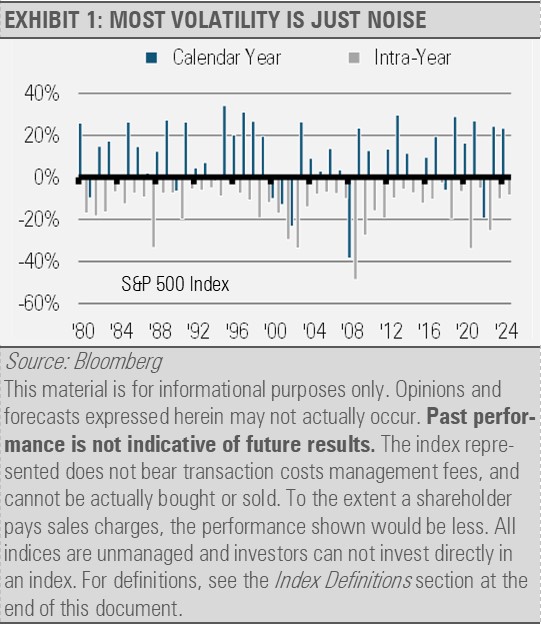

Volatility and Corrections are Part of Equity Investing

The equity market tends to see a correction every 18 months or so. Most corrections are recovered in a short period of time (exhibit 1). Bear markets are rarer and are usually associated with a recession. If it is not a recession-induced bear market, it is probably a buying opportunity.

The Economic Impact of Tariffs on the U.S. Economy

Tariffs are taxes imposed on imported goods, typically as a percentage of a product's value. These taxes are paid by the companies that bring foreign goods into the country and can be passed on to consumers in the form of higher prices. While tariffs are often touted as a tool to protect domestic industries or generate government revenue, they tend to increase costs, slow economic growth, and distort the functioning of international markets.

However, the impact of tariffs on the U.S. economy is somewhat mitigated by our relative economic insularity as a global economic powerhouse, and our unique trade relationships. Despite this, the effects of tariffs can still reverberate across industries, particularly affecting lower-income consumers and certain sectors like automobile production.

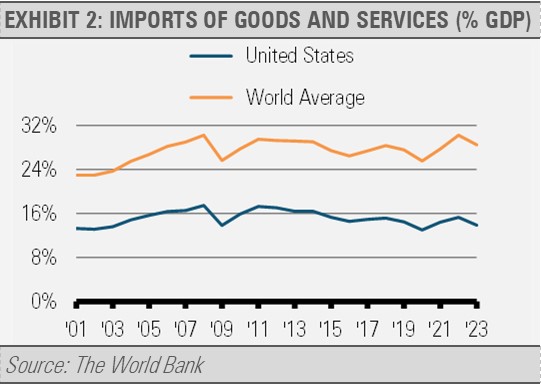

Limited Impact on the U.S. Economy

Unlike many smaller, more trade-dependent nations, the U.S. is relatively insulated from the direct effects of tariffs. As of 2023, imports of goods and services accounted for less than 14% of GDP, compared to over 28% for the global average (exhibit 2). This makes the U.S. less vulnerable to trade disruptions and tariff-related distortions than many other economies, which are more reliant on exports and imports to fuel their growth. In this context, while tariffs can still cause economic disruptions, their impact on the U.S. economy is likely to be more limited than in other countries.

Despite this relative insularity, tariffs still pose a challenge for the U.S. economy. The burden of tariffs falls on businesses that import foreign goods, and these companies often pass the increased costs to consumers. This typically leads to higher prices, which reduces disposable income and slows consumption. For low-income earners that often spend a larger percentage of their income on goods, the effect is even more pronounced. Many of these consumers are already struggling with inflation, and additional price hikes from tariffs could exacerbate their difficulties. Thus, while tariffs may not trigger a recession, they are likely to cause a slowdown in economic activity.

The Automobile Industry and Other Sectors

At the industry level, some sectors are more vulnerable to the effects of tariffs than others. The automobile industry, for example, stands to be significantly impacted by tariffs on imported parts and finished vehicles.

The U.S. automobile industry relies on a complex global supply chain, with many components, such as electronics, tires, and steel, sourced from other countries while some domestic brands perform final assembly in Canada and Mexico. Tariffs on these imports would raise production costs, potentially driving up the prices of vehicles and reducing demand.

The effects of tariffs, however, are likely to be more pronounced at the microeconomic level, rather than at the macroeconomic level. This means that while tariffs may slow overall economic growth, the most significant effects will be felt in industries with high levels of foreign input and by specific groups of consumers.

For example, consumers in higher-income brackets, who are less reliant on price-sensitive goods, may be less affected by the rise in costs compared to low-income households. Similarly, businesses in industries that rely heavily on imports will experience greater disruption than those with more domestic production.

Tariffs and Economic Growth

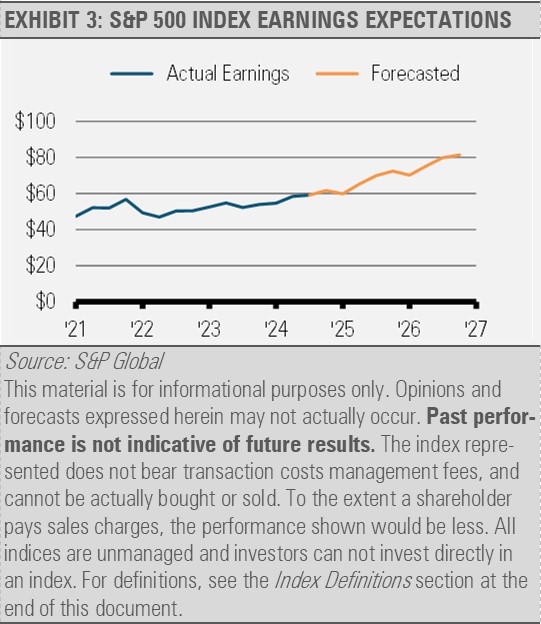

Despite the challenges posed by tariffs, analysts generally expect continued earnings growth for large-cap U.S. companies. The S&P 500 Index, for instance, is forecasted to see persistent earnings growth in the coming years, driven by the expansion of the broader U.S. economy. While tariffs and geopolitical tensions may slow this growth, they are unlikely to derail it entirely. In fact, analysts predict that large-cap companies will continue to grow earnings, albeit at a slower pace than in previous years (exhibit 3).

Jobs Creation Stabilizing

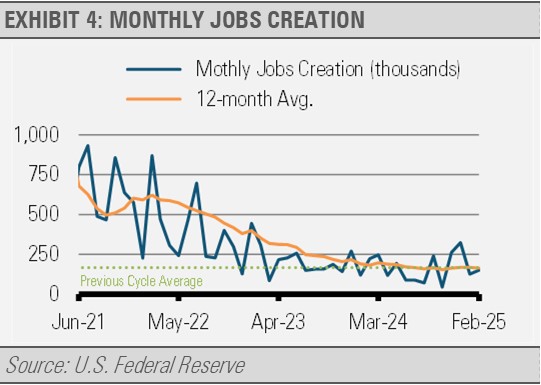

With 151,000 new jobs created, the February jobs gains slowed to 11,000 less than the 12-month average. This was mainly due to the reduction of 10,000 jobs in the federal government. The private sector continues to create new jobs at a steady pace. Now that the U.S. is close to full employment, we are unlikely to get major swings in the monthly jobs report like we saw earlier in the post-pandemic recovery. Steady jobs gains reflect a private sector that is healthy, stable, and growing.

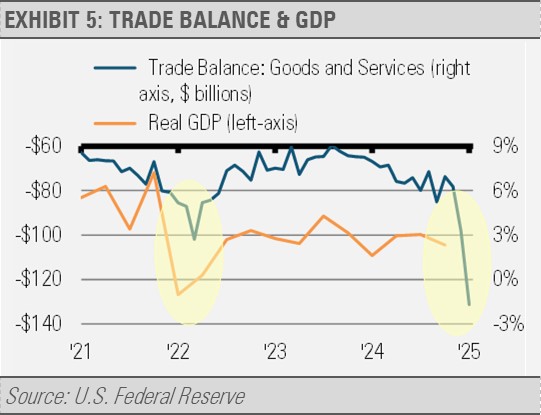

However, recent data suggests that the U.S. economy could experience a slowdown in the short term largely due to a slowdown in key economic indicators, such as personal consumption expenditures and private fixed investment. In addition, we could see a negative GDP print in the first quarter, though we would not consider this a recessionary risk. Rather, similar to what we saw in early 2022, imports in the U.S. have spiked recently (exhibit4). In 2022 the increase in imports was the result of supply chain bottlenecks easing. Imports spiked this year as businesses frontload inventories ahead of expected tariff increases.

Because imports subtract from the GDP calculation, this sharp increase in imports could result in negative GDP growth for the quarter. However, these effects will likely be reversed in future quarters resulting in a higher GDP figure at that time.

Looking Beyond GDP

While negative GDP growth may occur in the short term due to increased imports, it is important to focus on other indicators to gauge the health of the economy. For example, Real Final Sales to Domestic Purchasers (a measure of domestic demand that excludes the impact of net trade) offers a clearer picture of the underlying strength of the U.S. economy. By focusing on this measure, we can better assess the true economic conditions, ignoring temporary fluctuations caused by tariff-driven import spikes. Additionally, other data points, such as the manufacturing Purchasing Managers' Index (PMI), indicate that the U.S. economy remains resilient despite the short-term disruptions caused by tariffs and trade tensions.

INVESTMENT IMPLICATIONS

Our Strategies remain overweight the U.S. with a focus on quality businesses with consistent earnings and low financial leverage. The foreign businesses we favor have similar characteristics. »We have been advocating for some time in favor of the quality equity factor. The recent market action has illustrated how quickly rotations can occur and the quality factor protected nicely. We expect the rotation away from the Magnificent 7 to continue and for quality investments to benefit. On the fixed income side, we are focused on high quality intermediate duration corporate bonds and asset-backed securities.

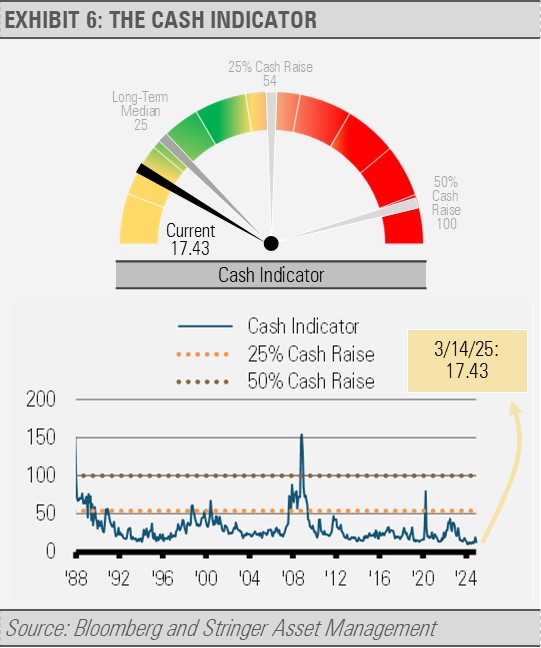

THE CASH INDICATOR

The current Cash Indicator (CI) level is not suggesting a severe market dislocation that would prompt significant cash raise. The CI is well below the 54 level that would suggest a significant increase in cash. Fear in the domestic equity market has been inching up from very low levels. We view this trend as a healthy development and a recent from last year’s complacency. Markets that are overly complacent are more easily subject to downside shocks. With the current positive economic backdrop, equity market declines are buying opportunities in our opinion.

For more news, information, and strategy, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

Index Definitions:

S&P 500 Index – This Index is a capitalization-weighted index of 500 stocks. The Index is designed to measure performance of a broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

A message from Advisor Perspectives and VettaFi: Exchange starts March 23. Register today and invest in your greatest asset – yourself!

Read more commentaries by Stringer Asset Management