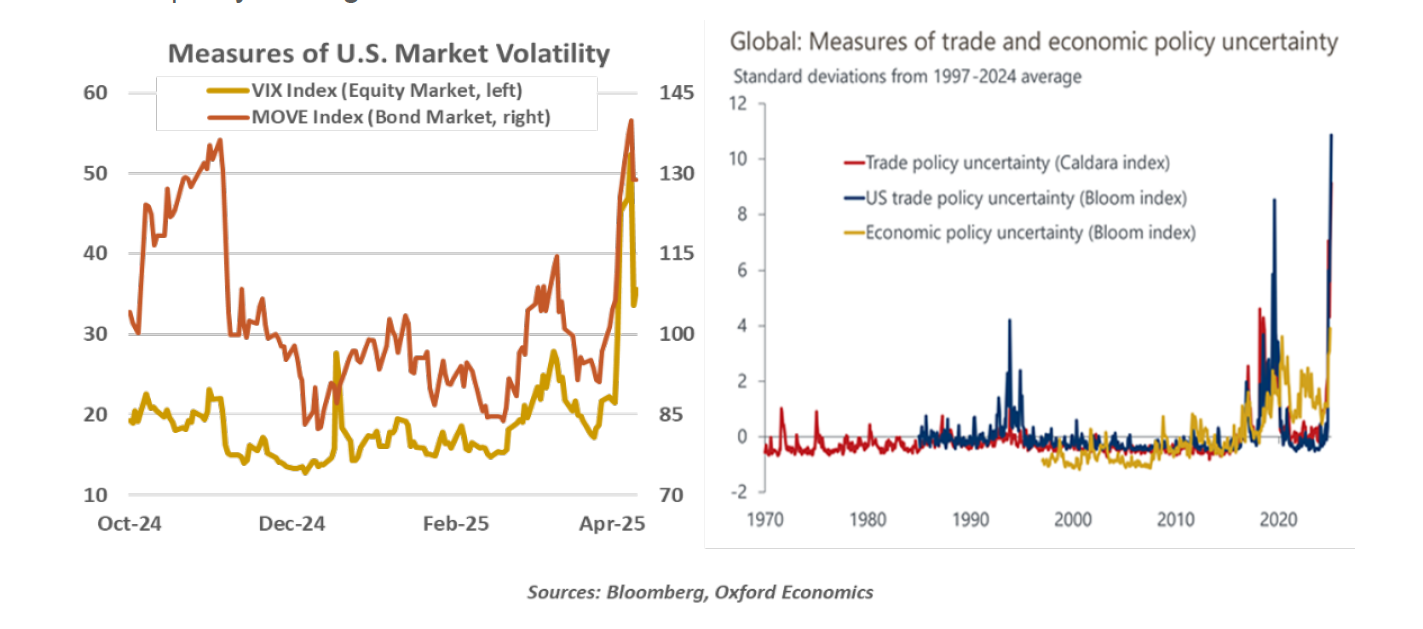

In an unpredictable year, this was the most volatile week yet.

By now, most readers will know the headlines: some of the highly punitive tariffs announced on April 2 in the Rose Garden have been postponed for ninety days. Markets had been wishing for a week that it had all been a bad dream, and rallied on the news. However, the nightmare is not over. Here’s why:

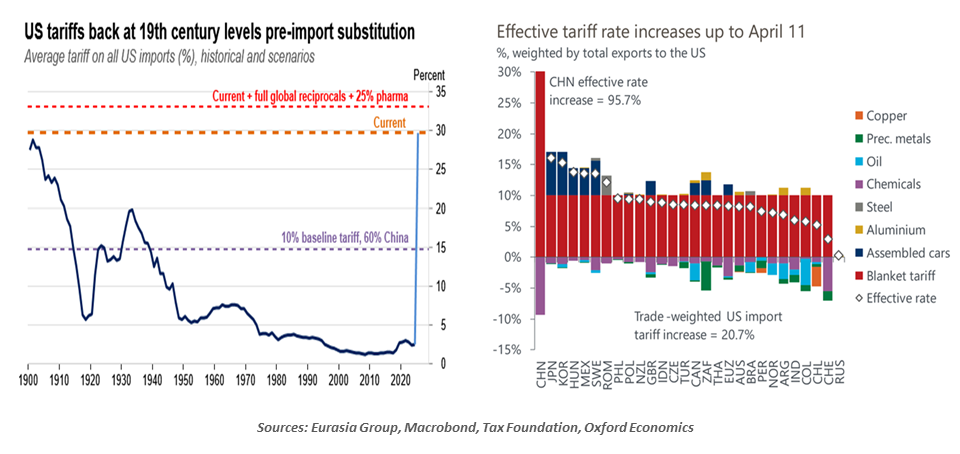

- The reciprocal tariffs (which were not really reciprocal) were only deferred, and not cancelled. There is another cliff event in ninety days.

- Coincident with the temporary suspension of reciprocal tariffs, the rate charged against Chinese imports was raised to 145%. The combination of the two actions will leave the aggregate U.S. tariff rate against all countries at an extraordinarily high level; impacts are now more heavily concentrated on just one trading partner.

- China has retaliated with 125% tariffs on U.S. imports, a particular risk for the U.S. agriculture, chemical and machinery sectors.

- Tariffs on steel, aluminum and autos remain in force. The 10% across-the-board tariff is also still in place. The dispute with Canada and Mexico carries on separately, as do Canada’s retaliatory tariffs. And the White house still aims to end exemptions for pharmaceuticals, minerals, lumber and semiconductors.

The about-face on reciprocal tariffs can be viewed in a positive and a negative light.

The positives: the President did respond to negative feedback, from business leaders and from the financial markets. Until this week, it was not clear that there were any checks on the aggression of the trade agenda.

As well, it appears that moderate voices within the Administration have gained some influence over the trade agenda. Their counsel may bring boundaries and discipline to decision-making.

The negatives: the sequence of events over the past two weeks illustrates the unusual nature of decision-making within the White House. Moves have been rushed out, and then modified. Deadlines are announced, and then extended. Broad announcements are made without adequate allowance for the complexity and nuance that surround trading relationships.

The unpredictability of policy has made it very difficult for businesses to orient their operations, and has caused substantial swings in the financial markets. The S&P 500 stock index, which had lost 12% of its value in the week prior to the pause, regained 9.5% in the hours after the reprieve came through. Bond markets and currency markets have reflected some doubt about the credibility of American policy-making.

Damage to consumer, business, and market confidence may already be irreversible. And when the consequences of tariffs begin hitting retail prices, a negative psychology may be renewed. Impacts on growth and inflation will be more lasting.

Many still expect that increases in tariffs will not be permanent. This is founded in the notion of the President as a deal-maker, a leader who will transition to being more pragmatic after putting the world on notice. But if and when negotiations begin, the initial tone from Washington may make it very difficult for them to conclude successfully.

If one attempts to discern an ultimate goal that is consistent with decisions made to date (however changeable they might be), it is clear that the Administration is resolute in its wish to bring substantial amounts of heavy industry back to the United States. Tariffs are seen as the best tool to bring about this realignment. And leadership appears willing to have the American economy and the American markets bear short-term costs in the hope of achieving long-term gains.

This perspective should serve as an important foundation for business strategy and portfolio construction in the months ahead. We’ll almost certainly be tossed about from time to time, but the direction of travel is clear.

Now, if you will excuse me, I have to get fitted for a neck brace.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Northern Trust

Read more commentaries by Northern Trust