China's stock market has suffered since the U.S. election, dragging down the MSCI Emerging Market Index where it makes up the biggest country weighting at 28% of the index. Tencent Holdings Ltd became the latest reason for the declines after becoming a political causality; the stock fell 10% after being added to the U.S. Department of Defense blacklist last week.

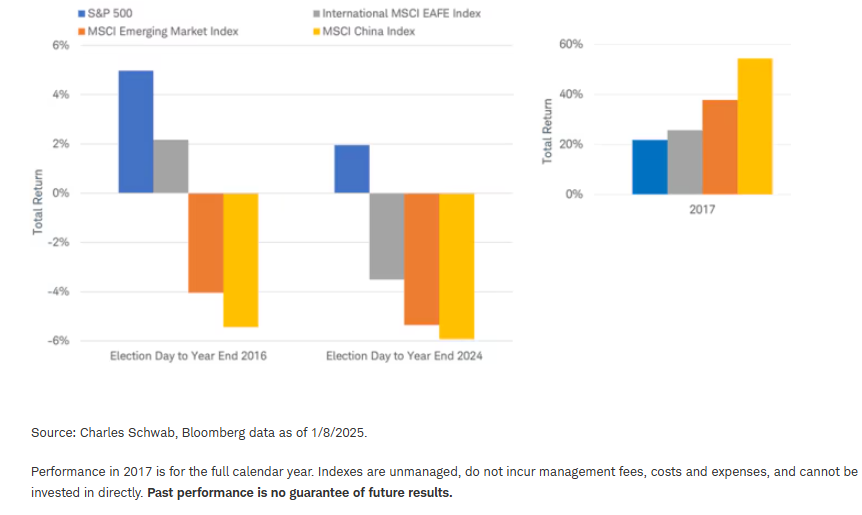

Since U.S. Election Day, the market has seemed to interpret President-elect Trump's "America First" policies as good for U.S. stocks and bad news for emerging-market stocks. This market behavior mirrors performance seen right after Trump's win in 2016, when U.S. stocks led the gains and emerging markets, including China, suffered the most. However, that trend quickly changed. During the first year of Trump's term in 2017, emerging-market stocks were the best performers—with China leading the way with a total return of 56% as measured by the MSCI China Index, followed by developed international stocks, then U.S. stocks.

Reversal of fortune

Could 2025 see China and emerging-market stocks follow the path of 2017's powerful gains? With Chinese stocks' valuations starting this year at a below average level that is similar to the beginning of 2017 (as measured by price to next-12-months earnings estimates), let's assess how the year is shaping up to gauge the potential for a rally.

Chinese stocks are off to a weak start to 2025, down 4% through the end of last week, as measured by the MSCI China Index. But this is not uncommon. Chinese stocks are notoriously volatile at the start of the year—the result of a lack of any news, not necessarily bad news. Market participants tend to dislike uncertainty more than anything else. China's economic data is often combined for January and February and not released until March. The week-long Lunar New Year holiday often sees a surge in manufacturing, industrial and export activity in advance of the national production shutdown, bringing a sharp rise in consumer spending and tourism that subsequently falls between late January and early February. This results in crucial monthly statistics being delayed by a month and subject to wide swings. To add complexity, the lunar holiday shifts slightly each year making year-over-year comparisons difficult. Also, the decisions made at December's Central Economic Work Conference, covering matters like China's annual growth target and government budget, are not typically followed by details on how those goals are to be achieved until the annual meeting of the National People's Congress in early March. The vacuum of data and details on stimulus plans and overall government spending initiatives means stocks tend to jump around on hints and signals, at least until more clarity comes in mid-March.

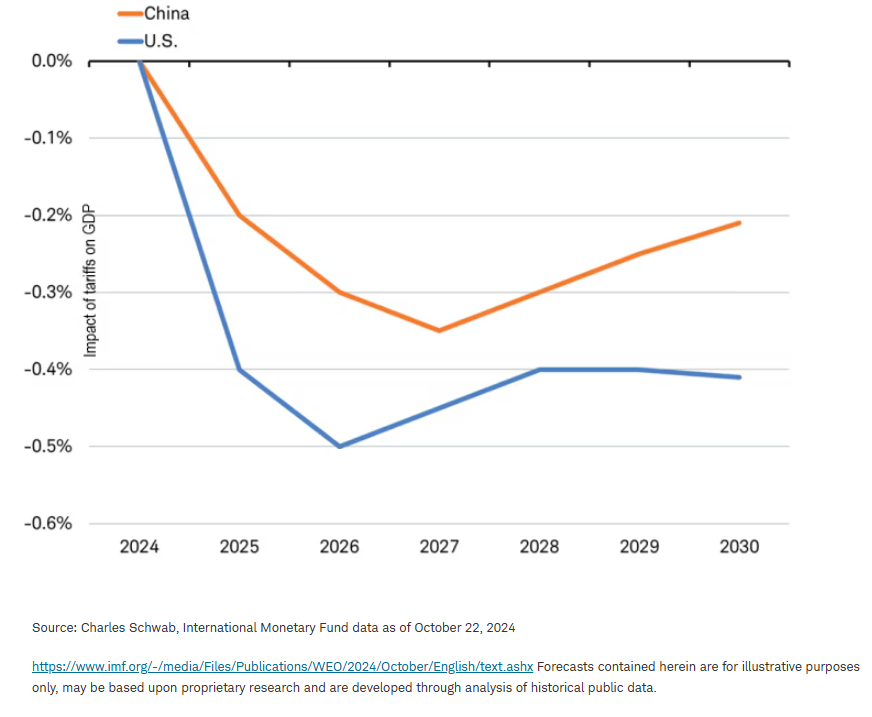

Many investors may have already concluded China is in for a tough year after the incoming Trump administration pledged significantly higher tariffs on imports from China. At this time, we have yet to see any details on what those tariffs may entail. It's important for investors to know that trade with the U.S. may not be a critical driver for China's economy. U.S. imports directly from China generate less than 3% of China's GDP (according to both Chinese and U.S. trade data) and unlikely to go to zero under any realistic scenario. The sharp rise in tariffs during the first Trump administration didn't reduce U.S. imports from China; overall imports directly from China remain near the pre-trade-war level and there appears to have been a rise in indirect imports from China through other countries such as Vietnam, Cambodia, and Thailand. Assuming China's currency depreciates along with a further shift of Chinese exports to the U.S. through other countries, the impact of additional tariffs could be negligible. Supporting this view, the forecast of the International Monetary Fund in their latest World Economic Outlook was for the potential of a -0.2% hit to China's GDP in 2025 from a trade war that includes not only the U.S. and China imposing new, reciprocal across-the-board tariffs on each other, but between Europe and China, as well.

IMF trade war scenario forecast impact on GDP level

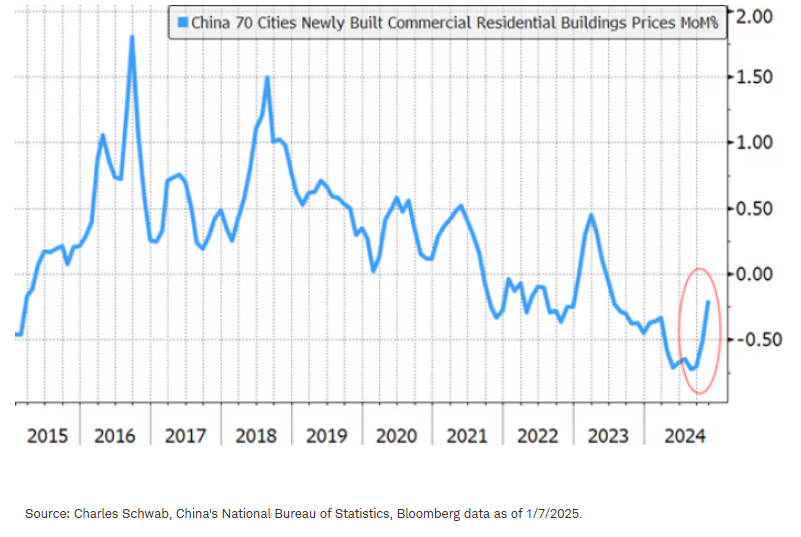

Instead of focusing on external developments, we believe the domestic economy is more critical for China's outlook in 2025. Specifically, whether the housing market is in the early stages of stabilization.

Signs of housing stability beginning in China

The data appears to signal some tentative improvement:

- Home prices appear to be seeing some signs of stabilization for the first time in a year and a half. Although prices are still falling, the pace of decline had eased in the fourth quarter, slowing from -0.7% in September to just -0.2% in December.

- Economic activity improved with the Purchasing Managers' Index (PMI) surveys for December showed solid improvement in the composite index driven by the service sector. Given that services supply most of the jobs, this may be good news for the labor market.

Government stimulus is critical to the outlook. In 2024, the Chinese government repeatedly overpromised and underdelivered in this regard. December's Politburo meeting changed the monetary policy stance for the first time since the Global Financial Crisis of 2008-09 to "moderately loose" from "prudent." In the same month, the Central Economic Work Conference moved up prioritizing domestic demand from second place last year to top the list of tasks for 2025, using strong language such as "vigorously promoting consumption" and pledging to implement "landmark reforms." But still, there were no details. There is the potential for a big stimulus program with enough details that may brighten the markets' outlook for stabilization in housing and improvement in consumer confidence in 2025. But few details or too narrow of a scope for the program could disappoint investors.

Overall, despite the trade-war headlines, the stage may be set for a rally in Chinese stocks—and emerging-market stocks by extension—in 2025 that might echo the gains seen during the first year of Trump's term in 2017. Yet, it is also possible that policy support will prove insufficient to sustain any improvement in housing, boost household confidence, and offset U.S. tariffs and other restrictions. Investors might be in for a wild ride in Chinese stocks in the first quarter before the data and policy announcements of mid-March set a clearer path for 2025.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Charles Schwab

Read more commentaries by Charles Schwab