The cacophony of headlines coming out of Washington D.C. seems only to get louder by the day. Government layoffs, Medicaid cuts, changes to vaccine policies, pressure on universities, and many other issues come to mind. The question for us as investors is what impact the White House’s policies will have on the economy and whether our portfolio is well positioned to navigate these ever-changing waters. In this outlook, we examine three key issues: immigration crackdowns, rising tariffs, and Trump’s attempts to co-opt the Federal Reserve. We conclude that while risks are certainly elevated, particularly in the long term, the economy in the near term continues to be reasonably healthy and should continue chugging along absent black swan events.

Immigration

Visit any social media site or watch any nightly news show, and you are likely to see immigration raids being carried out across the country or hear about cancelled foreign student visas. Countless articles have been written about the impact of the current immigration backlash on our country’s social fabric, an issue we do not want to ignore or minimize.

In terms of the economic impact, the threat is clear: immigrants account for nearly 20% of the U.S. labor force. They not only play a critical role across the economy — from low-wage day laborers essential to many companies and households, to CEOs of the most advanced companies in the country, to doctors serving rural populations. They also drive over 75% of U.S. population growth, a historically important but often overlooked building block to economic growth we have previously written about. We have multiple economic concerns related to the administration’s aggressive anti-immigrant policies:

- The labor force is already very tight, with unemployment at just 4.3%, so shrinking the labor pool for critical jobs that are often extremely hard to fill (construction, electrical work, plumbing, etc.) is potentially detrimental to the economy and could exacerbate labor shortages that drive higher inflation.

- Immigrants represent nearly 20% of economic activity, roughly commensurate with their representation within the labor force. Harming consumer confidence for this group could depress economic activity and purchasing behavior.

- Historically, universities have served as a pipeline to bring highly skilled workers into the U.S. for an education before ascending the private sector ladder. The administration’s attacks on immigrants and higher education have resulted in university enrollment of foreign students declining 19% year-over-year as of August and potentially as much as 40% once the full count is in. This could risk our coveted role as the global destination of choice for the most talented knowledge workers.

- In addition to universities, the H-1B visa program has historically served as a critical pipeline for bringing the most talented foreign workers into the U.S.; in fact, the current CEOs of Alphabet and Microsoft once held H-1B visas. Therefore, we view with grave concern the administration’s recent imposition of a $100,000 fee for all H-1B visa applicants, which anecdotally appears to be a huge deterrent.

While all these risks are real and not to be ignored (particularly in the long term), there is at least one major near-term offset: productivity improvement. The current business cycle since the fourth quarter of 2019 has averaged annual productivity gains of 1.8%, which compares favorably with 1.5% in the prior business cycle.

We believe this significant improvement likely reflects the effect of automation, with AI further enhancing productivity. These trends appear to be contributing to higher labor productivity for a wide range of jobs, including software coding, legal research, logistics, and customer service, just to name a few. In fact, Walmart, the world’s largest private employer, saw its revenue base grow a very healthy 30% in total from FY20 to FY25, yet headcount is actually down over that timeframe. Furthermore, Walmart’s CEO recently said that he intends to continue growing revenue over the next three years while keeping headcount flat due to AI productivity improvements. Accenture, the world’s largest IT consultant, which has long relied on a growing workforce to increase revenue, recently announced the elimination of 11,000 workers, and management intends to lay off more workers as AI productivity enhancements kick in — a stark reversal in hiring patterns for a headcount-dependent business. Many technology companies, including Alphabet, which long prided itself on a growing workforce, are also trimming their headcounts while maintaining breakneck growth and investment.

In short, companies that have historically depended on labor growth to drive revenue and profit growth are increasingly able to leverage a static or even declining workforce to generate growth. This means that slower population growth is much more compatible with a growing economy than was historically the case.

While we do not doubt that immigration raids have dampened spending among many immigrant communities (and many companies have indicated as much), overall spending resilience across the economy has mitigated this negative impact, particularly as stock market gains have led to surging consumer budgets among higher income demographics.

Tariffs and Globalization

While the U.S. has long been an international trading partner to many countries, the modern rise of globalization began around 1970 when U.S.-imposed tariffs began steadily declining. Offshoring kicked into high gear in the mid-1990s with the passage of NAFTA in 1994 and the formation of the World Trade Organization (WTO) in 1995. China’s entry to the WTO in 2001 was another key milestone in globalization, as China rapidly dismantled its tariff regime. All the while, U.S. tariffs continued to recede.

The net effect of this multi-decade globalization was the rise of low-cost manufacturing in countries like China, which enabled significantly lower priced consumer goods to be produced abroad and imported into the U.S. Offsetting the boon of low-priced goods was the hollowing out of the U.S. industrial base and stagnant wage growth. In fact, median real wages from 1979 to 2015 were essentially flat, while the number of manufacturing employees started to plunge in 1979, and has been declining ever since.

Trump’s tariff policies evidently aim to reverse these trends, but we have our doubts for several reasons. First, despite Trump’s rhetoric, tariffs are paid entirely by U.S. companies that import products into the U.S. These costs are often passed onto consumers in the form of price increases, creating the risk of an inflationary cycle.

Second, re-imposing tariffs will not magically bring manufacturing and heavy industry back to the U.S. Consider that China accounts for roughly 35% of global manufacturing output, more than the U.S., Japan, Germany, India, South Korea, Italy, France, and Taiwan combined. This rise in manufacturing dominance has led China and its companies to build a massive regional and global infrastructure and supply chain to support this manufacturing base. Imposing tariffs will not dismantle this infrastructure, and China is unlikely to relinquish its position as the sole “manufacturing superpower” in the world. In fact, a World Economic Forum study recently pointed out that China has begun to “focus on advanced technology and manufacturing, aiming to enhance the quality and sustainability of economic development.”

Lastly, simply look at the U.S. manufacturing PMI — a gauge of manufacturing activity — which has been in contraction for seven straight months with no evident benefit from tariffs.

Despite our reservations about tariffs, we believe there are two key mitigating factors. First, while Trump initially threatened preposterously high tariffs on China in particular and broadly across the globe, he quickly retreated. JP Morgan estimates that the initial framework laid out in April 2025 would have resulted in an average tariff rate of nearly 25% (above even Great Depression highs). This stood in contrast to an average tariff rate of less than 3% when Trump entered office in January 2025. Since then, Trump’s tariff retreat has led to an average effective tariff rate of about 12% and potentially as low as 4% according to one study — still elevated but well below the initial threat.

Second, the AI boom is leading to massive infrastructure and semiconductor investment in the U.S. In many ways this is helping achieve the administration’s desired outcome of re-industrialization, in spite of and not because of tariffs. Some estimate that AI spend has accounted for one-third of GDP growth in recent quarters. Reuters reports that “construction spending on U.S. data centers reached an all-time high of $40 billion at a seasonally adjusted annual rate in June [2025] … a 30% increase from the previous year, following a 50% surge in 2024.” This spend is underpinned by hyperscaler CapEx, which is on track to exceed $300 billion in 2025 and will likely continue to grow well beyond this year. As Bloomberg recently reported, a one gigawatt data center costs about $50 billion to build, with $15 billion in the form of land, construction, and energy and the other $35 billion spent on AI chips. In other words, while the current construction boom is meaningful to those involved in construction and the supply of products into the construction trade, the production and sale of semiconductor chips that go into these data centers creates even more demand for advanced manufacturing in the U.S. A good example is TSMC’s manufacturing plant in Phoenix that began producing NVIDIA’s advanced Blackwell chips this year. Two other new facilities are expected to open in Houston and Dallas, where partner manufacturers will produce other advanced chips for NVIDIA.

Taken together, we think the tariff retreat and the AI construction and production boom could materially blunt the impact of tariffs. And despite his retreats, Trump’s tariff threats may induce some companies to bring production into the U.S. to avoid being targeted. This dynamic should continue resulting in near-shoring of supply chains to countries like Mexico and Canada, now the two largest trading partners to the U.S., and increased domestic construction related to AI megaprojects.

Federal Reserve Independence

We are strong believers in Fed independence. Setting interest rates is a critical role for any well-functioning economy, and we think doing so should be separated from political considerations. Fed independence is thus critical to the functioning of the U.S. economy in our view. As a result, we have been alarmed to see Trump’s persistent attempts to meddle in Fed affairs in hopes of lowering interest rates. In July Trump threatened to fire Fed Chair Jerome Powell, an unprecedented move. He has since appointed Stephen Miran — a sitting member of the executive branch — as a Fed governor, another unprecedented move. And he continues to try to fire Lisa Cook, a Biden-appointed Fed governor.

While we firmly stand against these moves, there are several offsetting factors that dampen the threat to Fed independence. First, Chair Jerome Powell has so far been extremely firm in ignoring the president and recently “pushed back hard against claims the central bank allows politics to drive decisions.” We take comfort in Chair Powell’s resolve in the face of significant pressure.

Second, the Supreme Court continues to get in the way of Trump’s attempts to fire individual Fed Governors. In fact, on October 1st, the Supreme Court issued an order protecting Fed Governor Lisa Cook and allowing her to maintain her role at the Fed while the administration litigates against her. Similar to Chair Powell, Governor Cook has resisted and insists on having her case heard.

Third, and maybe most importantly, the Fed Board of Governors consists of seven appointees, each with 14-year terms. Thus, changing one or two governors is unlikely to result in a compliant and servile Fed. Rather, Trump would have to stack the Fed with his own appointees, which would be highly challenging given that apart from Stephen Miran (whose term is actually the first to expire, in January 2026), no Fed governor’s term expires before 2028 at the earliest. Therefore, we believe the institution’s structure protects it from meddling in all but the most extraordinary circumstances.

Secular Trends Shaping Our Portfolio

In our view, the most effective way to navigate through the current political environment is to focus on high quality companies that are experiencing secular growth. We believe AI efficiency and near-shoring/deglobalization are both secular trends with years of future runway, and many of the companies in our portfolios should benefit from these trends. Below are several areas in which we have invested and how they fit into this framework:

- AI beneficiaries

- Hyperscalers that provide cloud computing

- Semiconductor companies involved in advanced semiconductor design and production

- Software providers implementing AI

- Distributors into the data center construction market

- Near-shoring/deglobalization beneficiaries

- Rail operators

- Infill industrial real estate owners

- Industrial gas companies

Conclusion

We are undoubtedly in uncharted waters from a political standpoint and worry about the long-term implications of many of Trump’s policies. But near- and medium-term we believe there are significant offsets that are enabling relatively smooth sailing for consumers and businesses in the aggregate. Echoing this view, key macroeconomic indicators reflect a more sanguine picture: U.S. real GDP grew at a 3.8% annualized pace in the second quarter, unemployment — while creeping higher and a measure we watch closely — remains low at 4.3%, headline inflation is manageable at 2.9%, and real wages continue to grow at 0.7%. Importantly, corporate profits marched higher, with third quarter growth at 8% year-over-year and analysts projecting 11% earnings growth over the next twelve months. The recent interest rate cut could further boost sentiment and support demand across the economy.

Regardless of the environment, we continue to apply our quality growth framework to managing portfolios, as we believe owning high quality businesses that can grow in most environments and that are well run should result in attractive returns over time, particularly when purchased at discounted valuations.

As always, we thank you for your continued confidence in our management.

John Osterweis, Founder, Chairman & Co-Chief Investment Officer – Core Equity

Gregory Hermanski, Co-Chief Investment Officer – Core Equity

Nael Fakhry, Co-Chief Investment Officer – Core Equity

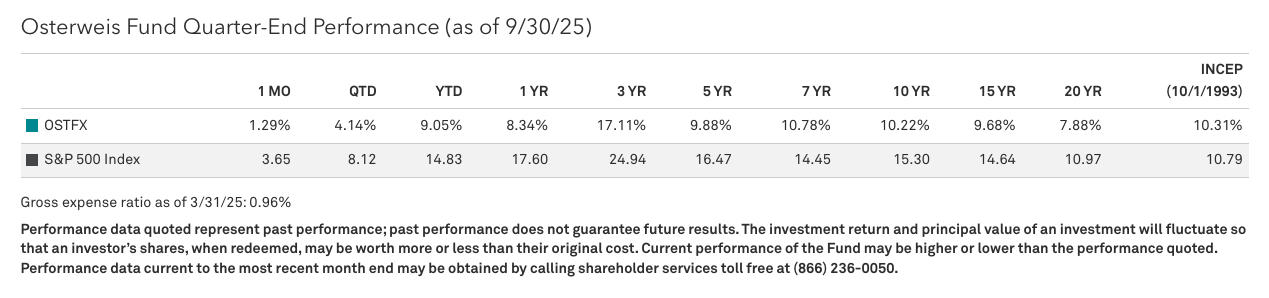

Rates of return for periods greater than one year are annualized.

Where applicable, charts illustrating the performance of a hypothetical $10,000 investment made at a Fund’s inception assume the reinvestment of dividends and capital gains, but do not reflect the effect of any applicable sales charge or redemption fees. Such charts do not imply any future performance. During the period noted, fee waivers or expense reimbursements were in effect for the Osterweis Fund.

The S&P 500 Index is widely regarded as the standard for measuring large cap U.S. stock market performance. The index does not incur expenses, is not available for investment, and includes the reinvestment of dividends.

References to specific companies, market sectors, or investment themes herein do not constitute recommendations to buy or sell any particular securities.

There can be no assurance that any specific security, strategy, or product referenced directly or indirectly in this commentary will be profitable in the future or suitable for your financial circumstances. Due to various factors, including changes to market conditions and/or applicable laws, this content may no longer reflect our current advice or opinion. You should not assume any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from Osterweis Capital Management.

Complete holdings of all Osterweis mutual funds (“Funds”) are generally available ten business days following quarter end. Holdings and sector allocations may change at any time due to ongoing portfolio management. Fund holdings as of the most recent quarter end are available here: Osterweis Fund

As of 9/30/25 the Osterweis Fund did not hold positions in Walmart, Accenture, or TSMC.

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges, and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com/statpro. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Mutual fund investing involves risk. Principal loss is possible.

The Osterweis Fund may invest in medium and smaller sized companies, which involve additional risks such as limited liquidity and greater volatility. The Fund may invest in foreign and emerging market securities, which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks may increase for emerging markets. The Fund may invest in Master Limited Partnerships, which involve risk related to energy prices, demand and changes in tax code. The Fund may invest in debt securities that are un-rated or rated below investment grade. Lower-rated securities may present an increased possibility of default, price volatility or illiquidity compared to higher-rated securities. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities.

Investment and insurance products are not FDIC or any other government agency insured, are not bank guaranteed, and may lose value.

Coupon is the interest rate paid by a bond. The coupon is typically paid semiannually.

A yield curve is a graph that plots bond yields vs. maturities, at a set point in time, assuming the bonds have equal credit quality. In the U.S., the yield curve generally refers to that of Treasuries.

Yield is the income return on an investment, such as the interest or dividends received from holding a particular security.

Gross Domestic Product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period.

Capital expenditures (CapEx) are funds used by a company to acquire, upgrade, and maintain physical assets such as property, plants, buildings, technology, or equipment.

Maturity is the date on which the life of a transaction or financial instrument ends, after which it must either be renewed, or it will cease to exist.

Investment grade bonds are those with high and medium credit quality as determined by ratings agencies.

Purchasing Managers Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

No part of this article may be reproduced in any form, or referred to in any other publication, without the express written permission of Osterweis Capital Management.

This commentary contains the current opinions of the authors as of the date above, which are subject to change at any time, are not guaranteed, and should not be considered investment advice. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy, or investment product. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC. [OCMI-820246-2025-10-14]

A message from Advisor Perspectives and VettaFi: Gain exposure to the evolving digital asset landscape. Learn about CoinShares ETFs.

© Osterweis Capital Management

Read more commentaries by Osterweis Capital Management