Key points

-

Meet the new bond: Persistently above target inflation, structurally higher debt and deficits, and lower global dollar recycling mean traditional fixed income may offer less reliable diversification and heightened volatility with more muted return potential than in the past.

-

Alpha over beta: Strategies harnessing the volatility and dispersion arising in this environment can potentially generate uncorrelated alpha to better position portfolios’ diversification and returns.1

-

10 years of SMS: A decade in, BlackRock's Systematic Multi-Strategy Fund (“SMS” - ticker BIMBX) has helped investors pursue enhanced diversification and return potential across a range of market environments.

Today’s investment landscape, shaped by persistently above-target inflation, structurally higher debt and deficits, and reduced global dollar recycling into US financial markets, has contributed to elevated market volatility alongside historically high policy uncertainty. In this environment, portfolio returns and diversification have come under pressure, particularly for investors relying primarily on traditional equity and fixed income exposures.

Yet this challenging environment also creates opportunities for alpha-seeking strategies able to take advantage of heightened volatility and dispersion. SMS combines directional fixed income exposure with differentiated alpha strategies seeking to enhance portfolio diversification and return potential—whether as a complement to traditional fixed income or as a core liquid alternative.

As SMS marks its 10-year anniversary, its innovative approach has never been more relevant to portfolio construction. We reflect on how the strategy has helped investors navigate a wide range of investment challenges over the past decade, and why it may be uniquely positioned for what’s ahead.

The growing need for alpha in portfolios

The macroeconomic and market dynamics that largely supported steady, low volatility returns from broad market indices and beta exposures through the post-Global Financial Crisis (GFC) cycle have shifted significantly in recent years. Today, investors are faced with elevated fiscal, policy, and macroeconomic uncertainty that is contributing to frequent bouts of market volatility and more muted return potential.

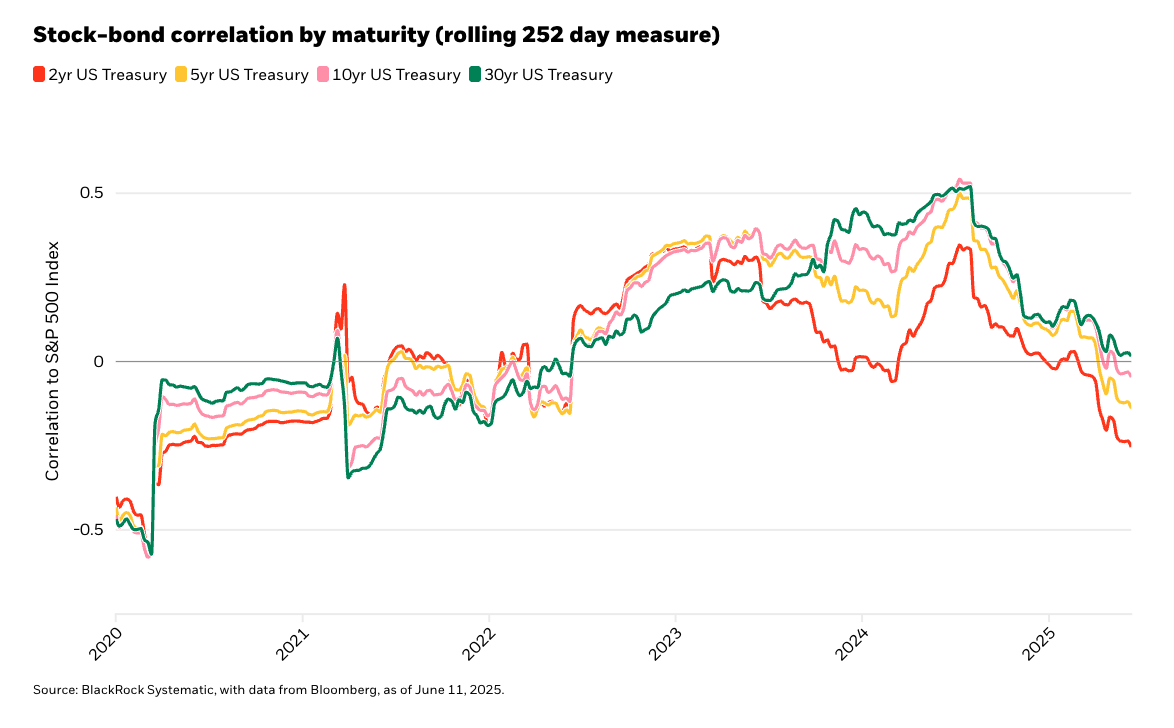

At the same time, bonds are facing structural headwinds that challenge their role as a reliable portfolio hedge. Rising fiscal deficits, elevated debt financing needs, and the prospect of more persistent above target inflation are among the forces that could continue to constrain their diversification potential. As the chart below illustrates, the historically negative correlation between stocks and bonds has weakened, with longer maturities providing the least effective ballast during recent risk-off periods.

The underperformance of longer maturity bonds as diversifiers underscores a broader shift in the traditional bond market structure that has historically supported returns. Specifically, term premia (the difference between long- and short-dated bond yields) had been steadily declining over much of the past 40 years. However, today’s fiscal and monetary (inflationary) pressures are now driving a steady rise in term premia, undermining both the returns and diversification benefits of longer maturity bonds, which were once among the most effective portfolio diversifiers.

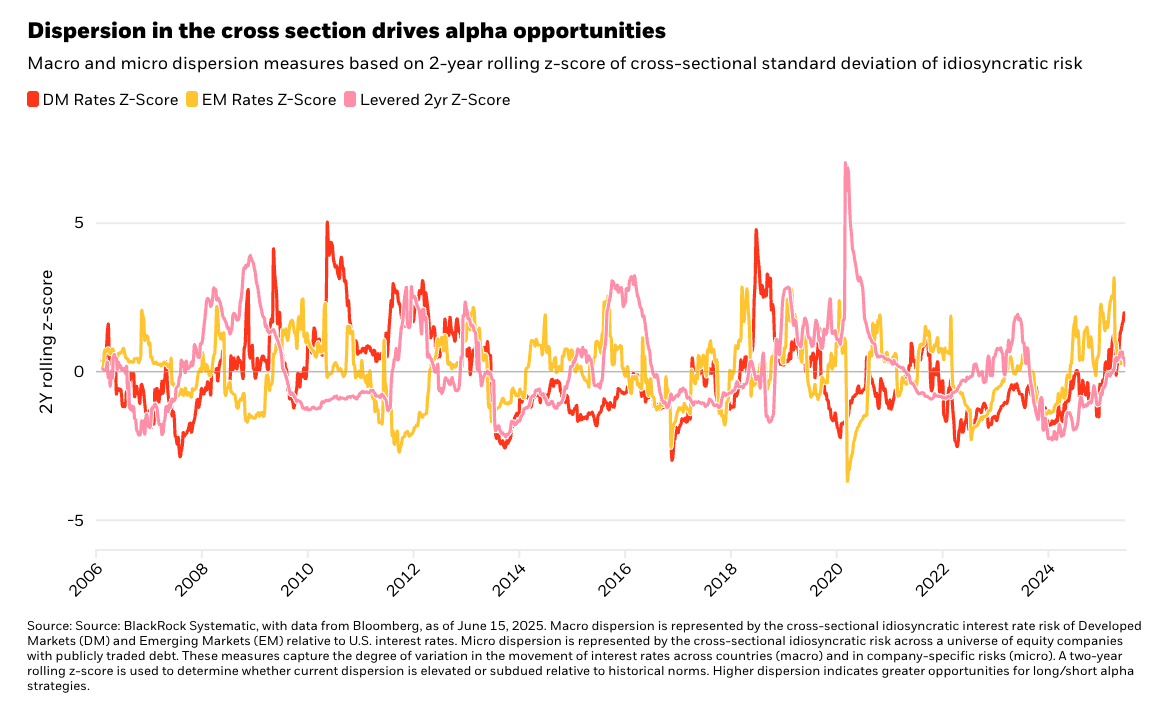

While market volatility and uncertainty can limit directional opportunities, the cross-section of markets offers a rich source of return potential. As the chart below illustrates, cross-sectional dispersion reflects the varying macroeconomic and policy environments. At critical periods, this dispersion highlights opportunities driven by divergence in company performance and macro exposures. In the current environment, elevated dispersion reflects heightened policy uncertainty—creating a key return source for long/short strategies such as SMS’s alpha strategies. This enhances their ability to potentially generate diversifying and defensively oriented returns.

An origin of innovation

Today’s market environment validates the original vision behind SMS: to deliver a more resilient and consistent source of returns with strong diversification properties—the role so effectively played by traditional fixed income in the past—but now challenged.

To achieve this, we drew on the full breadth of our systematic investing platform built over the past 40 years. A key strength of our systematic process is its ability to deliver targeted outcomes through the precise combination of innovative, complementary strategies. A decade ago, we set out to deliver targeted strong risk-adjusted returns with low volatility, limited beta to broad asset classes, and a defensive posture during periods of equity market stress. In doing so, we built an alternative source of diversification, whether as a core liquid alternative or a complement to traditional fixed income.

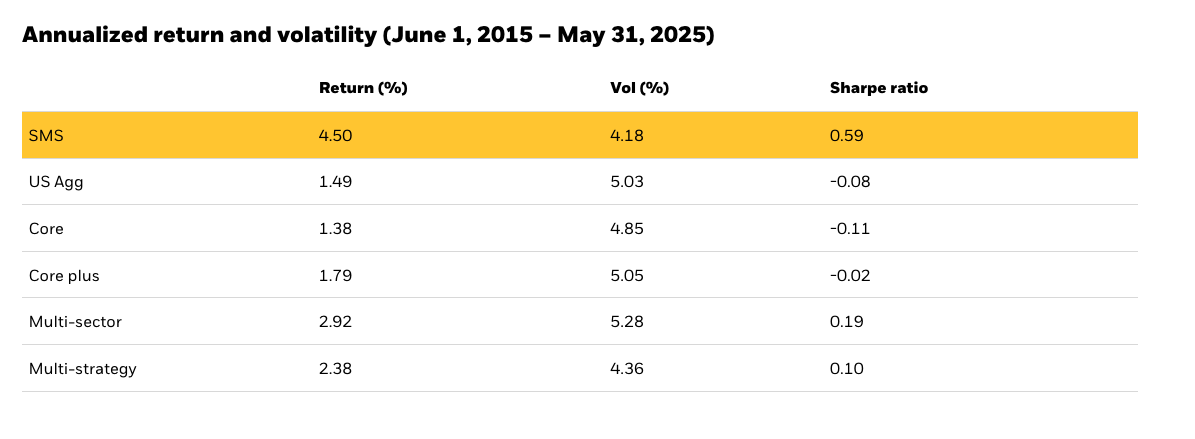

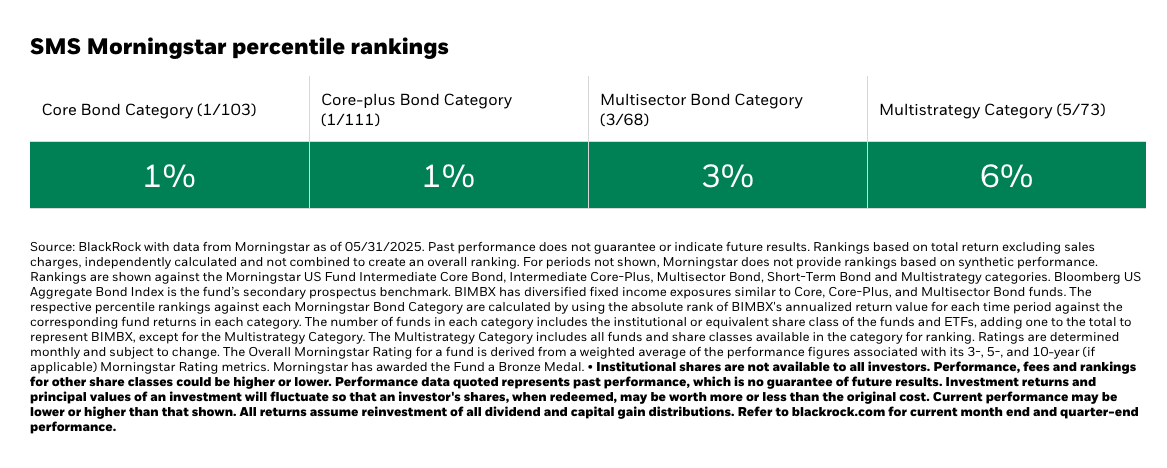

A decade later, combining our long-only fixed income expertise with some of our most unique and defensively-oriented alpha strategies delivered on these objectives. Over the past decade, SMS has generated an annualized return of 4.50% on annualized volatility of 4.18% for a Sharpe ratio2 of 0.59, and a beta of 0.11 to the S&P 500. This performance places it in the top decile of its Morningstar category, as well as among the top decile across several comparable bond categories.

The advantage of bonds + alpha

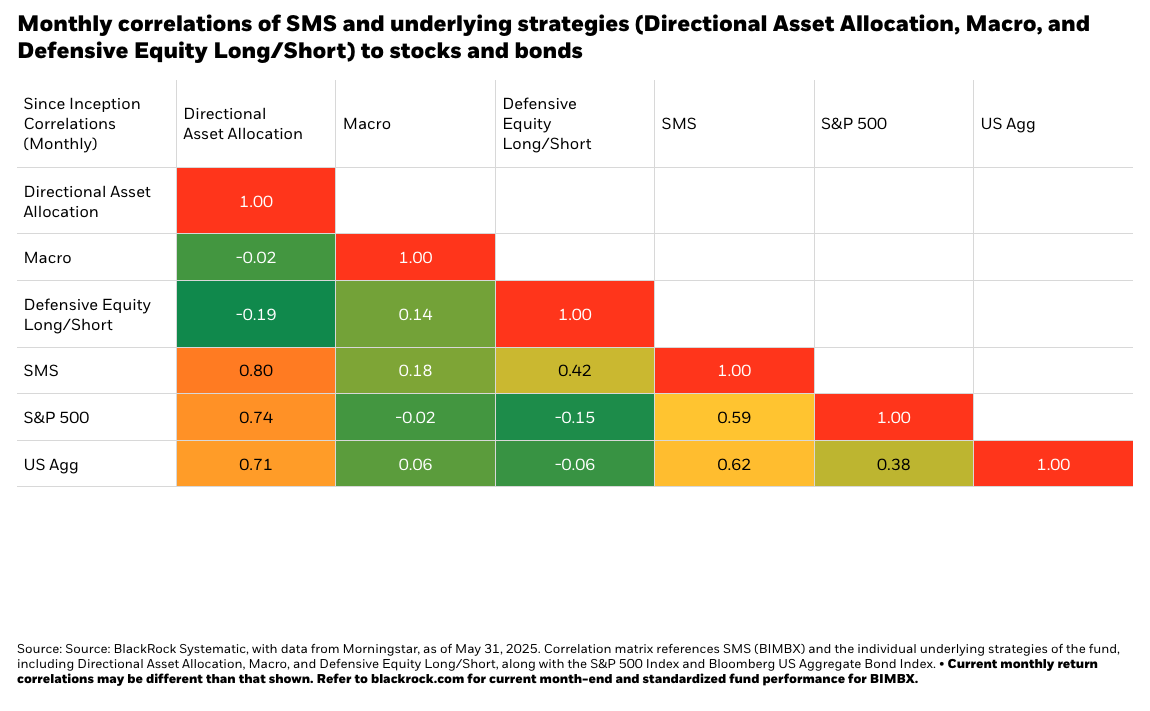

SMS is unique in its deliberate combination of return sources—distinguishing it not only from other liquid alternative funds but also from traditional bond funds.

At its core, SMS takes targeted credit and interest rate risk. The fund allocates across traditional fixed income sectors such as high yield, investment grade, securitized credit, and agency mortgages, while also actively managing duration and yield curve exposure. This means that at the fund level, SMS exhibits fixed income characteristics like yield and duration.

We combine that long-only fixed income exposure with pure, defensive alpha strategies across macro rates and equity markets. These strategies are long/short and market neutral, structured to take idiosyncratic risk rather than directional market risk. This makes them complementary to the beta portion of the portfolio, offering sources of return that are designed to behave independently across market environments.

In essence, these complementary (and often negatively correlated) strategies are intended to work at different times for different reasons, seeking to bring greater balance, diversification, and resilience to the overall portfolio. The complementary nature of these strategies’ low and negative correlations means that performance can be less reliant on things that traditional fixed income funds typically rely on—including excess risk and yield, market timing, and duration anticipation—potentially leading to more consistent, reliable and repeatable returns.

A decade of showing up when it’s needed most

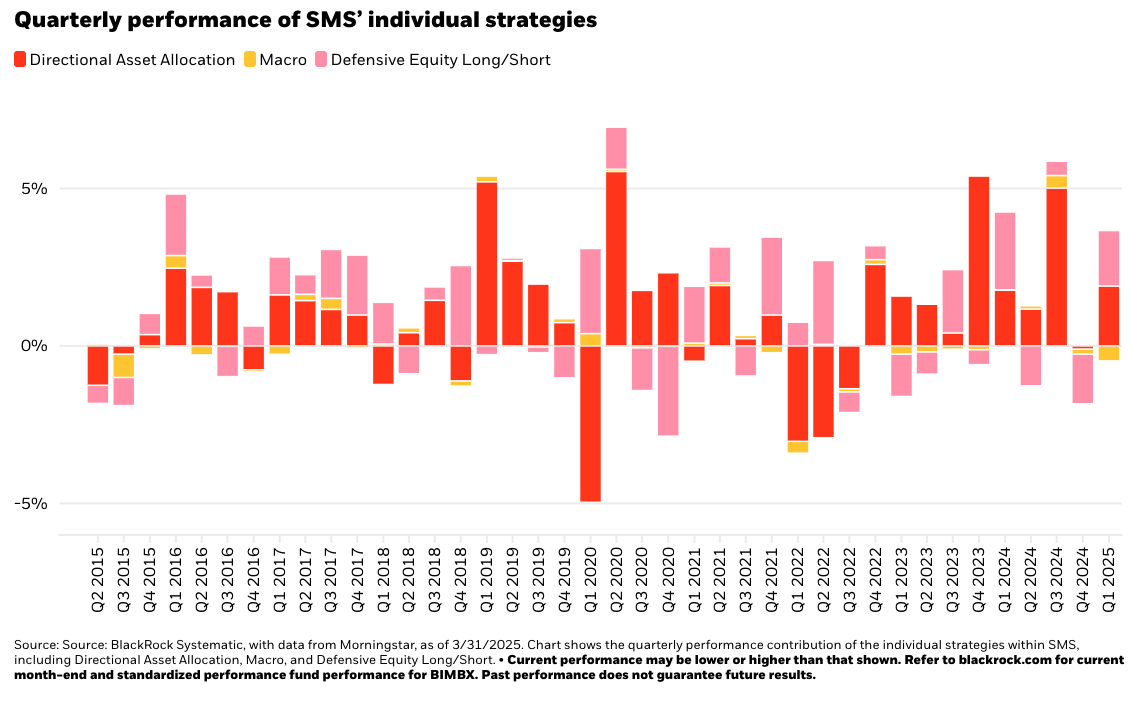

Over the past decade, SMS has demonstrated its ability to deliver across a range of market environments, with its individual strategies performing as designed.

Example 1: when growth fears hurt equity markets

In October 2018, equity markets sold off sharply amid rising US-China trade tensions and growing concerns about global economic growth and corporate earnings. During this period of heightened volatility, SMS demonstrated its role as a core alternative strategy by providing meaningful equity diversification. Its combination of long-only fixed income exposure and defensive alpha strategies helped dampen portfolio risk at a time when equity markets struggled. SMS ended the quarter up 0.94% versus the S&P 500 which was down 13.5%.3

Example 2: when unprecedented events drive steep sell-offs

In early 2020, the onset of the COVID-19 pandemic triggered one of the fastest and most severe market drawdowns in history. The S&P 500 Index fell more than 30% in just a few weeks as global uncertainty spiked and investors rushed to de-risk. SMS’s strategies performed as they were designed to, including its defensive equity long/short strategy which has a track record of strong performance during periods of market stress. This is due to the strategy’s application of credit-oriented insights in equity markets, enabling it to provide resilience during times of extreme turmoil, when dispersion rises and investors turn to companies with healthy balance sheets and strong cash flows.

This downside risk mitigation helped offset losses from risk assets, allowing SMS to deliver a 3% return from January through April, while the S&P 500 ended the same period down 10%.4

Example 3: when bonds no longer behave as expected

In 2022, investors faced a painful scenario: both stocks and bonds declined sharply, undermining the 60/40 portfolio and exposing the limits of bonds as a reliable diversifier in a new investment regime. With inflation surging and interest rates rising at the fastest pace in decades, the Bloomberg U.S. Aggregate Bond Index posted its worst annual return in history—falling over 13%—alongside steep equity losses.5 This environment highlighted the role that SMS can play as a resilient complement to traditional fixed income. While bonds failed to cushion equity declines, SMS provided an uncorrelated, defensive return stream as an added source of diversification beyond traditional duration.

The above examples underscore how SMS has performed across a range of challenging market environments. This has made it a valuable option for investors seeking both core alternative exposure and a complement to traditional fixed income. From 2015 to 2022, BIMBX grew from virtually zero assets to $10 billion—reflecting its broad adoption as a tool for navigating market complexity and addressing portfolio construction challenges.6

Navigating the next 10

As SMS enters its second decade, its relevance in today’s evolving investment landscape has never been clearer. With traditional sources of return and diversification under pressure, SMS offers a differentiated approach—combining fixed income exposure with defensive, alpha-driven strategies. Its history of being able to navigate complex market conditions positions it as a compelling option for investors seeking to build more resilient portfolios for the decade ahead.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

1 Alpha: Returns generated through active management, above and beyond market returns. Beta: The portion of returns explained by general market movement.

2 Sharpe ratio: A measure of risk-adjusted return. A higher Sharpe ratio indicates better return for the level of risk taken.

3 Source: BlackRock Systematic, with data from Bloomberg, Q4 2018 performance. Past performance is no guarantee of future results.

4 Source: BlackRock Systematic, with performance data from Bloomberg.

5 BlackRock Systematic, with performance data from Bloomberg for 2022.

6 Source: BlackRock Systematic, AUM data from 2015 to 2022.

Investing involves risk, including possible loss of principal.

Key risks of BIMBX: The fund is actively managed, and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Principal of mortgage-or asset-backed securities normally may be prepaid at any time, reducing the yield and market value of those securities. Obligations of US government agencies are supported by varying degrees of credit but generally are not backed by the full faith and credit of the US government. Non-investment grade debt securities (high yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher rated securities. Investments in emerging markets may be considered speculative and are more likely to experience hyperinflation and currency devaluations, which adversely affect returns. In addition, many emerging securities markets have lower trading volumes and less liquidity. The fund may use derivatives to hedge its investments or to seek enhanced returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility.

Effective 1/4/19, the Alternative Capital Strategies fund name was changed to the “Systematic Multi-Strategy Fund”.

Diversification and asset allocation may or may not protect against market risk or loss of principal.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change. This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. Reliance upon information in this material is at the sole discretion of the viewer.

The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective. The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

Prepared by BlackRock Investments, LLC, member FINRA.

©2025 BlackRock, Inc. or its affiliates. All Rights Reserved. iSHARES and BLACKROCK are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH0625U/S-4596770

© BlackRock

Read more commentaries by BlackRock