Earnings season is in full swing. This first round right out of the gate may well set the tone for markets in 2025. Overall S&P 500 Q4 earnings are expected to grow 12.5% year-over-year. The bulk of the bottom-line boost is slated to come from financials, communication services, and tech. This would mark the highest EPS growth rate since Q4 2021, per FactSet. It would also mark six-straight quarters of positive annual earnings growth.

So far, the banks have gotten off to a strong start. More companies are beating estimates. And they’re beating by more than usual. But Wall Street will be fixated on next week’s big roster of earnings reports. That includes Tesla, Microsoft, Meta and Apple. Google parent Alphabet, as well as Amazon, and Nvidia – now the world’s most valuable company – follow closely behind in the following weeks.

Profit growth from tech has beaten out much of the S&P over the past three years regarding the earnings equation. Of course, simply using the S&P 500 technology sector is a misleading rule of thumb. By traditional GICs standards, Tesla and Amazon are categorized as consumer discretionary stocks. Meta Platforms, Amazon, and Netflix all fall under the communication services sector. In many ways, the Magnificent Seven has become the poster child proxy for tech instead.

Can Big Tech Keep Up the Growth?

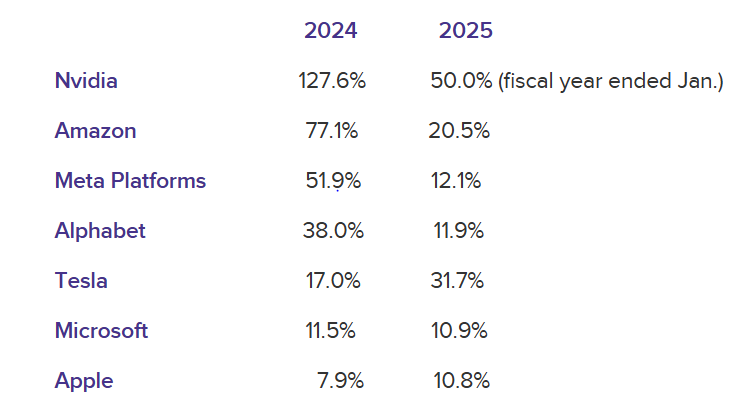

The expectation is for tech earnings growth to be well below where it’s been but still by no means lackluster. Over the past three quarters, the Magnificent Seven put up profit growth north of 35%. But that number is expected to slow to 21.7% for the fourth quarter. According to Christine Short, head of research at Wall Street Horizon, S&P 500 earnings growth for the quarter drops from 12.5% to 9.7% when you strip out those seven companies.

“The bar remains high for the Magnificent 7 this earnings season,” she said. “We’ve seen what happens to big tech stocks when results don’t impress. When names are priced to perfection like some of these mega tech names are, investors are looking for more than perfect quarterly results and future guidance.”

Megacap Tech EPS Growth (Blended)

Source: LSEG/CNBC

Many Facets of Tech ETF Exposure

A vast array of ETFs exist that cater to different segments of the tech industry. The year has barely begun. But so far, the flows have pointed to the most popular tech ETFs. One is the Vanguard Information Technology ETF (VGT), which already has north of $1 billion in net inflows. Then there's a pair of iShares funds. One is the iShares U.S. Technology ETF (IYW) and the other is the iShares Expanded Tech Software Sector ETF (IGV). Both of these funds have netted more than $300 million in net inflows.

Two of the biggest broad-market technology ETFs, the Technology Select Sector SPDR Fund (XLK) and the Invesco QQQ Trust (QQQ), are cap-weighted. They invest in a wide range of tech companies. Each has a heavy tilt toward large-cap stocks like Apple, Microsoft, and Google.

Subsector-specific tech ETFs focus on specific areas within technology. These include semiconductors (VanEck Semiconductor ETF (SMH)), cloud computing (Global X Cloud Computing ETF (CLOU)) and cybersecurity (Amplify Cybersecurity ETF (HACK)). Thematic tech ETFs target specific trends or themes within technology, such as artificial intelligence, robotics, or renewable energy tech. Cathie Wood’s ARK Innovation ETF (ARKK) proved the ultimate barometer of disruptive tech demand back in 2021, when thematic ETFs were all the rage.

Growth Leadership May Broaden Beyond Big Tech

Die-hard Mag Seven bulls may look to the Roundhill Magnificent Seven ETF (MAGS), which offers direct targeted exposure to the big seven. The nearly $2 billion fund has risen 62% over the past year on a NAV basis. Meanwhile, the Vanguard Mega Cap Growth Index Fund ETF (MGK) takes a broader-based approach by providing access to the 69 largest U.S. growth stocks. More than 60% sector representation in tech and Apple, Microsoft, and Nvidia tops the list of holdings.

But for those who believe the Mag Seven story may have run its course, the Defiance Large Cap ex-Mag 7 ETF (XMAG) offers an alternative strategy that allows investors to diversify away from megacap concentration risks.

“The S&P 500 minus Mag 7 goes from a current expectation of sub-10% EPS growth in Q4 to an anticipated increase of nearly 15% in the back half of 2025,” Short said. “Lagging sectors, such as industrials and materials, are expected to pick up in the latter half of the year, partially due to easier year-over-year comps.”

Although earnings growth rates in the technology sector are expected to slow in 2025, they are still projected to outpace the overall market. But growth leadership looks poised to broaden beyond big tech, encompassing other sectors, emerging themes, and smaller tech companies.

Additionally, potential initiatives from the new administration aimed at promoting high-tech and manufacturing industries could lead to a shift in investor sentiment and sector preferences. Such developments may guide investors as they navigate the diverse technology ETF landscape, selecting funds that align with their strategies and goals.

For more news, information, and analysis, visit VettaFi | ETF Trends.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more commentaries by VettaFi