Tax planning for high-income earners isn’t about loopholes; it’s about leveraging the strategies available to you. High earning W-2 employees don’t have the same deductions or write-offs as business owners, but that doesn’t mean they don’t have any tax optimization options.

Here are 7 advanced, but easy to implement, W-2 tax strategies to help reduce taxable income in a compliant way.

1. Maximize Pre-Tax Retirement Contributions

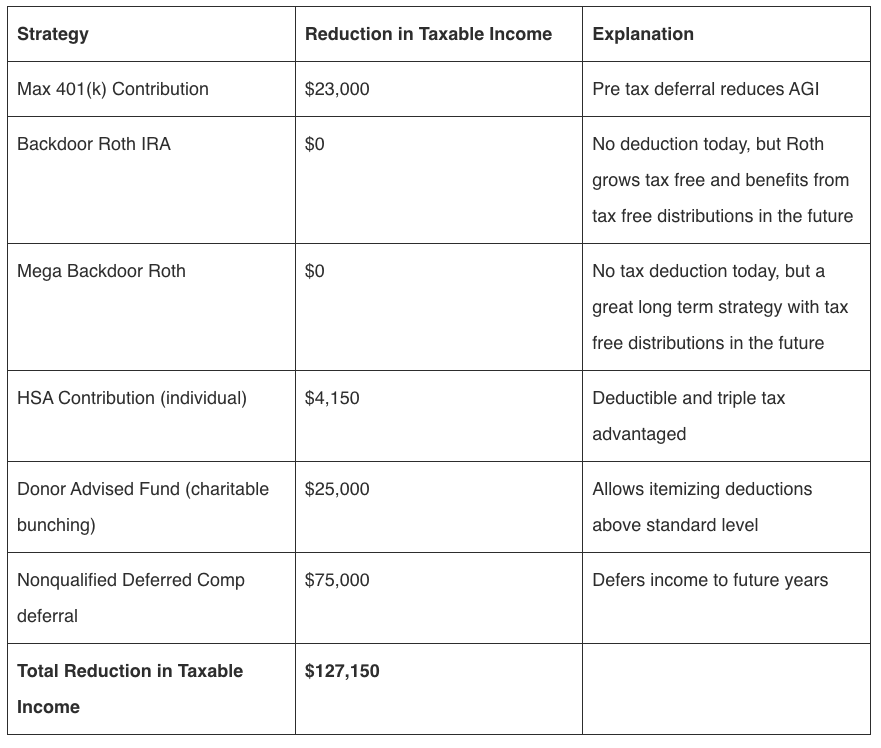

Contribute the maximum to your employer sponsored retirement plans like a 401(k), 403(b), or governmental 457(b). In 2025, the contribution limit is $23,000 (or $30,500 if you’re over 50). These contributions reduce your taxable income dollar for dollar and grow tax deferred, making them essential in any high income tax planning playbook.

2. Backdoor Roth IRA Conversion

If your income is too high to contribute directly to a Roth IRA, consider a backdoor Roth. This involves making a non deductible IRA contribution and then converting it to a Roth. While the conversion is taxable, the long term tax free growth of a Roth can be incredibly valuable, especially if done strategically each year as part of a larger tax reduction strategy.

Note: Make sure to work with your tax and financial advisor when implementing to avoid any pro rata rule implications.

3. Utilize a Mega Backdoor Roth (If Your Plan Allows It)

Some employer plans allow after tax 401(k) contributions above the standard limit, up to $69,000 total in 2025, including employer match. You can then convert the after tax portion into a Roth account. While this doesn’t reduce current taxable income, it’s a powerful tax optimization tool for long term wealth building.

4. Fund a Health Savings Account (HSA)

If you’re enrolled in a high deductible health plan, an HSA offers triple tax benefits: tax deductible contributions, tax deferred growth, and tax free withdrawals for medical expenses. For 2025, you can contribute up to $4,300 individually or $8,600 for a family. It’s a simple yet effective component of W-2 tax strategies.

5. Use a Donor Advised Fund (DAF)

If you’re charitably inclined, a Donor Advised Fund lets you bunch multiple years of donations into a single tax year, often pushing you over the standard deduction threshold. You get an upfront deduction while retaining the ability to distribute funds to charities over time. It’s a high impact tax reduction strategy that aligns generosity with efficiency.

6. Defer Income with Nonqualified Deferred Compensation (NQDC) Plans

If your employer offers one, an NQDC plan lets you defer a portion of your income until retirement or another trigger date. This can push income into lower tax years and reduce your current year liability, a core tactic in high income tax planning.

7. Invest in Tax Efficient Vehicles

Use your taxable investment account to hold assets that are naturally tax efficient, like municipal bonds (which are federally tax free) or ETFs that produce fewer capital gains distributions. If you’re a Qualified Investor consider investing in Real Assets like real estate and buildings that can pass thru losses via K-1s.

Asset location matters; let your accounts work with the tax code, not against it, as part of a broader tax optimization strategy.

Case Study: Reducing Taxes on $500,000 of W-2 Income

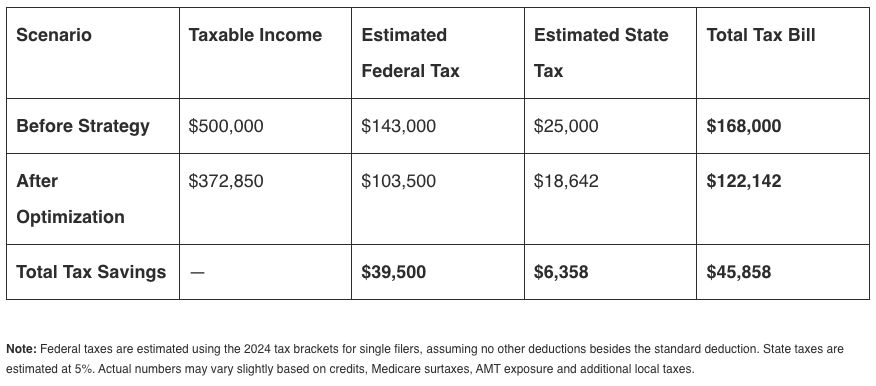

A high earning Senior Executive earning $500,000 in W2 income faced a significant tax burden. Without a proactive strategy to actively reduce their taxable income the individual faced significant taxes, which were going to be compounded by their high earning spouse.

They were already maxing out their 401(k) but hadn’t implemented any additional tax strategies. As a result, their marginal federal tax rate was 35%, and they lived in a state with a 5% income tax rate.

Our team worked with them (and their spouse) to develop an efficient tax strategy for their income. Let’s see what their tax liability looked like before and after implementing a layered tax strategy using some of the tools we covered above.

Step by Step Tax Optimization for 2024

Before vs. After Tax Bill

What’s the Takeaway?

By using a combination of pre tax retirement savings, strategic charitable giving, and deferred compensation, this individual was able to potentially reduce their taxable income by over $125,000 and save more than $45,000 in taxes.

These aren’t complicated maneuvers; they just require proactive planning and the right team in your corner. If you’re exploring W-2 tax strategies or tax planning for high income earners, let Defiant Capital Group help you build a custom plan.

For personalized guidance on tax liabilities and optimizing your wealth, contact Defiant Capital Group today

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group