The decision to drill for oil is not primarily driven by government mandates or regulatory pressure, but rather by market forces. Oil companies determine their drilling plans based on the economics of production, with a particular focus on the price of oil. According to a survey by the U.S. Federal Reserve Bank of Kansas City, the average cost of oil production is around $62 per barrel. Oil executives have indicated that they would be eager to increase production if oil prices rise to $84 per barrel. This market-driven approach underscores the limited influence of government in directly affecting the level of oil production. Unless production costs fall significantly or oil prices rise dramatically, it is unlikely that we will see a substantial increase in output, regardless of new government regulations or lease approvals.

In fact, it is not even clear that opening up more federal lands for drilling would significantly boost oil production. There are already thousands of unused drilling permits on federal lands, making it unlikely that additional leasing would lead to more drilling activity. The private sector has repeatedly demonstrated that it is capable of responding to market signals without the need for government intervention.

The Role of the Private Sector in U.S. Energy Production: A Marginal Government Influence

There is a common misconception that government policies and regulations have a significant impact on the production of oil and natural gas. While government actions, such as executive orders and regulations, do affect certain aspects of the industry, the private sector’s influence remains far more substantial in shaping the U.S. energy landscape. This is particularly evident in the production of oil, where the majority of extraction occurs on private lands, largely outside the purview of federal influence. The story of U.S. energy production is a testament to the power of market forces and the innovative capacity of private enterprises, with government involvement playing only a marginal role.

The Private Sector's Dominance in Oil Production

Despite frequent political rhetoric about the need for more government-led energy initiatives, the private sector is the real driving force behind U.S. oil production. Approximately 75% of U.S. oil production occurs on private lands. In contrast, only about 11% of U.S. oil production takes place on federal lands. When accounting for offshore drilling, federal areas contribute only about 25% of total oil production in the United States. This stark contrast highlights the primary role of private businesses in shaping the country's energy output.

Federal lands, managed by agencies, such as the Bureau of Land Management (BLM), do contribute significantly to the energy mix, with oil and gas production from federal mineral estates accounting for about 11% of the nation's oil and 9% of its natural gas. However, this is still a small fraction of the overall production. Furthermore, data from the BLM reveals that thousands of drilling permits for federal lands remain unutilized, with 6,903 approved permits sitting idle as of 2024. This raises an important question: if the government’s role in energy production was truly decisive, why are so many federal drilling permits not being used?

The Impact of Innovation and Technology

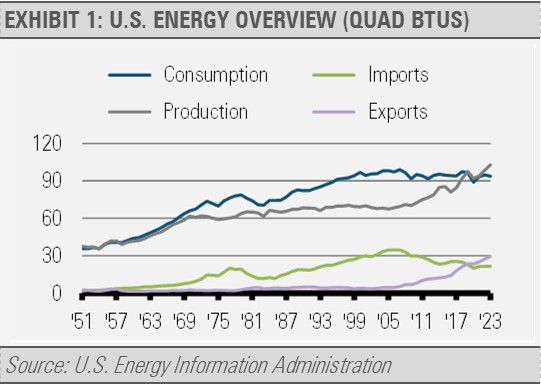

One of the key reasons for the U.S.'s increasing energy production, particularly in oil and natural gas, has been the application of innovative technologies. The shale revolution, which began in earnest in the late 2000s, was driven not by government mandates, but by technological breakthroughs in hydraulic fracturing and horizontal drilling. These advancements allowed energy companies to unlock vast reserves of oil and natural gas from previously inaccessible shale formations. As a result, U.S. oil and gas production has skyrocketed, with production increasing by 70% for natural gas and 112% for crude oil between 2010 and 2022.

This surge in production has not been a result of federal policy, but rather of market-driven innovation. The energy sector's ability to adapt to changing market conditions and technological advancements has been the primary factor in the U.S.'s transformation into a net exporter of oil and natural gas. While government policies can create certain regulatory frameworks, they have not been the catalyst for this remarkable transformation.

Energy Prices and Government Policy

It is also important to note that government policies have a limited impact on energy prices. While politicians may argue that increasing drilling on federal lands will lower oil and gas prices, the reality is more complicated. Lower prices typically discourage drilling, as oil companies are unlikely to invest in new production if the return on investment is not profitable. This cyclical boom-and-bust nature of the oil industry is a well-established feature of the market, not something easily controlled by government policy.

To lower energy prices in the long term, two things would likely need to happen: a significant drop in demand or a substantial decrease in production costs. A reduction in demand would most likely occur in the context of a broader economic downturn, such as a recession, or in response to technological shifts that reduce reliance on fossil fuels. A decrease in production costs would likely come from further technological advancements, not government intervention.

Conclusion

The U.S. energy sector is a striking example of how the private sector, rather than the government, drives economic growth and innovation. While the federal government has a role in regulating certain aspects of the industry, its impact on overall production levels is minimal compared to the influence of market dynamics and private enterprises. The significant increase in U.S. oil and gas production over the past decade is a testament to the power of innovation and market forces, with government policies playing a marginal role at best. As long as the private sector continues to lead the way in technological advancement and responsive production, the U.S. will remain a dominant force in the global energy market, regardless of political rhetoric or regulatory interventions.

For more news, information, and strategy, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by Stringer Asset Management