Navigating High-Yield Bonds: Opportunities, Risks and Fallen Angels

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- High-yield bonds have delivered strong returns in recent years with less volatility than equities, providing an attractive risk/reward balance for investors.

- Despite tighter credit spreads, we maintain a constructive outlook for higher-quality high-yield bonds.

- In our view, these issuers still offer historically attractive yields and are better positioned to navigate refinance risk and any potential economic slowdowns.

- Investors should be cautious of strategies targeting “fallen angels,” as a potential downgrade of Boeing and other issuers may present significant concentration risk.

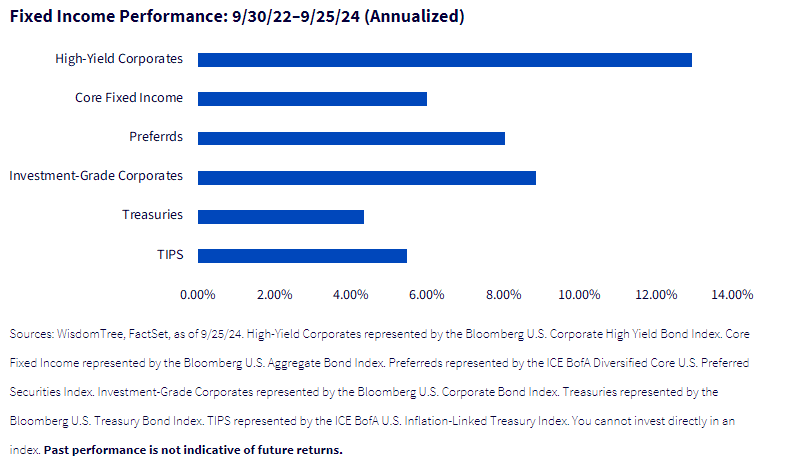

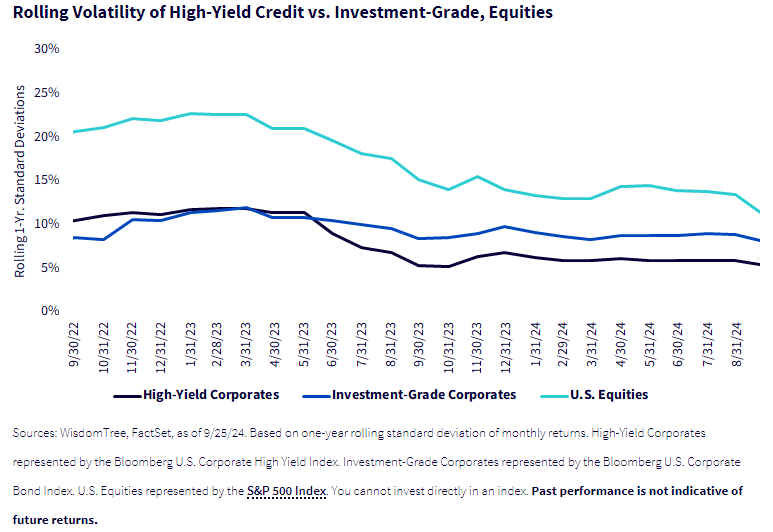

High-Yield Credit Has Delivered Strong Returns, with Less Volatility than Equities

Over the past several years, high-yield bonds have delivered impressive returns, outperforming most other sectors of the fixed income market.

This strong performance can be attributed to several key factors, including healthy investor demand, limited net new supply, robust corporate issuer fundamentals and historically low default rates.

Additionally, despite broader macroeconomic uncertainties, high-yield returns and credit spreads (the excess yield offered over Treasuries) have shown remarkable resilience and relatively low volatility.

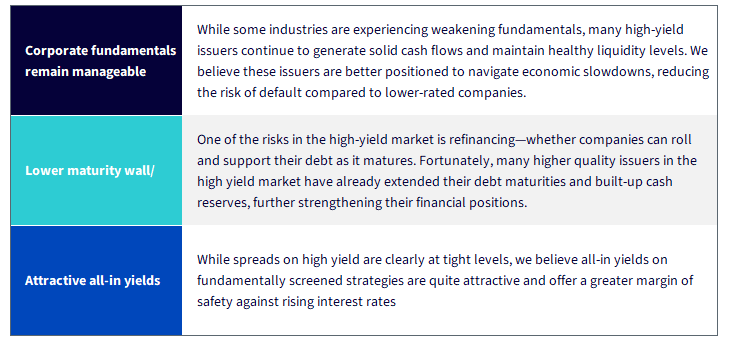

We Remain Constructive on Higher-Quality High-Yield Credit

While the spreads on high-yield bonds have now compressed to relatively low levels, we maintain a constructive outlook on the higher-quality segment of the high-yield market. Here’s why:

By focusing on higher-quality issuers, investors can benefit from the attractive risk-adjusted returns and income offered in high yield, while also mitigating some of the risks associated with lower-rated debt.

Not All “High-Quality” Strategies Are Created Equal

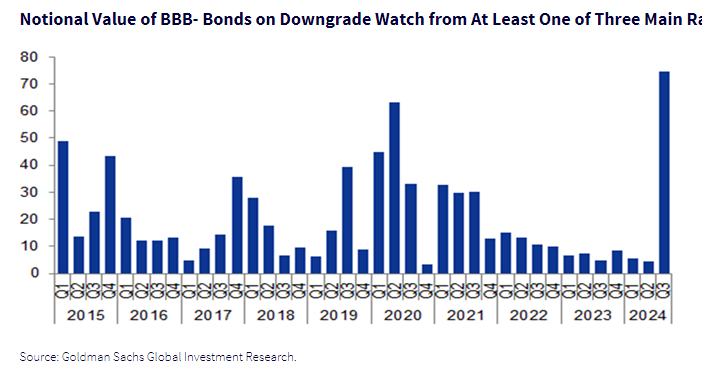

One popular way for investors to access the higher-quality portion of the high-yield universe is through “fallen angel” strategies. These strategies target bonds that were previously rated investment grade but have since been downgraded to high yield.

However, after a period of limited issuer migration, the risk of fallen angels has surged this quarter, particularly due to Boeing’s $57 billion in outstanding bonds, which are under review for possible downgrade by Moody’s.

While fallen angels may offer enticing yields, the prospects of a Boeing downgrade could dramatically increase the issuer concentration risk in these strategies, some of which have issuer caps as high as 10%!

Given the risks associated with issuer concentration in fallen angel strategies, we suggest that investors consider a broader approach to the high-yield market. Rather than relying solely on credit rating history, we believe it’s prudent to use strategies that systematically identify fundamentally strong issuers across the market.

In summary, the high-yield bond market continues to present a compelling investment opportunity for those seeking strong returns with lower volatility than equities. With careful issuer selection and a focus on quality, investors can still find attractive opportunities in today’s market environment.

This article originally appeared on WisdomTree's website and is reprinted on VettaFi | Advisor Perspectives with permission from the author. For more information, please visit WisdomTree.com.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All