Key Takeaways

- Russ argues that a 2-4% strategic allocation to gold is still warranted and notes that historically, gold tends to outperform stocks when volatility rises - which often occurs in the fall.

- While volatility is currently trading at its lowest level since February, upping one’s exposure to gold in the short-term can provide both insurance and lock in potential gains as we head into the latter half of the year.

After a difficult start, stocks are back to their winning ways. The S&P 500 continues to advance and is now up a respectable 10% year-to-date. While alternative strategies worked in the first quarter, since May investors have done best rotating back into U.S. equities. While I still believe stocks will end the year higher, we are entering a time of year when volatility tends to rise. Given this short-term dynamic, I would advocate adding a bit more gold to portfolios.

I last spoke about gold in May. At the time, I was less focused on gold’s short-term value as a hedge, which is mixed, and more motivated by gold’s role as a long-term store-of-value against runaway deficits and legitimate questions about the dollar. Both factors still argue for a strategic allocation, which I’d define as around 2-4%. That said, in the short-term there may be an argument for taking the allocation towards the upper end of the range. If volatility rises, as it typically does in the fall, gold tends to post strong relative performance versus stocks.

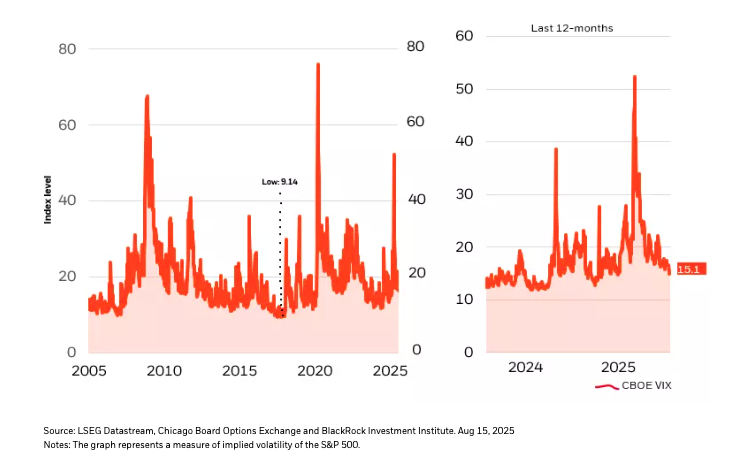

Calmer Waters

Consistent with a year of rapidly changing themes, equity market volatility, as measured by the VIX Index, has traded in a particularly wide range. March witnessed a violent spike, taking volatility to multi-year highs, only for the surge to reverse at a record pace. Recently, volatility has collapsed, with the VIX Index trading below 15, the lowest level since February (see Chart 1).

Chart 1

The key point in the relationship between gold, stocks and volatility: Even a modest uptick in equity market volatility can favor gold. Looking back at the past fifteen years, there has been a very consistent relationship between how gold performs relative to stocks and weekly or monthly changes in implied volatility.

Take the most recent period, in which gold has lagged as volatility fell. The reverse holds true as well. Based on weekly data from Bloomberg, in weeks when the VIX rises, gold outperforms the S&P 500 by an average of roughly 1%. The greater the spike in volatility, the greater the outperformance. A 20% spike in volatility has historically been associated with an average weekly outperformance of 3%; in the rare instances when the VIX spiked 50% or more, the average outperformance for gold is more than 5%.

Temporary Insurance

In addition to the turn of the season, investors might want to tuck in a bit of insurance given the unusually calm pall that has descended over markets. Regardless of the asset class – stocks, Treasuries, currencies – volatility is bouncing around the lows for the year, suggesting investors are not particularly focused on hedging their accumulated gains. A short-term trade in gold may help preserve those gains in what is turning out to be a decent year.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Russ Koesterich, CFA, is a Portfolio Manager for BlackRock's Global Allocation Fund and Lead Portfolio Manager for BlackRock’s Global Allocation (GA) Selects Model Portfolios and is a regular contributor to Market Insights.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

Commodities' prices may be highly volatile. Prices may be affected by various economic, financial, social and political factors, which may be unpredictable and may have a significant impact on the prices of precious metals. Concentrated investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and the general securities market. A significant portion of the aggregate world gold holdings is owned by governments, central banks and related institutions. One or more of these institutions could sell in amounts large enough to cause a decline in world gold prices. Should there be an increase in the level of hedge activity of gold producing companies, it could cause a decline in world gold prices. Should the speculative community take a negative view towards gold, it could cause a decline in world gold prices.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of September 2025 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2025 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH0825U/S-4786020

© BlackRock

Read more commentaries by BlackRock