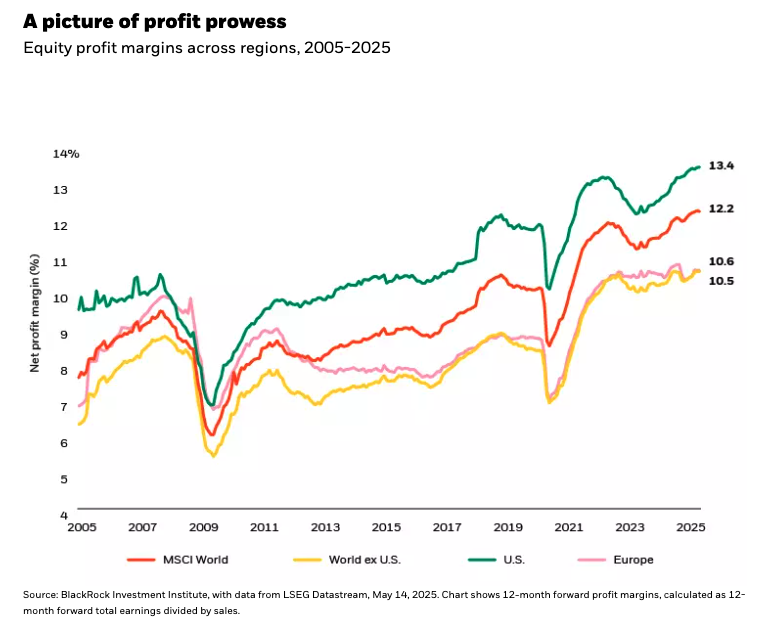

The Q1 2025 earnings season showed us that U.S. companies started the year in a position of strength. Earnings for the S&P 500 grew more than 12% year-over-year and sales expanded by 4.4%. Earnings outgrowing sales means that a strong period of U.S. profit margin expansion continues – a point I highlighted after Q4 2024 results came in. See the chart below. First quarter earnings were recorded before the tariff uncertainty shook markets in April. Yet we know that, overall, companies should be able to absorb the shock of potentially higher prices and slowing demand.

A focus on earnings also helps investors avoid the danger of trading on volatile newsflow. The recent market recovery highlights the importance of staying invested and shows the opportunities that can be seized upon by fundamental equity investors when valuations drop.

The Q1 season also revealed the level of nervousness around equities amid geopolitical uncertainty. The share prices of companies that missed expectations were hit harder than they have been historically, while optimistic guidance was rewarded. This shows the value of in-depth company knowledge during times of volatility.

Here are three areas that caught our eye during the recent earnings season, all of which we believe are fertile areas of active opportunity:

1. Big tech defies the doubts

Earnings for the “Magnificent 7” grew around twice as much as those of the S&P 500, as big tech shook off any doubts that began to emerge after the Chinese “DeepSeek” artificial intelligence (AI) model demonstrated impressive performance in January.

We believe AI is a powerful long-term investment theme that will evolve and present opportunities for skilled stock pickers. Big-tech capital expenditure on AI investment showed no signs of slowing down in Q1. Some of the hyperscalers, such as Meta and Amazon, announced that capex was accelerating, while Microsoft and Google reiterated forecasts. We estimate the total for all hyperscalers for 2025 will be more than $370 billion, up from $230 billion in 2024, while operating cash flows stand at $739 billion. Crucially, hyperscalers are beginning to see returns on investment. Meta CEO Mark Zuckerberg said, “AI is transforming everything we do.”

This investment is likely to flow through all areas of the AI technology stack, from data centers and power generation up to software and applications. Our tech team expects software companies to benefit as the technology becomes more readily available.

The DeepSeek news and recent tariff tumult show that many companies in this space were priced for perfection. Yet recent pullbacks have presented opportunities for long-term investors to lean into the AI theme at an attractive price.

2. How about healthcare?

Healthcare earnings jumped by 44% versus Q1 2024, as positive developments were seen across subsectors from pharma to insurance. Yet uncertainty surrounds the sector due to government announcements on drug prices and volatile tariff policies.

Most of the uncertainty concerns large-cap pharmaceutical companies, an area we have been underweight due to the persistent risk of patent cliffs. We prefer to lean into companies that specialize in medical devices and supplies, which benefit both from the stable earnings growth driven by ageing populations, as well as growth spurred by innovation. Some of the innovations here include AI-powered surgical robots, minimally invasive platforms and smart wearables.

Our healthcare analysts also spend a lot of time researching how trade uncertainty may hit healthcare earnings. Drug distribution companies, such as Cencora and McKesson, may be less impacted by tariffs than the broader sector.

And many of these opportunities are available at an attractive price, in our view. Healthcare remains cheap, at a 30% discount versus the S&P 500 – whereas historically healthcare stocks have traded at a premium to the market.

3. A focus on financials

The best performing sector globally in 2025 has been the financial sector, driven by the continued boost from higher interest rates. U.S. financials delivered solid, if unspectacular, results in Q1 2025, growing earnings by just more than 6%. Despite these slightly lacklustre numbers, we believe momentum in the sector can continue, and our global financials team remains overweight the U.S. versus other regions. Economic activity and interest rates are in the sweet spot for bank profitability; increased investment is driving loan growth and capital market activity; and operating costs in the industry are decreasing on the back of AI adoption.

Bottom line

I wrote one quarter ago that U.S. “exceptionalism” was still alive and well. The subsequent months of market volatility caused many to question this label. The latest earnings season once again demonstrated the persistent strength of U.S. companies, and we believe there are opportunities across sectors to find quality companies capable of thriving even in periods of great uncertainty.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Earnings figures cited herein are from BlackRock Fundamental Equities, with data from Refinitiv and FactSet as of May 2025, with 460 companies (87% of S&P 500 market cap) reporting. Year-over-year figures compare currently reported data to full-quarter data one year prior and are subject to change.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of May 2025 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results.

Investing involves risk. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Diversification does not ensure profits or protect against loss.

Prepared by BlackRock Investments, LLC, member FINRA.

©2025 BlackRock, Inc or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH0525U/S-4540868

© BlackRock

Read more commentaries by BlackRock