Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

For many investors, the fixed income portion of their portfolio is intended to be the ballast of the portfolio. Fixed income investments are well-suited to fill the capital preservation-focused portion of a portfolio for several reasons. First, the general nature of what a bond essentially represents: a loan that the issuer is legally obligated to pay back (both principal and interest) barring the unlikely event of a default when investing in investment-grade bonds. Fixed income compensates investors and carries less risk than other, more growth-oriented investments like equities (for example, a company’s dividend can be cut or eliminated at any time at the discretion of the company). Second, the known aspects of a bond (income, cash flow, redemption date, redemption value) mean that it will provide its many benefits regardless of what the market or interest rates do. Upon purchasing a bond, and investor locks in these terms.

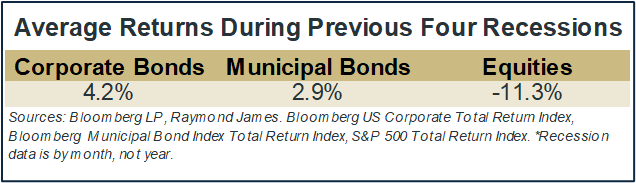

The FOMC cut the Fed Funds rate for the first time in over four years a few weeks ago. Cutting cycles historically preceded a recession, therefore it is a good time to remind ourselves of the importance of appropriate asset allocation. While past performance is no guarantee of future results, looking at how things have played out in the past can help dictate an appropriate asset allocation given an investor’s individual risk tolerance. The below chart looks at total returns for corporate bonds, municipal bonds, and equities during the last four recessions.

While the performance difference between stocks and bonds is rather substantial, it hopefully does not come as a surprise. A recession means the economy is not performing well and is in a downturn. As expected in this type of economic environment, riskier assets that rely on growth have historically not performed well while the more conservative, ballast of the portfolio tends to perform relatively much better. This emphasizes the importance of maintaining a balanced portfolio that is aligned with your personal goals and tolerance for volatility. A financial plan is ideally designed to perform and persist through multiple economic cycles, ignoring short-term swings and keeping a focus on long-term goals. While most of us are investing with an eye years or decades into the future, short-term market swings can still trigger strong emotional reactions and sometimes push investors to (inadvisedly) become short-term traders rather than long-term investors. A properly allocated portfolio can help to mitigate an emotional response that might derail a long-term plan. Is your portfolio appropriately positioned to weather the next economic downturn? Contact your financial advisor to ensure that you have an appropriate ballast constructed for your portfolio.