At the Midway Point: Returning to the Fundamentals

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- While geopolitical developments continue to make headlines and bear scrutiny, the underlying fundamentals of the U.S. economy remain resilient, warding off recession fears.

- Although the Federal Reserve appears to be still skewed toward rate cuts later this year, Chair Powell acknowledged that monetary policy remains “well-positioned,” and there’s “no hurry” to cut rates.

- The Treasury 10-Year yield is expected to remain at an elevated, “normal” level with heightened headline and data dependency producing continued volatility.

- We believe the bond portfolio decision-making process could benefit from taking an active-passive barbell approach from a solution standpoint.

- Stocks have upside catalysts that include robust lending activity, a muted oil price reaction to the Iranian conflict and a generally stable labor market.

The Macro Backdrop

Geo-Alpha

Liberation Day seems like a lifetime ago. But the 90-day pause is almost over, and—thus far—there are few deals that have been consummated. The countdown to July 9—the deadline for trade deals—is on, and markets will be particularly keen to see who makes a deal and what those deals entail. Rumors abound about the countries that are close to coming to terms with the Trump administration, but rumors do not sign the paper. That is the primary risk facing markets, that—much like Liberation Day—there are negative surprises on the horizon for the conclusion of the negotiation period. Certainly, exemptions and exceptions will happen, and some trading partners are going to come out the other side with a positive relationship and economic outlook. The questions outstanding are who and to what extent. And the answers are critical to understanding global asset market dynamics for the remainder of 2025 and 2026.

The “One Big Beautiful Bill” made its way through D.C. There are numerous elements to the bill that warrant attention. But the evolution of the State and Local Tax deduction (SALT) is acutely important. The provision for up to $40,000 is critical for consumers—a significant tailwind to middle- and upper-middleincome consumers. SALT is widely harangued as being a benefit to “blue states,” but “red states” will benefit as well (evidenced by the New York Congressional Republicans backing the SALT language). There are also provisions allowing businesses to 100% expense Research and Development costs, providing a potential boost to innovation in the future.

Taken together, there are positives and negatives coming from the combination of trade and tax deals. It will be important to understand who and what benefits from them, and whether or not they are meaningful to markets. Trade deals will be crucial to understanding the future of shifting global supply chains, and the OBBB will be fundamental to understanding the trajectory of the U.S. economy. Neither should be ignored.

Avoiding a Recession

The U.S. economy got off to an inauspicious start to the year, at least from a formal statistical perspective. Indeed, the Bureau of Economic Analysis reported that Q1 real GDP contracted by a modest -0.5%. This disappointing performance gave rise to concerns that a “textbook recession,” or two consecutive quarters of negative real GDP, could be in the offing.

Although “Liberation Day” hadn’t even occurred yet, the January–March data was impacted by tariffrelated developments, at least from a trade perspective. Specifically, a surge in pre-tariff imports overwhelmed other positive components of the GDP report, resulting in the negative outcome. Interestingly, underlying demand, consumption and investment were visibly on the plus side of the equation.

That was in the past; where do we go from here? Based on available data, it looks like the import surge was reversed in Q2, and we can get back into positive territory. With labor market activity remaining relatively solid, the underpinnings exist for the U.S. economy to potentially avoid any policy-related pratfalls that could be coming on the tariff front in the second half of the year. In fact, the focus could very well shift to any potential stimulus that could occur as a result of the passage of the “One Big Beautiful Bill.”

Against this backdrop, we maintain as a base case that a recession can be avoided but fully acknowledge that the probability of an economic downturn has not gone away completely. However, on the “other side of the trade,” the markets are not priced at all for a scenario where growth surprises to the upside.

Inflation: Will Disinflation Be Short-Lived?

The latest inflation readings have no doubt underscored that disinflation appeared to be a prominent trend in the second quarter. The cooling of price pressures from the goods side of the equation had been expected, for the most part. A more interesting and perhaps more important development has been that services-related inflation has finally shown some easing.

Indeed, in our opinion, shelter-related costs in reports, such as the Consumer Price Index (CPI), had been overstated for quite some time, and we have been anticipating some lessening here, impacting the overall services component, accordingly. Going forward, investors should potentially expect basically the opposite of the inflation trends outlined above. In other words, any tariff-related price increases would be more likely to show up in the goods sector of the economy, while services could be more neutral on overall inflation trends.

The potential challenge going forward will be to see if the markets can look through any tariff-induced increases to inflation and focus instead on underlying demand pressures. In addition, as Fed Chair Powell recently stated, another key factor to consider is whether any potential increase in prices will be short-lived or have more of a persistent impact.

Either way, the Fed’s 2% target continues to be elusive.

Fed Policy: In No Hurry

As expected, the Fed did not make any changes on the rate front at the June FOMC meeting. The policy maker did tweak its outlook in both the policy statement and updated Summary of Economic Projections (SEP). Within the policy statement, the voting members adjusted their language by now saying that “uncertainty has diminished” versus “has increased further.” With respect to their economic/ inflation forecasts, real GDP growth was dialed back a bit, while inflation was dialed up a bit. The closely followed dot plot remained at two rate cuts for this year, but the 2026 outlook was downshifted from two decreases to basically just one.

Powell & Co. continue to reiterate that monetary policy is “well positioned.” However, the chairman’s comments seem to focus more on the inflation aspect of their dual mandate as he maintains that labor market conditions “remain solid.” In other words, the Fed is in no hurry to cut rates.

Bottom line: The macro setting allows the voting members to take a deliberate approach to monetary policy. In other words, the song remains the same, i.e., the Fed is data-dependent and can let the data “come to them.” Against this backdrop, a reasonable-case scenario still involves potentially one to two rate cuts this year.

Equities: A Bull Market With Stretched Fundamentals

According to Yardeni Research, the S&P 500’s bottom-up earnings estimate for 2025 is $263.43. Should that come to pass, it would bring this year’s growth rate to a very achievable 7.0%.

The 2026 estimate is more of a stretch. The consensus is penciling in earnings of $300.09. That should be tough to come by because it would mean growth of nearly 14% next year. Still, FY2 earnings estimates are frequently sky-high; almost all serious strategists wink at each other on these things, then mentally revise down. If earnings come in around $280–$285 or so in 2026, that would be just fine for most observers.

Nevertheless, at face value, these figures put the market’s P/E multiple at 24.8x, 23.2x and 20.3x earnings for 2024, 2025 and 2026, respectively. At earnings of $280, the multiple is 21.8x.

Those valuations are what you get when the S&P 500’s V-shaped reversal from its April 8 lows sends the market up 23% in less than three months. Suddenly, the S&P 500 finds itself in its fourth go at the 6,100 level (it is trading at 6,103 as we write). The first attack on this territory came in early December as the market got excited about Trump’s election. It then took a routine breather before running back to current levels twice again in February. Now here we are again, with “Sell in May” having fizzled and a fourth onslaught of 6,100. The more this happens, the harder the cement grows on this level, be it support or resistance.

We are observing a few promising developments that will be critical if the market is to support a valuation that is pushing nearly 25x last year’s earnings. We could end up eating crow on this, but it appears that almost everything we ever read, ruminated on and heard about Iran’s threats of closing the Strait of Hormuz went out the window in the last few weeks.

Whether the year was 1990, 2000, 2010 or 2020, we have all read our share of Hormuz Doom-mageddon think pieces, with seemingly every one of those putting $200 oil on the radar. Instead, what we really got out of this year’s Hormuz threat, the boldest on record, was Brent crude mustering a half-hearted rally. Additionally, the Energy sector itself couldn’t even take the leadership baton amid Israel’s bombing of Iran’s nuclear facilities. To wit, over the last month, the S&P 500 Energy sector has been ranked just 4th among the 11 sectors.

Right or wrong, and we are thinking “right,” the market is coming to a belief system that has Middle East wars having minimal effect on the vagaries of the stock market, at least prior to prior cycles. This is a far cry from the action in 1990, when Iraq went after Kuwait, sending stocks down. September 17, 2001, when markets first reopened after the terror attacks, also comes to mind. The Middle East simply moved markets more back then than it does now, largely due to the United States’ more secure oil supply/demand profile these days relative to the pre-shale era.

Meanwhile, prognostications of recession will have to wait. We are heartened by lending activity. For example, the YoY rate of growth in small bank loans bottomed in March at +2.8%. It ticked a tad higher in both April and May, to +3.3%. We saw similar action in this indicator in 1991, 2010 and 2021. The first two of those episodes preceded nine years each of heady stock market gains. Then again, the bears know well what happened to stocks in 2022 (the NASDAQ, to use the poster child, fell 30% top-to-bottom).

Something else is promising for stocks: our concerns about bond market ructions affecting order and continuity are gently dissipating, though the market is far from out of the woods. For example, we’ve long been bullish on Japan, but spring ushered in summer with that country’s bond market having a freak-out. It wasn’t that long ago, 2022 to be exact, when Japan’s 30-Year bond traded south of 1%. It first breached 2% in May 2024, then continued up to a high last month of 3.17%. It has since settled at 2.88%. Similarly, the U.S. long bond changed hands at as high as 5.1% this spring before stabilizing at 4.77%.

We continue to remain keen on Japan. The country’s “shareholder yield payout ratio,” which combines buybacks and dividends as a fraction of earnings, has risen to 61%. For context, MSCI China and the S&P 500 each have a shareholder yield payout ratio of just 40%. Broad Japan’s shareholder yield itself is 4.0%, akin to levels observed two months after Lehman failed and double the 2% on offer in the S&P 500. The gap between the two is the widest in our proprietary PATH software’s dataset, which dates to 2006.

Additionally, more than half of Japan’s large caps have an earnings yield that is at least 400 bps north of what is available on the 10-Year sovereign bond. In contrast, only about one in five S&P 500 names sport that type of margin of safety over U.S. t-notes.

China could be an interesting case, though we remain underweight to the country in our Model Portfolios. The country’s stock market came to life last autumn: MSCI China has outperformed the MSCI USA Index since September 13, 2024. We think that both China and Korea had a “What about me?” moment in 2023–2024. That’s when those two large economies both realized it was time to tag along with Japan on a push for corporate governance reform, which was the catalyst for the latter’s bull market in recent years. Those themes remain “on” in the second half.

As for Europe, we have reason to believe the direction of the euro’s exchange rate, currently $1.18, will be the primary driver of European equities in the second half. On that score, partly because bearish sentiment on the dollar is at multi-year extremes, we are dollar bulls.

To give you an idea of how lopsided things are, Bank of America’s June Fund Manager Survey found the percentage of respondents who say they are overweight to the dollar to be at the lowest level since January 2005. This result is corroborated by the heavily followed ZEW survey, which just posted its most bearish U.S. dollar response since the question was first posed in 2012. We do not believe the dollar’s status as global hegemon is going away anytime soon. Put us down for a USD relief rally this summer.

Fixed Income: "Normal" Rates, but with Volatility

There certainly have been a lot of headlines/news thrown at the U.S. Treasury (UST) market this year. At times, it has functioned as expected in terms of “risk-on/risk-off” situations, but at other times, yield movements have been a bit more unexpected. It is not because the global investment community has altered its broader premise of Treasuries being a store of value, but rather market participants trying to navigate their way through the heightened levels of uncertainty on many fronts. In fact, through April (Liberation Day), Treasury Department data revealed that foreign holdings of Treasuries had increased year-to-date, led by Japan and the UK. With respect to China, its UST holdings were down only slightly, -$1.8 billion or -0.2%.

As the calendar flips to the second half of the year, and perhaps tariff-related uncertainty goes into the rearview mirror, the UST focus will turn more and more to the macro fundamental backdrop, i.e., the economy, inflation and Fed policy. We expect the UST 10-Year yield to remain in its more historically “normal” territory (elevated, as compared to its pre-COVID-19/COVID-19 levels) but with heightened volatility remaining a visible part of the trading landscape.

Just like the Fed, the UST market is highly datadependent for yield direction. If fiscal policy comes back into focus, there could be dueling forces to contend with, like the potential for both rate cuts and higher budget deficits.

Opportunities in Asset Allocation

Fixed income investors reversed course in the second quarter. Treasury yields rose, and credit spreads tightened, supported by resilient economic data and reduced concern over aggressive tariff implementation. Municipals received greater support as fears around the repeal of tax exemptions subsided, and seasonal issuance pressures ebbed. Despite the broader reversal, three themes remained intact from the first quarter:

- the coupon portion of the Treasury curve continued to steepen

- the dollar weakened against both developed and emerging market currencies

- EM local debt outperformed.

So, where does this leave us? We are feeling:

- A bit more confident in the trajectory of growth,

- Somewhat more relaxed—though not fully resolved—on the impact of tariffs,

- Increasingly concerned about geopolitical risks and

- Assured that the municipal bond tax exemption remains intact.

Still, changes in perspective are only a tweet away, and investors must remain alert. Conviction remains challenging in this environment.

The base-case scenario we adopted in the beginning of the year—incremental Fed easing, a resilient economy and reasonably anchored inflation expectations—persists largely intact and argues for little change in our fixed income asset allocation. Securing diversified sources of income remains a key consideration for investors for the rest of 2025.

Corporate bonds remain a core income source but have now returned to valuation levels that are historically tight. Fundamentals continue to be strong, and many corporations have taken proactive measures to defend against tariffs. We maintain our current positioning with a focus on quality screened credits but could look to add incremental allocations if spreads widen from current levels.

Our principal overweight within taxable fixed income remains securitized debt, where we see attractive valuations and the potential for volatility to ease somewhat in the months ahead. It remains the largest overweight allocation within our income-focused strategy, reflecting both relative value and our view on risk-adjusted returns. We see value in agency RMBS as well as broadening opportunities for value investors in non-agency supported debt.

Positions in emerging local debt have long featured as diversifiers in our less-conservative fixed income models. While currency returns may be less of a tailwind for these positions in the coming months, the carry advantage of emerging market local positions relative to the developed market ex-U.S. sovereign debt is sizable and presents an interesting option for investors looking to diversify their bond exposure outside the U.S.

Within tax-aware portfolios, we think municipals offer a great deal of value. Yields are attractive, credit fundamentals remain solid, and the threat to the municipal tax exemption has passed. Technicals also turned positive, with the seasonal rush of issuance behind us. We prefer stable revenue sectors such as public utilities and water and sewer credits to opportunities offered by general obligation credits.

WisdomTree Asset Allocation Views

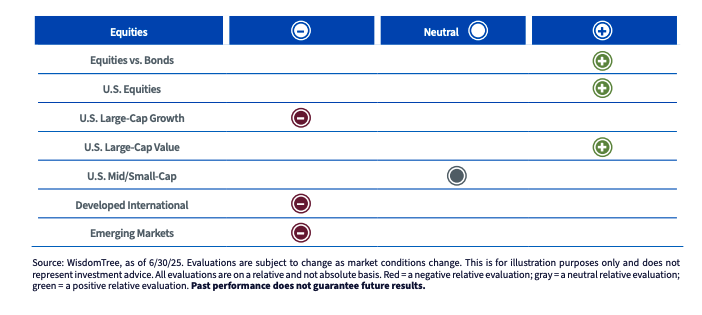

Equities

- Favor equities over bonds, emphasizing high-quality stocks for their relative defensiveness versus expensive market-cap leaders.

- Potential equity catalysts this quarter include easing Middle East tensions, subdued investor positioning and ongoing disinflation that could support Fed rate cuts.

- The U.S. market’s high-quality profile and sector composition may warrant a higher long-term multiple versus history and other regions.

- Maintain overweight to U.S. and underweights to broad ex-U.S. equities, with targeted overweights to Japan and India driven by compelling structural growth themes.

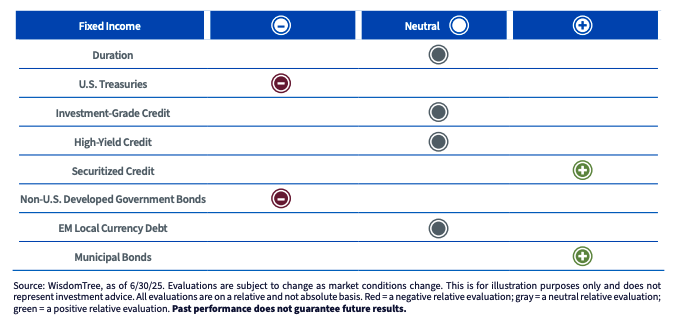

Fixed Income

- Interest rates are likely to stay structurally higher, with volatility driven by shifting macro data and policy signals.

- Given a highly data-dependent Fed, we maintain a neutral duration stance.

- Corporate credit fundamentals remain strong, though spreads have compressed to historically tight levels.

- Securitized credit continues to offer more attractive relative value opportunities.

- While currency tailwinds may fade, EM local debt offers an attractive carry advantage versus developed international bonds for investors looking to diversify beyond the U.S.

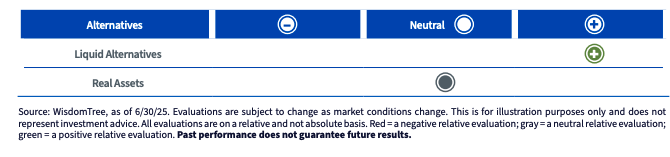

Alternatives

- For investors who are hesitant to reduce their allocation to equities and fixed income, efficient-core strategies may provide an innovative solution to free up capital for alternative strategies.

- With the possibility that stock-bond correlations could remain in positive territory, we believe trendfollowing and other liquid alternative strategies can play an important role in multi-asset class portfolios.

- We continue to favor strategies that seek to generate uncorrelated returns in periods of heightened volatility.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

IMPORTANT INFORMATION

Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund before investing. For a prospectus or, if available, the summary prospectus containing this and other important information about the Fund, call 866.909.9473 or visit WisdomTree.com/investments. Read the prospectus or, if available, the summary prospectus carefully before investing.

Foreign investing involves currency, political and economic risk. Investments in emerging markets, real estate, currency, fixed income and alternative investments include additional risks. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. In addition, when interest rates fall, income may decline. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuers ability to make such payments will cause the price of that bond to decline. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates but may decline in value. Investing in mortgage- and asset-backed securities involves interest rate, credit, valuation, extension and liquidity risks and the risk that payments on the underlying assets are delayed, prepaid, subordinated, or defaulted on.

This material contains the opinions of the authors, which are subject to change, and should not be considered or interpreted as a recommendation to participate in any particular trading strategy or deemed to be an offer or sale of any investment product, and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein.

WisdomTree Funds are distributed by Foreside Fund Services, LLC.

Kevin Flanagan, Rick Harper, Jeremy Schwartz and Jeff Weniger are registered representatives of Foreside Fund Services, LLC.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All