The Hidden Tax Trap in Retirement Planning

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTell me if this rings a bell. You worked hard your entire life. You maxed out your 401(k) every single year of your career and invested those assets inside your employer 401(k).

Now it’s time for retirement. Inside your 401(k) and other retirement accounts you have nearly $2mn, which combined with your Social Security, is supposed to be enough to maintain your lifestyle in retirement.

There’s just one problem. Your lifestyle isn’t changing, which means your tax bracket isn’t either. And every dollar that you take out of your retirement accounts is taxed as well.

All of a sudden what should have been a relaxing retirement is now stressful. Spending needs adjusted. Investment strategies need to change. The travel, home improvement, and other lifestyle plans are scrapped.

This isn’t an uncommon scenario. At the core of the problem are retirees who overly concentrated savings into qualified accounts. While initially saving on taxes, now that they are retired they must withdraw from them to fund their lifestyle. And in doing so, face the unspoken consequence that every dollar distributed is taxed at their nominal tax rate.

Retirement Income Is More Taxed Than You Think

Most people believe that when they retire they’ll be in a lower tax bracket. It’s the core of the “deferred tax” argument for retirement savings, and the reasons millions put money into qualified retirements (e.g. 401k, IRAs, Roth IRAs, etc.) every month. But in reality, that’s not always the case, and more commonly, it is a significant risk factor when planning for retirement.

That’s because assets in tax-deferred accounts like 401(k)s and traditional IRAs, while growing tax free, are subject to taxes when withdrawn. So, every dollar taken out is taxed as ordinary income. And unlike capital gains, there’s no preferential treatment. What that means for anyone retired (or getting ready to retire) is that you may need anywhere from 1.2x to 1.3x more money than you think for retirement, since every dollar taken out will likely be taxed at 20% – 30%.

Now layer in Required Minimum Distributions (RMDs), which begin at age 73 (for most people). These force you to withdraw a set amount every year, whether you need the cash or not, triggering even more taxable income. And with RMDs, the larger your account, the larger the RMD, the more you pay in taxes, and the less money you keep.

Example: Robert’s Retirement Tax Burden

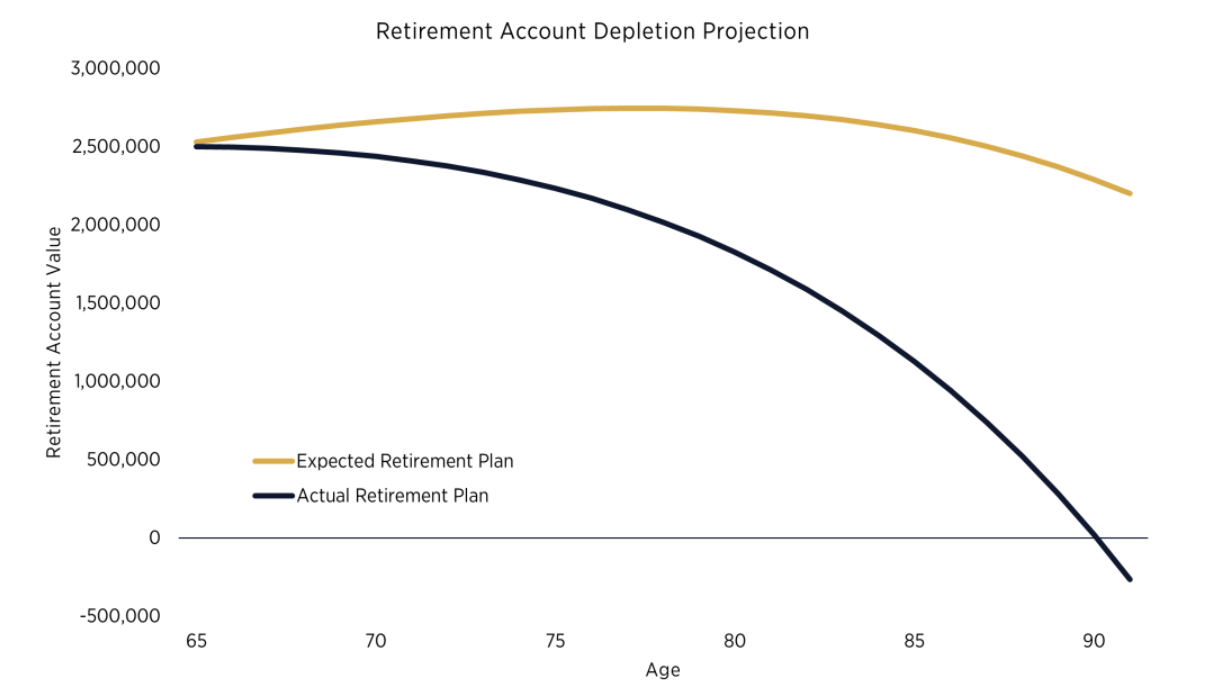

Consider Robert, a successful executive who retired at 65 with $2.5 million split between his 401(k) and traditional IRA. Based on his lifestyle he needs $150,000 annually (before tax) to maintain a comfortable life. He receives $30,000 from Social Security (net of Medicare and taxes), which means he needs to withdraw $120,000 of spendable income from his qualified accounts now. That means he’ll need to withdraw more than $120,000 in order to pay the taxes and still be left with enough to cover living costs. (And due to inflation he’ll need to withdraw even more in the future.)

When planning for retirement Robert thought he’d be in a low tax bracket. But in reality, due to Medicare premiums, phaseouts, and the marginal rate effect, his effective tax rate will likely be close to 20%.

That means Robert must withdraw nearly $150,000 to net $120,000 after taxes. And on a portfolio of $2.5mn, that means he’ll need to earn an additional 1% in annual return just to cover the taxes.

Over a retirement that difference compounds. And more importantly, the additional distributions each year impact his portfolio’s ability to grow. This means there is now longevity risk for him (the scenario where you outlive your assets).

Strategies to Control Taxes in Retirement: Roth IRAs and Beyond

The good news? Even if you’re already retired there are potential solutions. There are tax-smart strategies that can reduce your lifetime tax bill and give you more control, there are investments that can generate tax efficient income, and there are ways to invest in assets that can provide income “blockers” (for tax purposes).

That said, to properly optimize your tax liabilities you will need to coordinate between tax, legal and investment advisors. But if done properly it can be the difference between enjoying a comfortable retirement, and running out of money.

Below are a few of the strategies we regularly use with clients to help control their tax liabilities in retirement.

1. Roth IRA Conversion Ladders

Strategy: Convert portions of your traditional IRA or 401(k) to a Roth IRA each year, especially in lower-income years before Social Security and RMDs begin. This can help to spread your tax liability over time and creates a future pool of tax-free income.

Downside: You’ll need to pay the taxes upfront for every dollar converted into the Roth IRA, which is why it’s important to work with an advisor to structure the conversion ladders. Read our recent post about Roth IRA conversions in retirement to learn more.

2. Tax-Efficient Reinvestment

If your RMDs exceed your spending needs, reinvest the excess into tax-efficient vehicles that can offer preferred income treatment, or even block income (i.e. income is classified as return or capital, or they provide pass-thru depreciation losses):

Some strategies include:

- Municipal bonds

- Tax-managed mutual funds or ETFs

- Private Investments with K-1 loss pass-thru

- Real Assets

3. Asset Location Optimization

Align asset types with account types to optimize income treatment. By controlling the amount of income taxed at your nominal tax rate you can limit your tax liability. Strategies include:

- Place growth-oriented or tax-efficient assets in taxable accounts.

- Review tax treatment for income from “high income” ETFs and mutual funds. Ensure it qualifies for “qualified dividend” treatment, or preferential income taxation.

- Place private investments with pass-thru losses into taxable accounts.

- Put ordinary income-generating assets (REITs, taxable bonds) in IRAs or 401(k)s.

-

Keep Roth IRAs for the highest-growth assets you won’t need for a long time.

4. Block and Balance Strategy

Pair qualified withdrawals with:

- Long-term capital gains from brokerage accounts

- Roth IRA withdrawals

- Cash value loans (if applicable)

This reduces your taxable income in any given year and smooths your overall tax exposure.

Part III: Robert’s Example Revisited — The Power of Planning

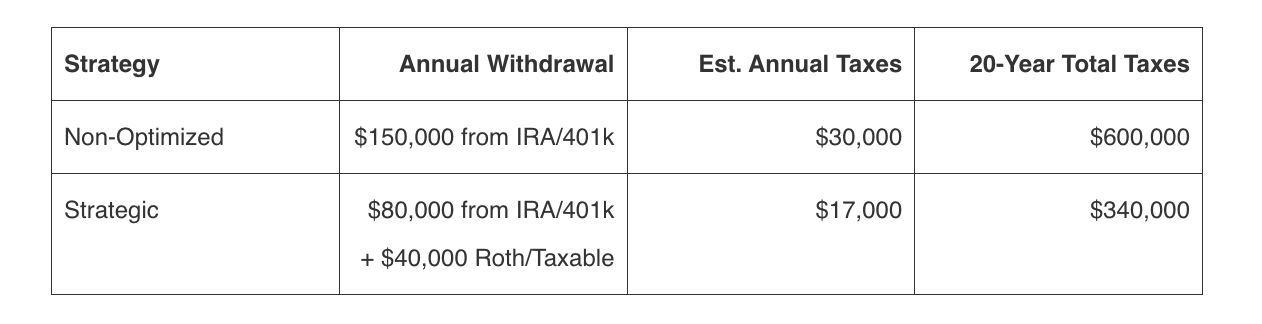

That’s a $340,000 tax savings—money that can be reinvested, compounded, spent, or left as a legacy.

Act Early to Reduce Tax Burdens

If you’re approaching retirement with million-dollar-plus qualified accounts, or you’re already retired and worried about the tax burden, we can help. It’s important to start your retirement planning now before RMDs begin and Social Security complicates the income picture.

The sooner you start planning for retirement taxes the more time you’ll have to implement solutions.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All