In the world of retirement planning, target-date funds (TDFs) have become the default investment vehicle for millions of Americans. Yet, despite their widespread adoption, one of the most critical components of these funds—the glide path—is often overlooked in the selection process.

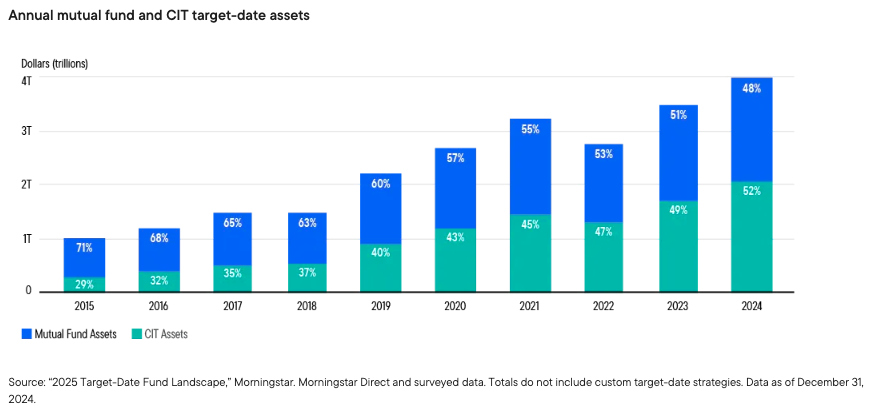

Target-Date CIT and Mutual Fund Assets Continue to Grow at a Steady Pace, Reaching $4 Trillion in Assets at the End of 2024

Why? Because retirement outcomes depend on more than just a date

At its core, a glide path is the investment roadmap that guides participants from their early career through retirement. By guiding asset allocation decisions, it determines how much risk participants take at each stage of their journey. But not all glide paths are created equal.

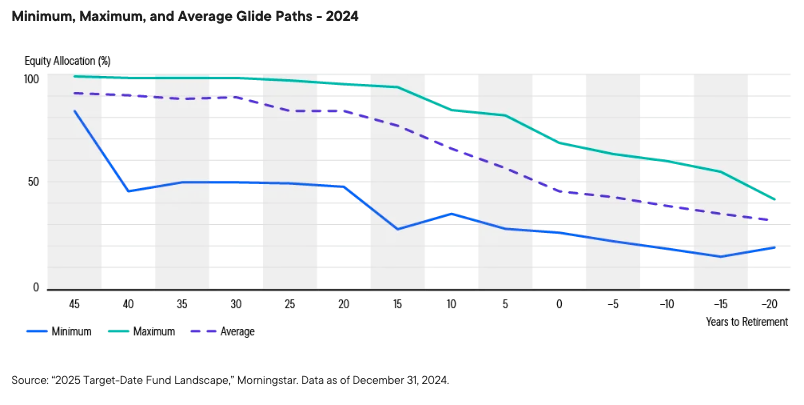

All target-date managers must decide how to prioritize the same retirement saving risks: shortfall, sequence and longevity. Target-date glide paths vary based on how different managers address these often-competing risks. This choice is a good thing for advisors and sponsors, as it lets them match a glide path with their preferences and with each plan’s needs. But navigating more than 100 different glide path strategies creates a daunting task for any advisor or sponsor.

The prioritization challenges described above have caused our industry to use unhelpful labels such as “to vs. through” and “aggressive” or “conservative” to describe target-date funds or their “landing points”—the point at which glide path driven asset allocation changes are no longer made. Such generalizations are not helpful, just like assuming all members of the same generation share the same characteristics is not a helpful perspective.

The following chart provides a visual representation of the discussion in the previous three paragraphs:

If we truly care about participant outcomes, we must look beyond fees and brand names. We must ask: Does this glide path reflect the needs, behaviors and risks of our participants?

How? By aligning glide path design with participant realities

We believe a differentiated glide path should:

-

Account for participant behavior, not just theoretical models.

-

Balance growth and protection through dynamic risk management.

-

Extend support beyond retirement, recognizing that retirement is a phase—not a finish line.

In our view, it’s critical to incorporate the use of real-world data, behavioral finance insights, and advanced modeling to build a glide path that adapts to the evolving needs of today’s workforce.

What? A better way to evaluate TDFs

For retirement plan advisors and consultants, this means evolving the TDF selection process:

Ask deeper questions: What assumptions underly this glide path? Are they realistic for our participant base?

Demand transparency: Can the manager explain how their glide path performs across different market environments and demographic groups?

Prioritize outcomes: Look at projected income replacement, drawdown risk and longevity support—not just historical returns.

Time to rethink the default investment

Glide path design is not a footnote—it’s the foundation. After all, there are more than 100 glide paths to consider in the Morningstar 2025 “Target-Date Fund Landscape.”

As fiduciaries, we owe it to participants to ensure that the default option is not based on a broad, unhelpful label, but truly aligned with their investment objectives.

We suggest you differentiate target-date strategies through a new lens. There’s more to a glide path than a simple fixed income and equity allocation.

See what separates glide paths with this tool (for financial professionals only).

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Principal invested is not guaranteed at any time, including at or after a fund’s retirement target date; nor is there any guarantee that the fund will provide sufficient income at or through the investor’s retirement. The investment risk of the retirement target fund changes over time as its asset allocation changes. Investments in underlying funds are subject to the same risks as, and indirectly bear the fees and expenses of, the underlying funds.

Equity securities are subject to price fluctuation and possible loss of principal. Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Alternative strategies may be exposed to potentially significant fluctuations in value.

Active management does not ensure gains or protect against market declines.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as, investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

© Franklin Templeton

Read more commentaries by Franklin Templeton