Summary

- Midstream/MLPs have been generating significant free cash flow (FCF) in recent years, and with fee-based business models, companies are able to generate FCF independent of oil and gas prices.

- Even with capex increasing for some names, midstream FCF generation is expected to remain intact.

- Midstream/MLP FCF yields remain healthy, and companies have been allocating excess cash toward growing dividends, pursuing growth opportunities, and opportunistic equity buybacks.

Energy infrastructure companies have been generating healthy free cash flow (FCF) in recent years. This has been a sustained company-level tailwind for the space since 2020/21. Excess cash flow has supported dividend increases and opportunistic buybacks. Growth capital spending has been on the rise for some names. Therefore, it is helpful to dig into FCF yields using 2025 projections. Today’s note looks at FCF yields for MLPs, as well as U.S. and Canadian midstream C-Corps, and how midstream compares to broader energy and the S&P 500.

Free Cash Flow Generation & Its Related Tailwinds

Midstream companies largely reached a FCF inflection in 2020/21. Growth capital began to moderate in 2020 after years of heavy spending to facilitate the boom in U.S. oil and gas production during the 2010s. Simultaneously, companies were reaping the cash flows from completed projects (read more). Rising cash flows and less spending resulted in solid FCF generation for a space that historically had modest or no free cash flow. With excess cash, companies focused on reducing leverage, growing dividends, and repurchasing equity.

Today, there is broad dividend growth among energy infrastructure companies (read more), and several names have equity buyback authorizations (read more). Combined, the total shareholder yields for midstream MLPs and corporations have been generous, albeit with solid equity performance putting some downward pressure on yields (read more).

Digging Into 2025 Estimated FCF Yields

Shifting to 2025, midstream companies are enjoying more robust growth opportunities driven by natural gas and natural gas liquids (NGLs). As a result, capital budgets have been on the rise (read more). With companies pursuing growth projects, investors may be wondering if FCF generation and its related tailwinds remain intact.

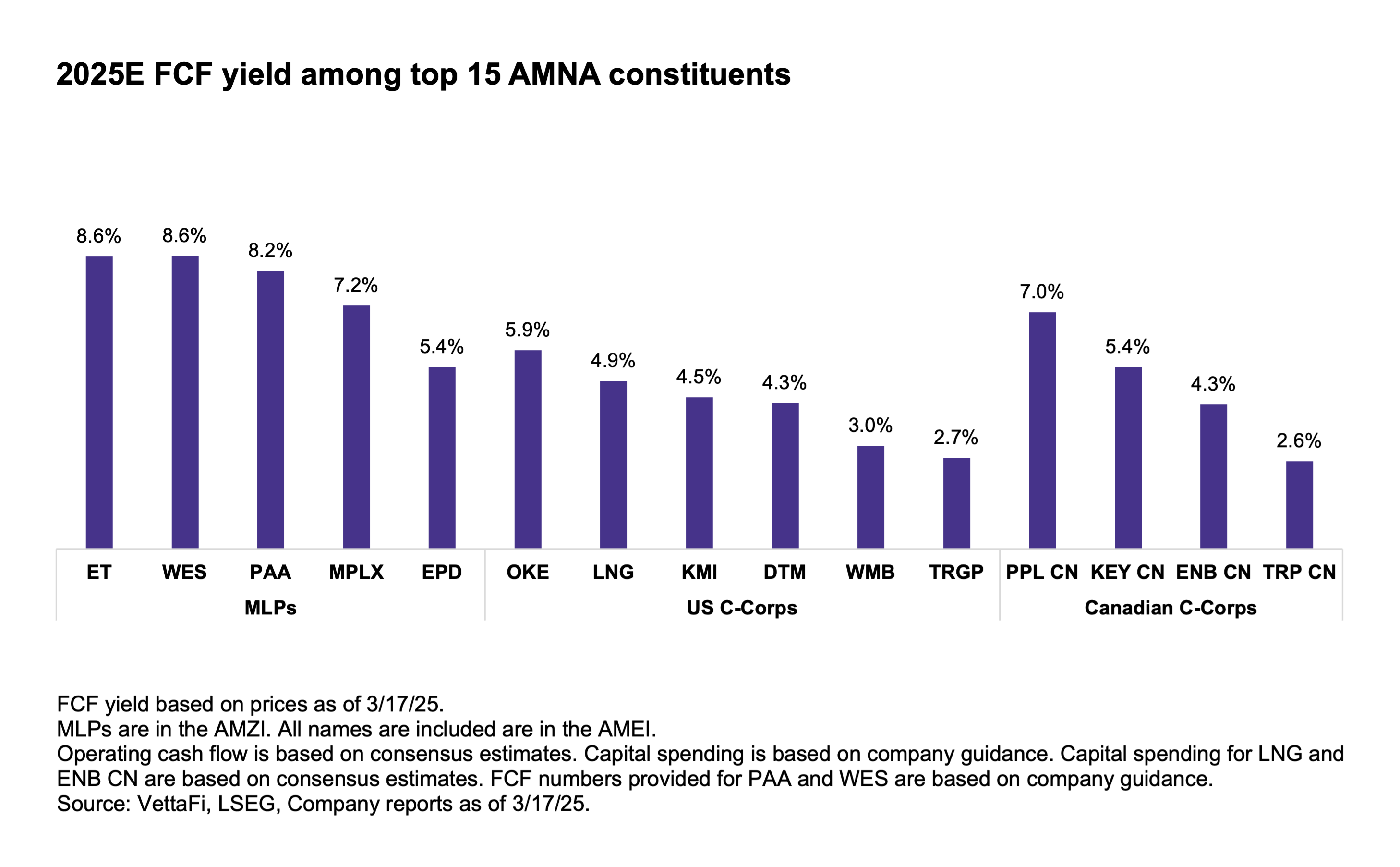

As shown in the chart below, FCF generation remains healthy for energy infrastructure companies, with yields largely in the mid-single digits. By comparison, yields were mostly in the low double digits just a few years ago (read more). However, lower FCF yields correspond to a better valuation. And strong performance for midstream in recent years implies the equities have been rewarded for their FCF and related benefits (dividend growth, buybacks). Keep in mind, since the end of 2021, the broad Alerian Midstream Energy Index (AMNA) is up 74.4% on a price-return basis as of March 17, 2025.

The chart below shows FCF yields for the top 15 constituents in AMNA by weighting as of March 17. All of the names included are also in the Alerian Midstream Energy Select Index (AMEI). The MLPs are in the the Alerian MLP Infrastructure Index (AMZI). FCF yields were calculated using consensus estimates and company guidance for 2025.

Despite Capex Creep, FCF Yields Remain Healthy

Although capital spending is increasing for some companies, large midstream names in the chart are still expected to generate solid FCF. For example, Energy Transfer (ET) is expecting $6.1 billion in growth and maintenance capital spending in 2025. That's up from $4.6 billion spent last year. Even with the notable increase in spending, ET has the highest FCF yield in the chart, along with Western Midstream (WES).

As another example, Kinder Morgan (KMI) has announced three large gas projects since July, representing $5 billion in costs for the company. KMI is expecting a $0.5 billion or 19% increase in capex in 2025 compared to 2024 but still has a solid FCF yield. Of note, KMI acquired Bakken gathering and processing assets for $640 million earlier this year/ That is not incorporated in the year-over-year capex comparison or in the chart above.

From a capital allocation standpoint, growing dividends and reinvesting in the business tend to take top billing. Often, midstream companies will grow their dividends in line with EBITDA or cash flows (read more). Broad dividend growth is expected to continue. Companies may also pursue attractive acquisitions with asset-level deals quite common.

Some companies are expected to have ample FCF after dividends, easing the path for future buybacks. Others will likely prioritize growth capital over buybacks in the current environment. Strong performance in recent years may also dampen buyback activity for names that take a more opportunistic approach. Only eight names in AMNA did buybacks in 2024. And 17 constituents have repurchase authorizations (read more). In summary, excess cash after dividends is expected to be deployed strategically with companies pursuing the highest-return uses of capital.

How Does Midstream Compare With Energy & the Broader Market?

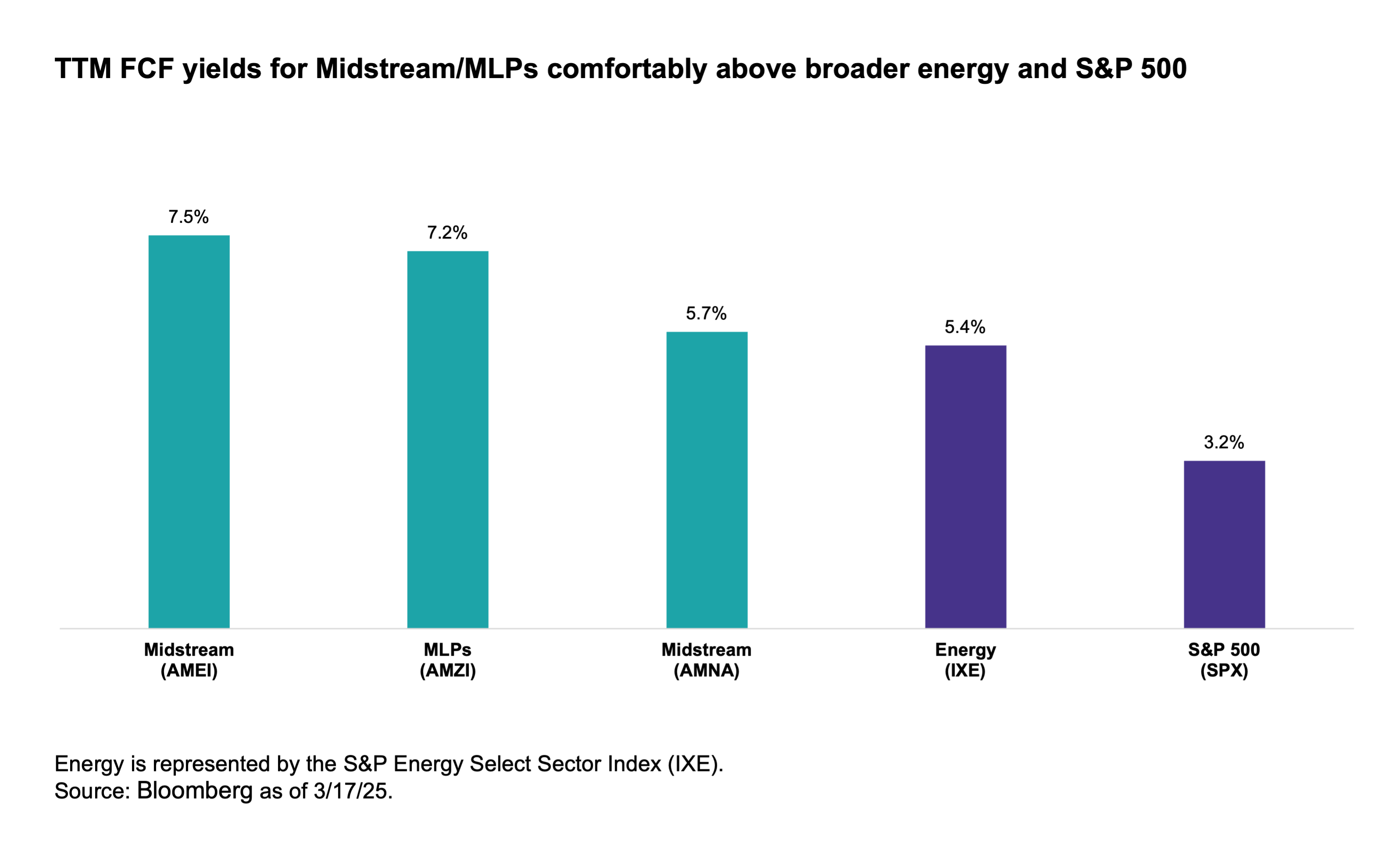

Energy companies broadly are focused on generating FCF, but midstream/MLP’s fee-based business models help generate FCF independent of commodity prices. The chart below shows trailing 12-month FCF yields per Bloomberg. As shown, MLP/midstream FCF yields remain compelling compared to broader energy and the S&P 500. Midstream valuations have improved in recent years. But the space has not become expensive compared to energy or the S&P 500 on a FCF yield basis.

Bottom Line:

Free cash flow generation continues to be an important tailwind for midstream/MLPs. Even with capex increasing as names pursue growth opportunities around natural gas and NGLs in particular, FCF is expected to remain positive. Midstream/MLP FCF yields remain attractive compared to other relevant equity benchmarks.

For more news information and analysis, visit the Energy Infrastructure Channel.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMZ is the underlying index for the JPMCFC Alerian MLP Index ETN (AMJB), the ETRACS Alerian MLP Index ETN Series B (AMUB), and the ETRACS Quarterly Pay 1.5x Leveraged Alerian MLP Index ETN (MLPR). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, AMJB, AMUB, MLPR, AMNA, ENFR, and ALEFX, for which it receives an index licensing fee. However, AMLP, MLPB, AMJB, AMUB, MLPR, AMNA, ENFR, and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, AMJB, AMUB, MLPR, AMNA, ENFR, and ALEFX.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by VettaFi