A lot has happened surrounding tariffs since President Donald Trump took office three weeks ago. While the long-expected increase to tariffs on Chinese goods was applied, the levy was 10%–not the 60% proposed on the campaign trail. President Trump announced 25% tariffs on Columbia which were later rescinded and took similar action with 25% tariffs on Mexico and Canada, only to delay their implementation until early March. In all three of these cases, the tariffs appear to not be about economic policy, but about gaining concessions on illegal immigration and related trafficking issues. The number one surprise in our Top 5 Surprises for 2025 was "tariffs being much higher and then abruptly dropped or sharply reduced." Tariffs being more bark than bite (so far) supports our outlook for both heightened market volatility and our positive outlook for the markets this year. But, while a pattern looks to have been established, the market is far from done with tariff risks in 2025.

Delayed not dropped

President Trump delayed the tariffs for Canada and Mexico from the start of February to the start of March, after initially being planned for Trump's first day in office on January 20. At that time, they will be reevaluated based on the success of planned border enforcement efforts. This echoes the similar threat of 25% tariffs on Mexico made by Trump during his first term, which was dropped 10 days later after Mexico agreed to increase border security.

If the proposed 25% across-the-board tariffs for Canada and Mexico are implemented in March, the high dependence on exports to the U.S. for those two countries is likely to heighten the risk their economies slip into a recession. In fact, with Mexico's GDP negative in the fourth quarter, big U.S. tariffs could tip that country into a second quarter in a row of declines—resulting in a recession.

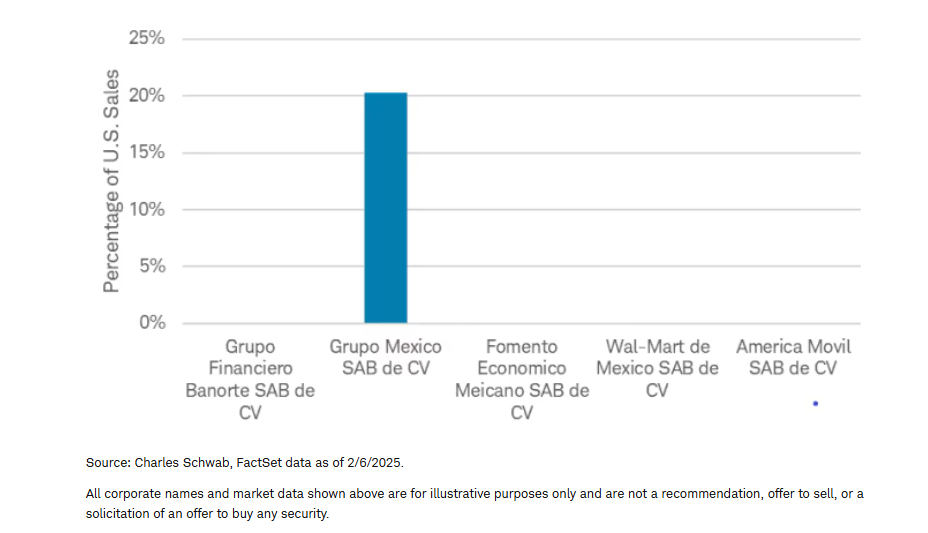

It may seem that the U.S. holds all the cards on negotiations with Canada and Mexico, given their economic dependence on exports to the United States. But the exposure of companies is different and may point to another powerful player in the negotiations: U.S. companies. Based on our analysis, tariffs on U.S. imports from Mexico would likely have a disproportionately negative impact on U.S. businesses, not Mexican ones. Mexico's largest exports to the U.S. are goods produced by U.S. companies operating in Mexico, rather than Mexican companies. Autos are the largest category of Mexico's exports. Mexico's biggest exporters are automotive manufacturers headquartered in the U.S., including Ford and GM. In contrast, a lot of Mexican businesses that have large U.S. sales come from their operations located in the U.S. whose goods would not be subject to tariffs (for example, CEMEX, the big Mexican cement maker). In fact, four of the top five Mexican stocks that make up more than 50% of the MSCI Mexico Index are not likely to be directly affected by the tariffs, because they serve the Mexican market (a bank, a Coca-Cola distributor, a telecom provider, and Wal-Mart). Just the mining company, Grupo Mexico, would be directly affected.

U.S. sales exposure in the top five holdings of the MSCI Mexico Index

This same scenario applies to Canada as well. Outside of energy exports, the largest Canadian exporters to the U. S. are auto makers including Ford, General Motors, Stellantis, Toyota, and Honda—not Canadian companies. The biggest companies in the MSCI Canada Index are banks, not directly impacted by tariffs, and energy companies facing reduced tariff rates.

This may help account for why the Canadian and Mexican stock markets (as measured by their relative MSCI Indexes) continued to outperform the S&P 500 this year, even before the tariffs were delayed.

In lieu of tariffs, the impact of any boycotts may be limited. In Canada, the pulling of U.S. alcohol brands from store shelves in Ontario attracted some attention, but the majority of U.S. imports to Canada are not consumer goods; they are machinery or other capital goods. A Canadian boycott that could be more impactful might be a boycott on U.S. tourism which is, ironically, on the services side of the economy and not subject to tariffs. Surprisingly, Canada is the top source of international visitors to the United States. According to the U.S. Travel Association, Canadians made 20.4 million visits to the U.S. in 2024, generating $20.5 billion in spending. A 10% reduction in Canadian travel could mean two million fewer visits and $2.1 billion in lost spending, as well as contributing to some job losses. The overall impact isn't likely big enough to move GDP numbers, but it could matter for some tourism-focused industries.

Opening salvo

An announced 10% increase in China tariffs did go into effect on February 1st, as widely expected. China's limited retaliation seems aimed at avoiding escalation. This may be because China is more focused on domestic economic concerns rather than friction on direct trade with the U.S. which makes up only 3% of its GDP, based on China's reported exports to the U.S. Yet, Trump referred to the 10% tariff announcement as an "opening salvo." Note that executive orders on President Trump's Day One included a directive to review the existing China 301 investigation as well as the 2020 Phase One deal by April 1, signaling further U.S. actions may follow. China may respond with offers to purchase U.S. goods or concessions on geopolitical issues such as Russia-Ukraine in the negotiations that may follow.

Import and export data reveal that exporters based in China appear to be getting around the Trump 1.0 China tariffs by exporting to Cambodia, Vietnam, Thailand, or others to then deliver products to the U.S. since the tariffs went into effect in 2018. This rerouting avoids the impact of the tariffs on economy and markets.

Tall tariffs

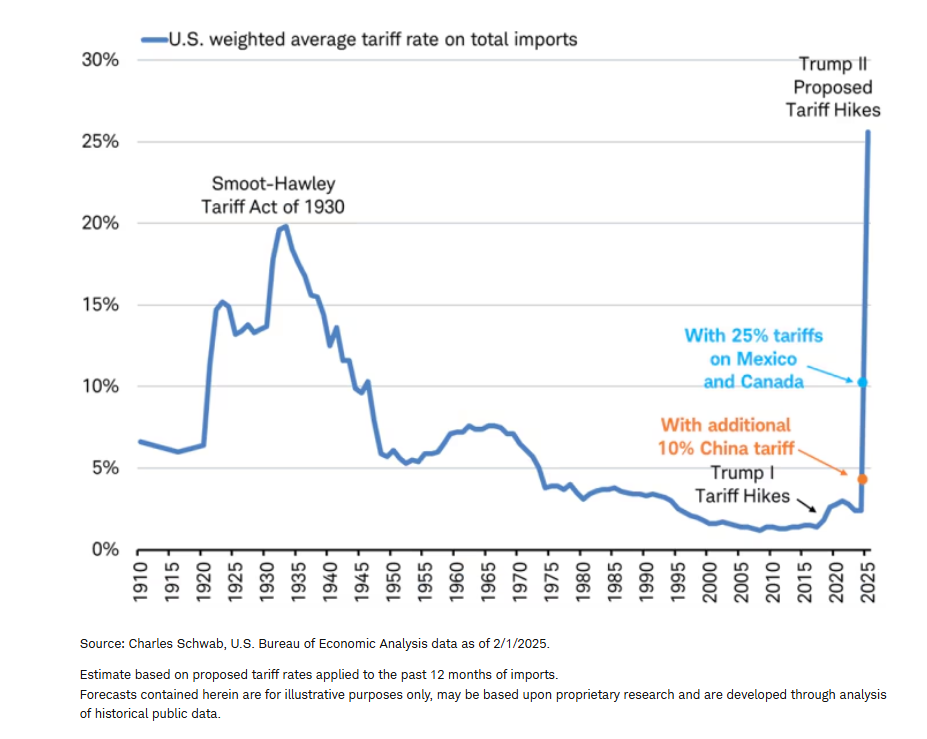

We estimate that the increase in the China tariff rate raises the weighted-average China tariff to 20.6% and raises the U.S. overall all-country weighted-average tariff to 3.6% from 2.6%. If the Mexico and Canada tariffs also went into place, we calculate the tariff rate would rise to 10.5%, based on proposed tariff rates applied to the past 12 months of imports.

Estimated U.S. weighted average tariff rate

More to come

There could be more to come with Trump having threatened across-the-board import tariffs that would apply to all U.S. imports and imposing tariffs on U.S. imports equal to rates that trading partners impose on U.S. exports he has referred to as "reciprocal tariffs." Although the later could potentially move tariffs lower if other countries lower their tariff rates in response to the threat, as India already did in early February on some products and the European Union (EU) reportedly discussed regarding autos.

On Sunday, President Trump said he plans to impose 25% tariffs on all imports of steel and aluminum into the United States. The tariffs would apply to imports of both metals from all countries, including major suppliers in Mexico and Canada. He didn't specify when the duties would take effect. For the European Union (EU), the tariff threat echoes 2018 when Trump applied U.S. imports of European steel and aluminum with tariffs, citing national security concerns, at the time. The two sides agreed to a temporary truce during the Biden administration in 2021, when the U.S. partly removed its measures, substituting an import quota above which duties on the metals are applied.

EU's policymakers have learned that the White House is open to negotiations, which may help avert any potential trade shock and boost the region's growth outlook. To avoid tariffs, the European Union could offer to buy more U.S. energy and defense products, promise to increase Europe's defense spending or threaten tariffs on U.S. services. A coordinated EU response to any new tariffs may await the outcome of the German election on February 23 since Germany is Europe's biggest economy and is major auto exporter to the United States.

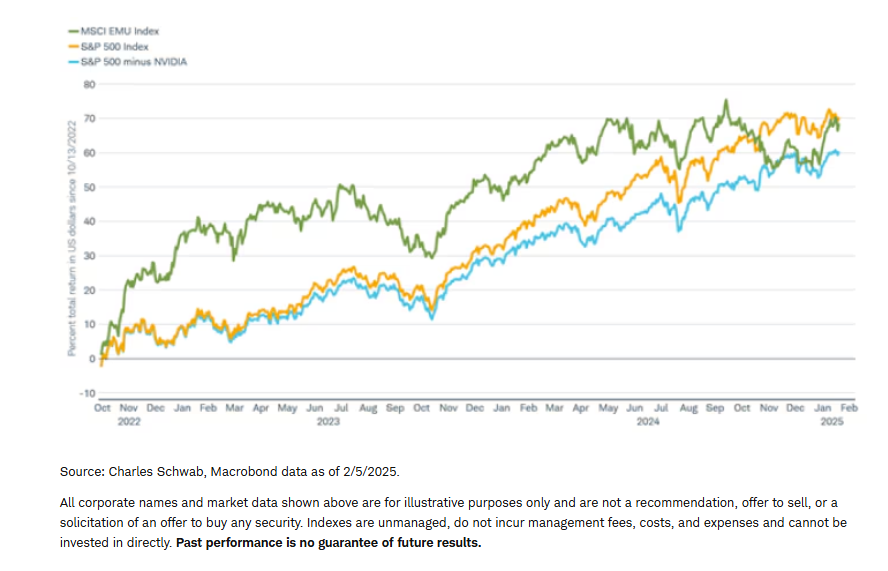

It's worth noting that Europe's stock market, measured by the MSCI EMU Index, has been keeping pace with the U.S. stock market, measured by the S&P 500 since the current bull market began back in October 2022. The total return measured in U.S. dollars for the MSCI EMU Index is about 70% similar to the S&P 500 Index. And, if just one stock (NVIDIA) was removed from the S&P 500, the MSCI EMU Index would be outperforming by a wide margin.

Europe's stock market keeping pace with U.S. stocks since bull market began

The U.K. and Japan have avoided being targeted by tariffs, thus far. When asked by a reporter on February 3 about potential U.K. tariffs, Trump responded "I think that one can be worked out. Prime Minister Starmer has been very nice. We've had a couple of meetings, we've had numerous phone calls, we're getting along very well, and we'll see whether or not we can balance out our budget with the European Union." The U.K. is not a member of the EU and Trump's response suggests the U.K. is further down Trump's list, indicating that they may have an easier solution to avoiding tariffs than other major countries. While Japan's $70 billion trade surplus with the U.S. and the yen's undervaluation could be potential targets, Japan's new prime minister had a friendly meeting with Trump over this past weekend. In part, due to Japan's imports of U.S. energy and Japanese manufacturers' considerable investments in their U.S. operations. Japan is the top source of foreign direct investment in the United States, per the latest data from the Bureau of Economic Analysis.

Safer haven

A tariff delay could still pose problems. Companies may pre-emptively raise prices, lifting inflation (as has already been reported for U.S. steel companies) while holding back on investment given the uncertainty. So how can investors seek a potentially safer haven from tariffs?

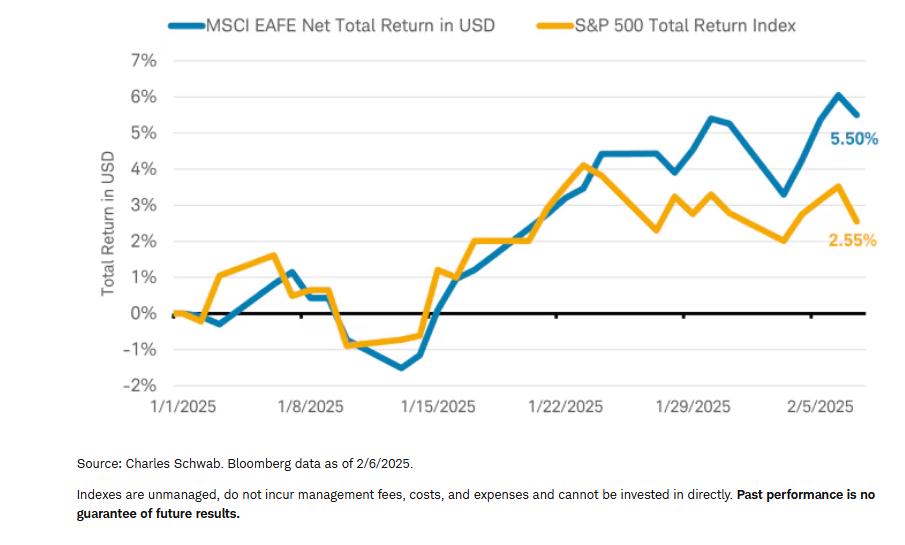

It's possible the MSCI EAFE Index of developed international stocks might offer a relative safe haven from the trade noise, since it doesn't contain any of the first-round combatants in the Trump 2.0 Trade War. EAFE does not include Mexico, Canada, China, or the United States. The biggest country weightings in the index are Japan and the U.K., both countries do not seem to be targets of the Trade War. The MSCI EAFE Index was already outperforming this year, doubling the return of the S&P 500 year-to-date. So those investments that track the EAFE index may be a place for investors to look. From a sector perspective, Financials, the biggest sector in the EAFE index, has been among the leaders this year and is not directly affected by tariffs, and may be another place investors could choose to dodge some of the headline-driven volatility.

International stocks outperforming U.S. stocks so far in 2025

The U.S. dollar (USD) is flat so far this year. While tariffs, if implemented, should push up the USD and weigh on the USD-based returns of international investments. Some tariff impact was likely priced into the USD rally seen last year. This year, both Mexico and Canada's stock markets are outperforming the S&P 500, measured in USD.

What's next

While the stock and currency markets bounced back after the tariffs on imports from Mexico and Canada were delayed, tariff issues are not yet solved and still hold the potential to drive market volatility in the months ahead. But, just as importantly, these events serve as a reminder that we should be cautious about taking announcements at face value, let alone overhauling economic forecasts or investment portfolios in response to them. The MSCI EAFE Index of developed international stocks has the highest weightings in Japan and the United Kingdom while not having any exposure to Canada, Mexico, China, or the United States, offering a potential safer haven for investors seeking less exposure to the combatants in the Trump 2.0 Trade War.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

3384

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Currency trading is speculative, volatile and not suitable for all investors.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI Canada Index is designed to measure the performance of the large and mid-cap segments of the Canada market covering approximately 85% of the free float-adjusted market capitalization in Canada.

The MSCI Mexico Index is designed to measure the performance of the large and mid-cap segments of the Mexican market covering approximately 85% of the free float-adjusted market capitalization in Mexico.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Charles Schwab

Read more commentaries by Charles Schwab