An old investing adage is to "buy the rumor, sell the news." Looking back at the first-quarter gross domestic product (GDP) and earnings reports published last week gives us a sense of how the economy and companies fared as the "rumors" tied to April 2 tariff announcement uncertainty began to take effect. Looking ahead, the potential buying or selling by investors in the second quarter may depend on how the news of tariff negotiations progress during the 90-day tariff delay that began April 9.

First-quarter GDP

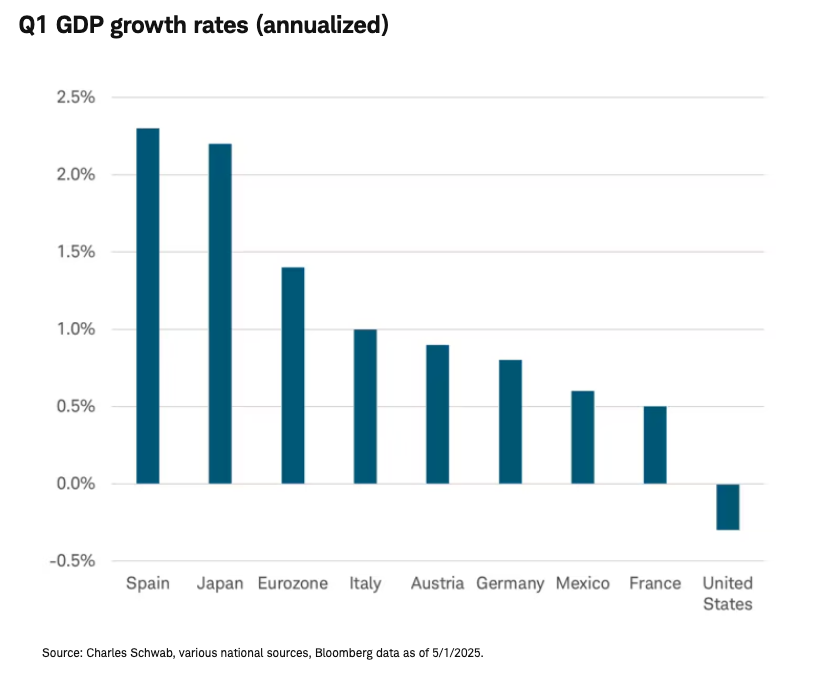

Last week, many major countries released the initial reading of first-quarter GDP. Eurozone Q1 GDP expanded by 0.4%, or an annualized 1.4% to put it on the same basis as U.S. GDP is reported. That was double what was expected and double the increase in the prior quarter. Gains were broad-based among economies, with Germany and France, the region's two largest economies, returning to growth after declines in the fourth quarter. The weaker-than-expected Q1 decline in U.S. GDP was largely attributable to a surge in U.S. imports ahead of the April tariffs. Yet, the better-than-expected growth in Europe may not have been due to a surge in exports to the United States.

While we don't know the exact contribution from net exports to GDP in the preliminary release from European countries last week—those details will follow in the next update on May 23—we know from the press releases that they were either not much of a factor and may have even been a drag on Europe's major four economies.

-France's press release noted net trade (exports less imports) was a drag of -0.4%.

-Italy's press release also noted a negative contribution from net exports.

-Spain's press release showed net trade contributed just +0.2%.

-Germany's press release did not mention trade as a factor but noted that "both household final consumption expenditure and capital formation were higher than in the previous quarter."

Ireland's strong GDP growth of 13.4% on an annualized basis likely reflected a sharp rise in exports to the United States (more likely due to pharmaceuticals). But the eurozone's GDP would have been better than expected even without Ireland's contribution (Ireland's economy only makes up 3% of the eurozone economy). Therefore, there is not a reason based on U.S. exports to believe Europe's economy will necessarily give back the stronger growth in Q2.

First-quarter earnings

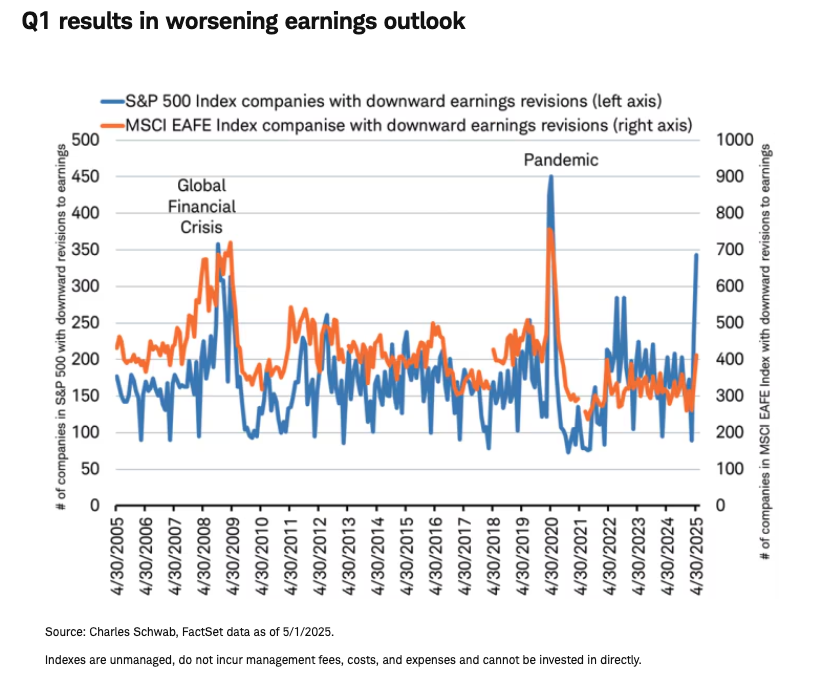

The earnings picture for Q1 is also brighter outside the United States. Last week was the peak for the earnings reporting season when companies release their earnings results and guide analysts on their outlook for the coming quarters. The number of companies in the U.S. S&P 500 with downward earnings revisions to future quarters is similar to the Global Financial Crisis and the COVID-19 pandemic. But for non-U.S. companies it is still within a normal range and nowhere near past crises peaks. That may be due to the U.S. the tariffs posing a potential supply shock, while for other countries it poses a potential demand shock—and it is easier to replace lost demand with domestic stimulus than it is to replace missing supplies with new factories, materials, and workers. This may help to explain why non-U.S. companies have been performing much better than U.S. stocks this year.

Second quarter

What might Q2 look like when GDP and earnings are released? That will likely depend on the progress of trade talks during the 90-day pause of many of the most disruptive tariffs that began on April 9. Since the April 2 tariff announcement, the Trump administration has claimed it is engaging in tariff negotiations with over 70 countries. Last week, Treasury Secretary Bessent said the U.S. has put China to the side for now as it focuses on trade deals with between 15 to 17 other countries.

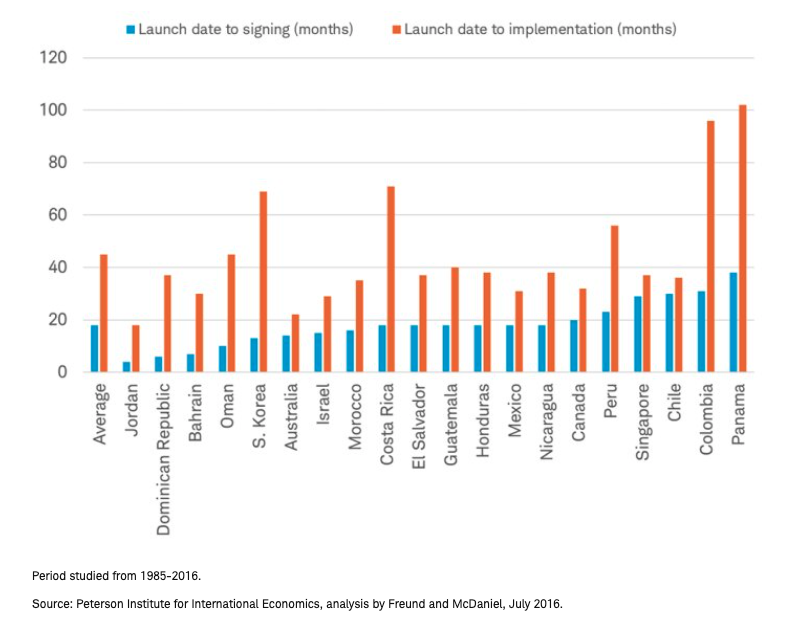

Frameworks for deals could be forthcoming but may not end uncertainty. Talks with India, Japan, and South Korea have been described as making good progress. However, these frameworks, or memorandum of understanding (MOUs), may describe the topics to be addressed in eventual deals and may not have a lot of details. This could set up an extension of the 90-day pause past July 9, keeping a cloud over corporate decision-making and markets. From 1985 to the start of President Donald Trump's first term in 2017, the average U.S. trade deal has taken 18 months before the deal was signed and 45 months before it was implemented, according to Apollo Global and the Peterson Institute for International Economics.

It takes 18 months on average to sign a trade deal and 45 months to implement

Japan

On the evening of the tariff day of April 2, President Trump said that he is "open to tariff negotiations if other countries offer something phenomenal." Back in 2019 he literally called the updated trade agreement with Japan "phenomenal" and a "tremendous" agreement. Yet, the U.S. and Japan announced a negotiation in September 2018 and deal was signed in October 2019, a year later. That was faster than 18-month average, expedited by a friendly relationship between then Prime Minister Abe and President Trump. It is hard to imagine a deal happening this time in just 90 days. The comment late last week by Japanese finance minister Kato that Japan's $1.1 trillion of U.S. Treasuries will be "on the table" in negotiations with the U.S. illustrates the high stakes for both sides.

Canada and Mexico

Mexico and Canada were in the crosshairs of President Trump's initial tariff threats, but the agreement has ultimately provided a degree of protection, with many goods still entering the U.S. tariff-free. Mexico's President Sheinbaum indicated last week on X that "We agreed that the secretaries of the Treasury, finance, economy and commerce will continue working in the coming days on options to improve our trade balance and advance outstanding issues for the benefit of both countries." Mexico is the U.S.'s largest trading partner with most exports to the U.S. coming from U.S.-headquartered companies operating in Mexico, like GM, making trade negotiations more about the operations of U.S. businesses than factors directly under the influence of the Mexican government.

Now that Canada's election is out of the way and Prime Minister Carney and President Trump plan to meet in the "near future," we may soon see how a renegotiation of the United States-Mexico-Canada Agreement (USMCA) may look. However, the relationship is not friendly with Carney's campaign benefitting from Trump continuing to question Canada's sovereignty. The White House commented on Carney's win, with deputy press secretary Anna Kelly saying: "The election does not affect President Trump's plan to make Canada America's cherished 51st state." During Trump's first term as president, the renegotiation of the North American Free Trade Agreement (NAFTA) into the USMCA took 13 months between the beginning of negotiations in August 2017 and the signing on September 30, 2018, and another 21 months until it went into force on July 1, 2020.

Europe

In early April, European Commission President von der Leyen said the European Union (EU) offered to drop tariffs to zero on cars and industrial goods imported from the U.S. if Trump reciprocated, termed a "zero-for-zero" deal. President Trump declined the deal with a counteroffer referencing the trade deficit with Europe saying, "They have to buy and commit to buy a like amount of energy." Hundreds of billions in cost aside, there likely isn't enough spare U.S. liquified natural gas (LNG) transportation capacity to facilitate transporting the quantity of LNG Europe would need to purchase to satisfy Trump's energy-purchase demand. So there appears to be an impasse. EU governments are unwilling to offer any concrete concessions in return for uncertain commitments from Trump to withdraw recent tariffs on EU sectoral goods, knowing that Trump might simply put them back on again. Full tariffs on EU exports and EU retaliation against U.S. exports may commence shortly after the delay expires on July 9th.

EU officials have been prompted to explore a more constructive trade relationship with China after China lifted earlier sanctions against the European Parliament and other European institutions. Should China offer EU firms World Trade Organization (WTO) rules-based access to new markets and investment into the EU economy, it may act as a buffer to Trump's chaotic trade relations on consumers and businesses. During Trump's trade war with China during his first term, China reduced most favored nation tariffs on the rest of the world, despite duties rising on goods traded between the U.S. and China.

China

On Friday, China's Ministry of Commerce said that it's "evaluating" the possibility of trade talks with the White House, after senior U.S. officials repeatedly expressed an openness to talk about tariffs. That seems far from an eager commitment to de-escalate trade tensions. While both China and the U.S. have exempted some goods from tariffs, those efforts seemed aimed at easing the burden on some domestic businesses rather than being tied to any de-escalation. China is not signaling any domestic pressure to address U.S. tariffs. China's Politburo meeting that concluded on April 25 declined to make major changes to fiscal or monetary policy, and the vice chair of the National Development and Reform Commission on April 27 said policymakers were "fully confident" in reaching the 5% GDP growth target for 2025.

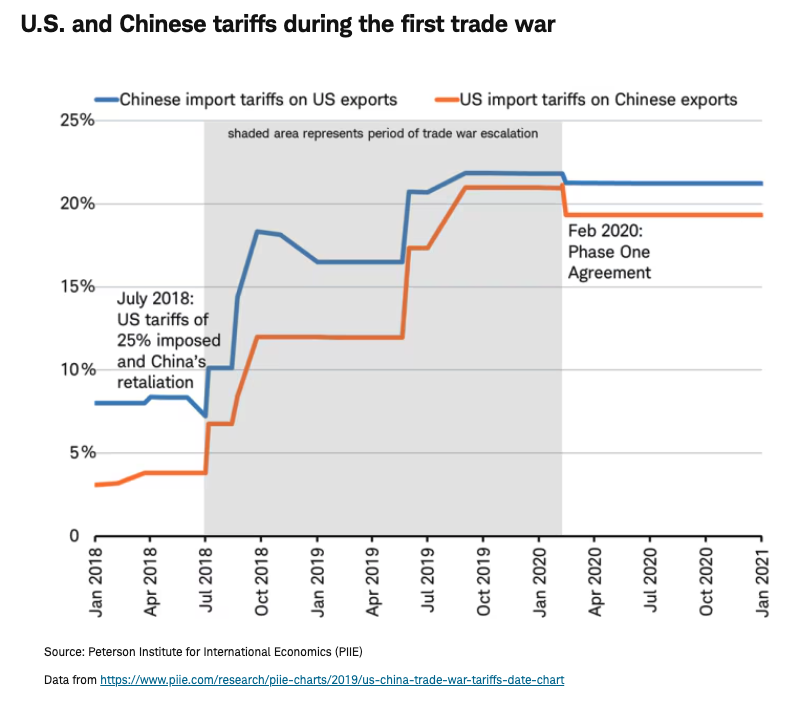

A review of Trump's trade war with China during his first term may be instructive. President Trump threatened China with tariffs during his first campaign, in 2016. During his first year in office, trade investigations into unfair import practices, conducted by the U.S. International Trade Commission began, but tariffs were not implemented until July 6, 2018, when $34 billion of "List 1" of goods were tariffed at 25%. China and the U.S. continued to escalate the trade war over the next five months until Trump and China's President Xi met at a G20 meeting on December 1, 2018, signing a 90-day truce. However, after the 90 days, tariffs escalated again over the next year, until the Phase One trade deal was agreed to on December 13, 2019 and signed on January 15, 2020, going into effect February 14, 2020. This was a 12-month "negotiation" period.

What might trade progress with China look like? Transparent progress in high level discussions, perhaps accompanied by reduction in broad-based tariff levels to 60% or below (the level talked about on the campaign trail), although targeted tariffs or export control on certain sectors or goods could remain.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author"s views as of that date. It will be kept solely for historical purposes, and the author"s opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Diversification strategies do not ensure a profit and cannot protect against losses in a declining market.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg"s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg"s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

© Charles Schwab

Read more commentaries by Charles Schwab