The last two years brought challenges for investors across all walks of life, but particularly for retirees. Soaring inflation and interest rates resulted in a rising cost of living and ongoing market volatility. This left many investors hedged in cash and forced to weather the storm through any means necessary.

According to the Natixis Investment Managers’ 2024 Global Retirement Index report, the specters of inflation and interest rates still loom large for retirees. The report includes findings from a recent survey that included 8,550 individual investors across 23 countries and highlighted the risks retirees and those saving for retirement still face.

The Interest Rate Cash Trap for Retirees

An environment of historically low rates created several challenges for retirees in the last 15 years. Elevated rates drove bond yields higher in the last two years (bond prices and yields move inverse). While it brought income back to fixed income allocations, it also resulted in many people hedging their risk in cash, money markets, certificates of deposit, and other instruments similar to cash. Natixis notes that over $6 trillion was invested in money markets as of June 2024.

The risk now becomes that investors remain in these overallocations and the long-term potential impacts on income.

“Interest rates have been among the greatest risks to retirement security since the Natixis Global Retirement Index was introduced in 2012,” Natixis wrote. “But with rates at or near 15-year highs, many may be sacrificing a sustainable long-term income for short-term security presented by cash.”

The Road Here

Extremely low rates in the last decade created several challenges for retirees looking to bonds for income. In some cases, this resulted in an overallocation to equities, particularly given their long bull run over the same period. The overweight to equities also opened up more of the portfolio to volatility exposure. This exposure proved particularly painful during the pandemic crash of 2020 and the market correction in 2022.

In the last two years, the Fed’s battle to bring soaring inflation to heel resulted in elevated bond yields. While a boon to retirees, bond exposures still carried elevated interest rate risk. Elevated yields in low-risk money markets and similar strategies during a period of elevated and ongoing market volatility proved equally, if not more, attractive. Over $6 trillion was invested in money market funds as of this summer, and advisors are concerned.

“Even with cash paying upward of 5%, 53% of these investment professionals said more attractive returns can be found elsewhere,” explained Natixis. “Another 43% said investors should be aware of inflation risk, while the same number also warned of reinvestment risk when considering cash.”

Diversifying income streams beyond cash may prove a boon as interest rates decline.

The Lingering Impacts of Inflation on Retirees

Inflation continues to slowly cool from its 2022 highs, but the squeeze of high prices proved a painful reminder of its outsized impact on retirement portfolios. Notably, this pressure was reported across wealth bands. 8,000 investors surveyed in 2023 with over $100,000 in investable assets reported rising prices as their highest financial fear. “In fact, 42% went so far as to say inflation was killing their dreams of retirement,” Natixis noted.

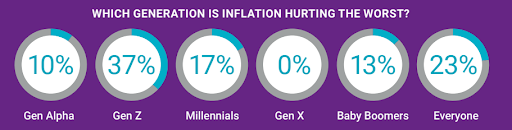

Image source: Natixis Investment Managers

While inflation and high prices prove challenging for everyone, for those on a fixed income, they create compounding difficulties. Retirees must contend with higher living costs and may be forced to dip into savings. If the money comes from savings, it leads to a smaller nest egg that may last for shorter years. If, instead, it came from investments, the reduction in assets may create longer-term challenges.

When inflation spikes, and prices rise, retirees face a difficult choice. They must choose to curtail expenses or invest in higher-risk assets to meet new income needs. “Cutting expenses can be difficult at an age when medical costs may be escalating,” wrote Natixis. “Taking on more risk may be harder, as older individuals may not have the time needed to rebuild their savings should they experience significant losses.”

Inflation doesn’t just impact retirees, however. 66% of investors surveyed reported that inflation significantly impacted their ability to save for retirement, with just 32% reporting this as a motivating factor to save more. Gen Z (those ages 12-27) feel the brunt of this most, according to Natixis strategists. The elder portion of Gen Z faces soaring rents, an elevated cost of living, school loans, and more. Entry-level jobs may not provide enough income to meet all these needs, let alone to begin saving for retirement.

For more news, information, and analysis, visit the Portfolio Construction Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more commentaries by VettaFi