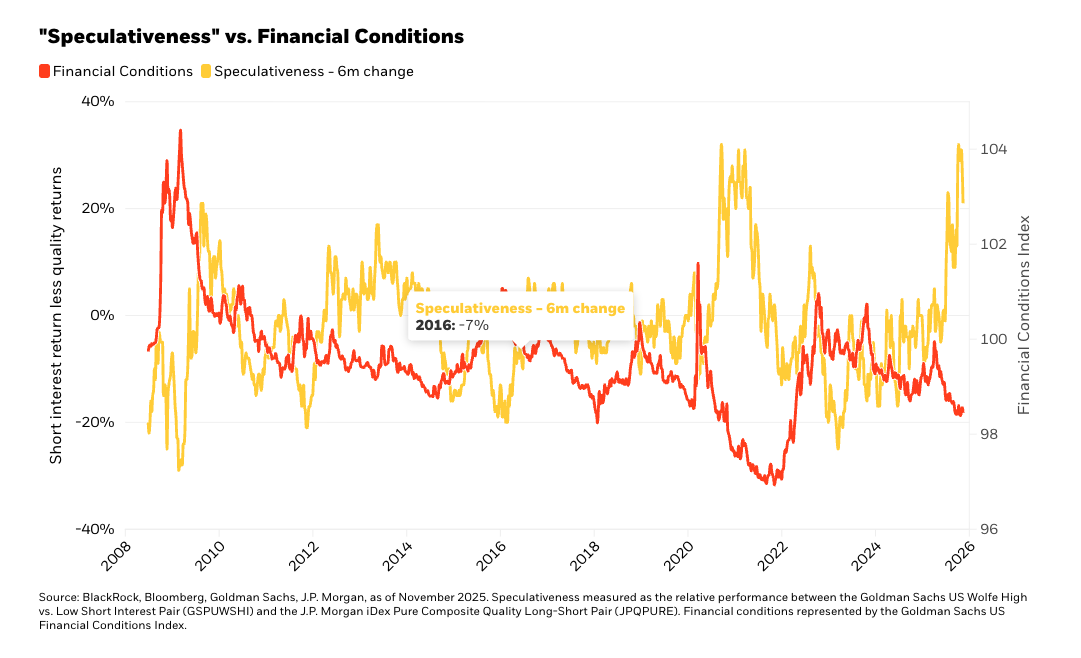

The story of this year’s rally is a familiar one: fear gave way to greed. After markets recovered from “liberation-day” tariff-induced recession worries in June, equities surged as investors piled back into risk. Defensive stocks lagged, high-volatility names soared, and short-sellers scrambled to cover positions. We capture the “speculativeness” of this behavior through the return gap between heavily shorted stocks and high-quality stocks. By mid-July, that return gap had ballooned to an extraordinary 23% over six months—one of the widest stretches in recent memory.

On the macro side, July’s payroll revisions validated the doves’ argument that earlier job gains had been overstated. Fed Chair Powell abruptly shifted focus, signaling a preference for sustaining growth over tamping down inflation concerns. Markets seized on the cue. Expectations for lower rates climbed, financial conditions loosened, and liquidity flooded back into risk assets. The result was a second surge in market speculativeness, pushing our six-month measure to a 32% return gap in early October. This renewed exuberance coincided with the easiest levels of financial conditions seen outside of the COVID response, and before that, not since the run-up to the GFC.

Volatility Turns Upside Down

Investor enthusiasm didn’t just lift prices; it flipped one of market behavior’s oldest relationships on its head. Normally, volatility rises when stocks fall, reflecting hedging demand. But in late September, volatility increased alongside higher equity prices. During the week ending October 3, implied volatility climbed even as indexes pushed higher, a telltale signature of call-option buying and speculative leverage. The week closed with five consecutive days of this inverted pattern, the longest such streak in the history of the VIX index.

When Quality Falls Out of Fashion

The speculative fever extended well beyond volatility and short covering. Market leadership shifted decisively toward unprofitable and highly levered companies. Investors rewarded balance sheet fragility while selling steady, cash-generating firms. For systematic strategies grounded in quality, stability, and downside protection, this environment proved uniquely challenging. The market’s reward system temporarily inverted—penalizing prudence while celebrating risk.

Credit Markets Reflect a Two-Speed Economy

Credit markets echoed this divide. Pricing now reflects a two-speed economy, often described as “K-shaped,” where high-income consumers’ wealth gains power overall consumption even as lower-income consumers struggle with rising delinquencies, defaults, and auto repossessions.

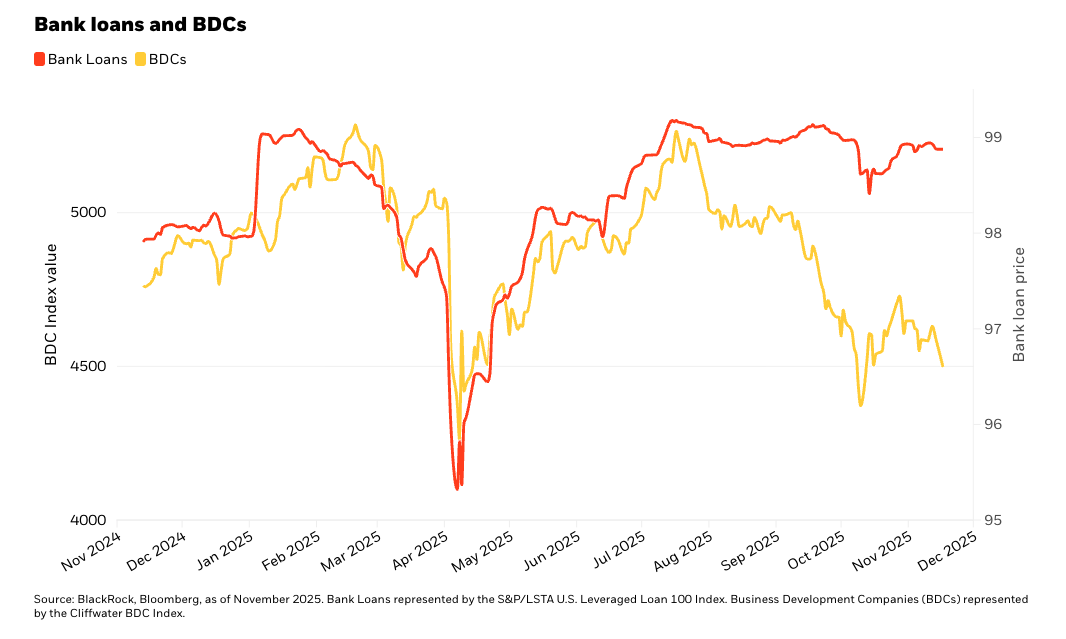

Corporate balance sheets tell a similar story. The dominant technology giants, flush with cash and supported by fortress-like balance sheets, enjoy record-tight spreads. Meanwhile, weaker firms on the losing end of creative destruction—and some affected by highly publicized weaknesses in underwriting that have led to a recent uptick in defaults—are facing rising defaults and growing investor caution.

By October, syndicated loan prices had slid, and Business Development Companies (BDCs) exposed to those types of loans also suffered. At the same time, the capital demands of the AI infrastructure build-out are drawing even the strongest issuers back to debt markets, threatening to expand corporate bond supply and potentially widen spreads from today’s compressed levels.

Finding diversification in an increasingly concentrated equity market

As we look ahead, investors face a new kind of challenge—not one of volatility or valuation, but of historic concentration risk. The equity market has rarely been so dominated by a handful of mega-cap names, leaving portfolios more exposed to idiosyncratic risks than at any point in recent memory. At the same time uncertainty surrounds the Fed’s ability to respond aggressively to future shocks.

In this environment, diversification through alpha becomes essential. Our liquid alternatives suite offers investors a way to reduce concentration risk and broaden return sources without making binary calls on the path of AI-driven growth or the direction of interest rates.

Liquid alternatives have never been more relevant as a complement to traditional equity and fixed income exposures, providing balance, adaptability, and differentiated sources of return when markets move as one.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Investing involves risks, including possible loss of principal.

Key risks of BDMIX: The fund is actively managed and its characteristics will vary. Stock values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. The issuers of unsponsored depositary receipts are not obligated to disclose information that is, in the United States, considered material. Investing in long/short strategies presents the opportunity for significant losses, including the loss of your total investment. Such strategies have the potential for heightened volatility and in general, are not suitable for all investors. The fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility. The fund may engage in active and frequent trading, resulting in short-term capital gains or losses that could increase an investors tax liability. Short-selling entails special risks. If the fund makes short sales in securities that increase in value, the fund will lose value. Any loss on short positions may or may not be offset by investing short-sale proceeds in other investments. Investing in small- and mid-cap companies may entail greater risk than large-cap companies, due to shorter operating histories, less seasoned management or lower trading volumes.

Key risks of BIMBX: The fund is actively managed, and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Principal of mortgage-or asset-backed securities normally may be prepaid at any time, reducing the yield and market value of those securities. Obligations of US government agencies are supported by varying degrees of credit but generally are not backed by the full faith and credit of the US government. Non-investment grade debt securities (high yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher rated securities. Investments in emerging markets may be considered speculative and are more likely to experience hyperinflation and currency devaluations, which adversely affect returns. In addition, many emerging securities markets have lower trading volumes and less liquidity. The fund may use derivatives to hedge its investments or to seek enhanced returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility. Effective 1/4/19, the Alternative Capital Strategies fund name was changed to the “Systematic Multi-Strategy Fund”. The Fund’s information prior to September 17, 2018 is the information of a predecessor fund that reorganized into the fund on September 17, 2018. The predecessor fund had the same investment objectives, strategies and policies, portfolio management team and contractual arrangements, including the same contractual fees and expenses, as the fund as of the date of reorganization. As a result of the reorganization, the Fund adopted the performance and financial history of the predecessor fund.

Diversification and asset allocation may or may not protect against market risk or loss of principal.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change. This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. Reliance upon information in this material is at the sole discretion of the viewer.

The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective. The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

Prepared by BlackRock Investments, LLC, member FINRA.

©2025 BlackRock, Inc. or its affiliates. All Rights Reserved. iSHARES and BLACKROCK are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH1125U/S-4994723

© BlackRock

More Specialty Investments Topics >