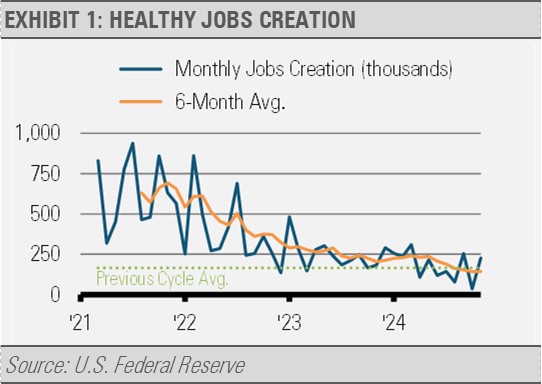

The U.S. economy has demonstrated remarkable resilience despite ongoing challenges. As we look toward 2025, our outlook for the economy and financial markets remains positive, driven primarily by robust private sector activity. Households and businesses, which form the backbone of the U.S. economy, are showing strong signs of growth. Jobs creation is stabilizing at healthy levels with nearly 2 million jobs expected to be created in 2025. Private sector finances are sound, and consumer sentiment is healthy, which contributes to a generally optimistic economic environment.

Given that nearly 70% of U.S. economic activity is consumer-driven, nothing is more fundamental to the current health of the economy than jobs creation and income growth. As evidenced below, jobs creation is stabilizing at a level consistent with the previous business cycle and we think will create nearly 2 million new jobs in 2025.

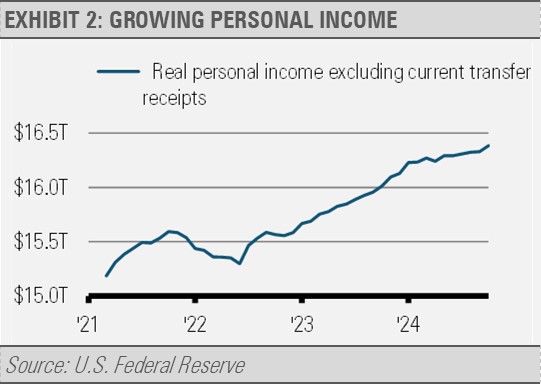

Meanwhile, real personal income is at an all-time high. We measure real personal income excluding transfer receipts because it adjusts for inflation and excludes payments, such as Social Security, Medicare and Medicaid, Unemployment Assistance, and a wide range of other benefits. As the following graph shows, personal income, even after adjusting for inflation and government support, is at an all-time high, which bodes well for consumption going forward.

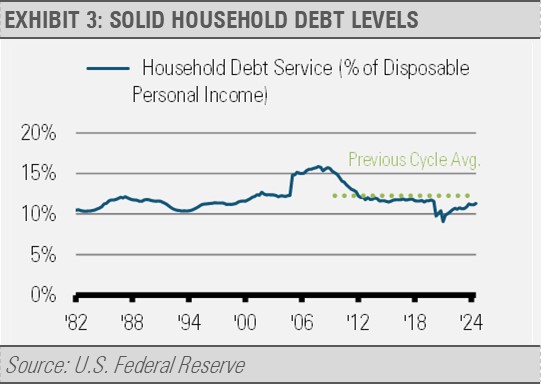

Similarly, overall private sector debt, including households and businesses, has declined relative to the size of the economy (GDP) to levels consistent with historical norms after fully recovering from the pandemic. Looking at household debt-to-disposable income, the situation has normalized following the unprecedented economic disruptions of the COVID-19 pandemic. The current household debt-to-income level is at a rate similar to the long-term average and well below levels that we saw during the mid-2000s housing boom. This situation represents a fundamental improvement in economic resilience and provides businesses and consumers with greater financial flexibility.

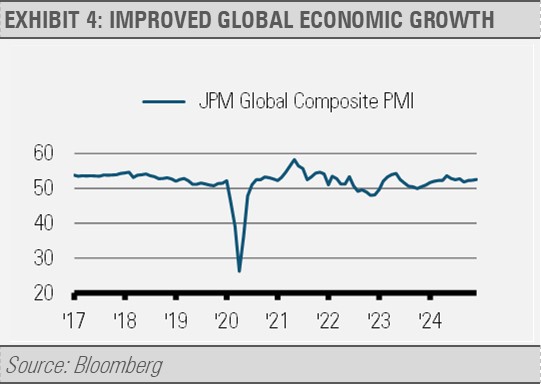

Global economic expansion improved in late 2024 as the rate of growth reached a four-month high according to the JPMorgan Global Composite PMI. The U.S. was one of the strongest performers with robust growth in services, although manufacturing has faced headwinds.

The global economy remains uneven, with regions like India experiencing solid growth, while the Eurozone and Canada experienced contractions. Despite a mixed picture in the U.S. with the service sector advancing while the manufacturing sector struggled, business expectations for the coming year are high.

Amid the backdrop of persistent inflation and healthy economic growth, the U.S. Federal Reserve has indicated that interest rate cuts in 2025 will likely be more moderate than previously anticipated. As a result, we expect higher interest rates to persist for a longer period, especially given the ongoing fiscal deficits. Short-term interest rates at the end of 2025 are now expected to range between 3.75% and 4.00%, with long-term rate expectations also adjusted higher.

While inflation pressures persist, there are structural factors that support continued U.S. economic strength. Geopolitical fragmentation, the rapid growth of artificial intelligence (AI), and other innovations across industries, as well as the broader buildout of U.S. industrial capacity, are driving economic shifts that may elevate costs in the short-term but have long-term growth potential. Additionally, the U.S. is well positioned to benefit from these trends, especially as corporate earnings continue to expand. These developments go beyond the AI boom and highlight the resilience of U.S. businesses despite higher interest rates. Overall, our work suggests a constructive backdrop for the U.S. and strong relative economic strength compared to most foreign markets. Geopolitical risks remain a concern and will likely lead to greater market volatility, which supports our risk first approach.

INVESTMENT IMPLICATIONS

We encourage investors to pay particularly close attention to risk tolerance, appropriate asset allocation, and rebalancing. The recent run of a handful of companies creating unprecedented equity market concentration can develop significant risks resulting from portfolio dislocations. Equity market rotations can happen quickly, and it is important to be prepared for these potential shifts, especially in light of today’s equity market concentration.

Despite some concerns about valuation levels in the equity market, there are strong reasons for optimism. While S&P 500 Index valuations look expensive relative to historical norms, we note that equity market valuations have little impact on near-term forward returns. Equity market valuations are much more relevant over the coming 5-year and 10-year time horizons but are negligible in the short term.

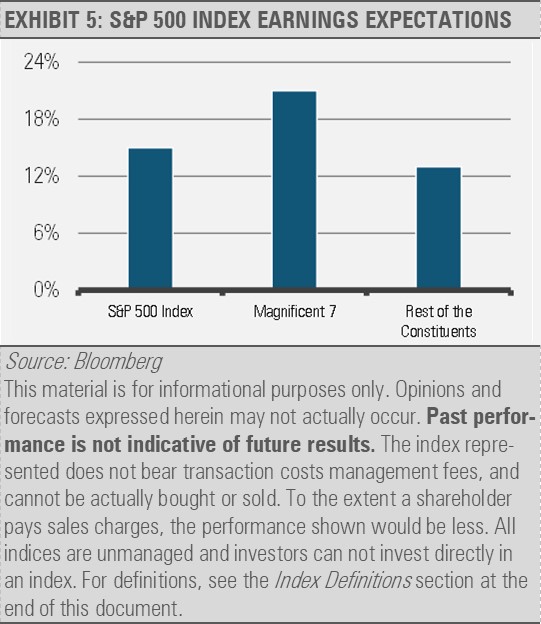

Furthermore, the nature of today’s concentrated equity market leaves many opportunities to be captured as earnings growth and market participation expands beyond the Magnificent 7. Analysts expect 15% earnings growth for S&P 500 Index’s companies according to FactSet. This includes expectations for 13% earnings growth for the other companies that are not the Magnificent 7.

In our view, while the S&P 500 Index might not be able to match its strong 2024 performance this year, the ability for investors to find attractive opportunities has broadened significantly.

We are focused on areas where we find quality businesses with consistent earnings growth and low financial leverage. This plays out in our tactical overweight to the U.S. relative to foreign equity markets and specific sectors, such as information technology, financial services, consumer discretionary, and communications services. Tactical allocations can provide a chance for investors to rebalance and diversify across the broadening array of opportunities to capture returns while managing risk.

In addition to the growth in U.S. equities, there are also investment opportunities in certain blue-chip companies with global businesses that happen to be headquartered overseas. Dividend paying global businesses, especially in the health care sector, offer particularly attractive investment opportunities in our view. Countries like India stand to benefit from long-term trends, such as the U.S. and China competition and the global push toward innovation. However, we are more cautious on markets like China due to ongoing trade uncertainties, a massive debt burden, and negative demographic trends despite fiscal support.

Regarding our fixed income allocations, we remain overweight asset-backed securities, mortgage-backed securities, and corporate bonds in the belly or intermediate part of the yield curve. Here, we are finding opportunities to harvest attractive current income while maintaining less interest rate risk than the broader bond market. We expect continued interest rate volatility in the months ahead as shifting inflationary trends combine with persistent federal deficits to add to uncertainty. Our more active duration management and diversification across our models may help capture yield and take advantage of changes in interest rates in the year ahead. Our fixed income management continues to be a valuable differentiator for us as it was last year.

Looking ahead to 2025, the outlook for the U.S. economy and financial markets remains strong, but there are risks to consider. Inflation is likely to remain above target and lead to higher interest rates for a longer period than previously expected. However, structural shifts in the economy, particularly the growth of AI and the broader industrial buildout, offer substantial opportunities.

Corporate earnings are expected to continue growing from innovation and the U.S. equity market remains a strong investment. At the same time, there are attractive opportunities in investment grade core fixed income. As always, staying nimble and adjusting investments based on evolving conditions will be key to navigating the year ahead.

THE CASH INDICATOR

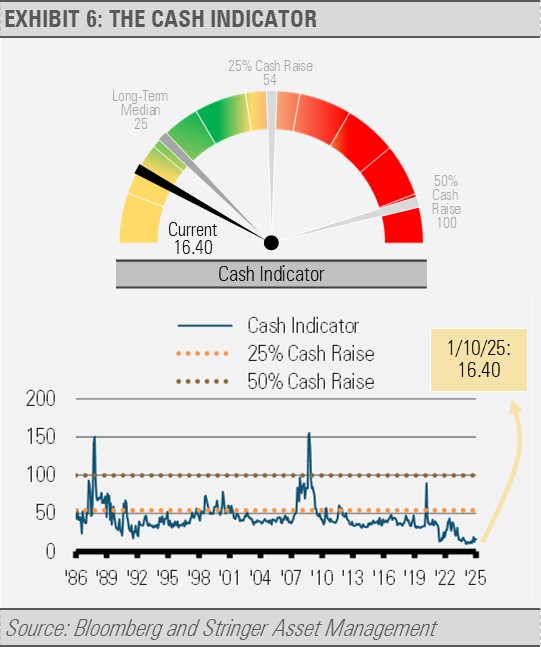

The Cash Indicator (CI) remains well below historical norms as equity market volatility has been limited and fixed income credit spreads remain tight. Given the shifting interest rate environment and geopolitical risks, there are many factors that could tip the equity market into a period of heightened volatility. With our positive economic backdrop, we think periods of increased volatility are likely buying opportunities for disciplined investors.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

Index Definitions:

S&P 500 Index – This Index is a capitalization-weighted index of 500 stocks. The Index is designed to measure performance of a broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

For more news, information, and analysis, visit the ETF Strategist Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

More Active Fixed Income Topics >