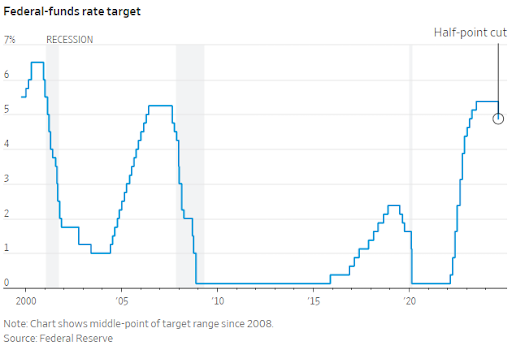

The Federal Reserve cut interest rates by 0.50% today as it continues to aim for a soft-landing scenario. The interest rate cut is the first in the Fed’s historic fight against inflation that’s lasted over two years.

The vote for the half-point cut was almost a unanimous one, with 11 of the 12 Fed officials voting to bring rates down to the 4.75%-5% range. Federal governor Michelle Bowman voted instead for a 0.25% raise, the first dissent in interest rate voting since 2005, reported the WSJ. The more aggressive 0.50% rate cut over the predicted 0.25% cut by markets reflects the pivot in focus from inflation to economic health. It’s a significant departure from the last two years of Fed policy and is the first rate cut since 2020.

Image source: WSJ

The Inflation Road Begins Downhill Coast

As inflation skyrocketed in 2022, the Fed expressed a determination to reign in inflation at all costs. This included a willingness to drive the economy into recession as long as inflation could be curbed to the desired 2% from its 9.1% peak in June 2022. Now, with inflation continuing to move closer to the desired 2% rate, the Fed turns its attention to preventing recession.

“We’re trying to achieve a situation where we restore price stability without the kind of painful increase in unemployment that has come sometimes with disinflation,” Powell said in a meeting this afternoon, reported CNBC.

Rising unemployment and a rapid slowing in payroll growth over the summer months indicate a cooling labor force. That, alongside the manufacturing sector reporting its fifth consecutive month of contraction in August, signals potential challenges to economic health. In addition to mixed economic signals, the strength and resilience of U.S. consumers remain in question. An August report from the New York Fed revealed Americans reached a record $1.14 trillion in credit card debt.

The U.S. central bank is later to the rate-cutting game, with many central banks globally already cutting rates earlier this year. For international investors, interest rate changes play a role in currency rates. A strong U.S. dollar has created several challenges for the strength of currencies internationally, which in turn puts potential inflationary pressure on domestic economies overseas. Easing the dollar’s strength could bring some relief to EM countries in particular.

Harness Rate Cut Opportunities With Small-Caps, Gold

It’s no secret that small-caps could prove to be the darling of a rate-cutting regime, should the Fed manage a soft landing. Small-caps carry greater interest rate sensitivity than their large-cap peers. Higher rates squeeze margins and create challenges as they generally carry greater debt levels.

Given their greater rate sensitivity and the squeeze they’ve experienced in the last two years, small caps offer notable rebound potential in a declining rate environment. While it’s more complex than simply rates going down and small-caps bouncing up, they’re a category to watch should the economy prove resilient.

ETFs to gain exposure to the small-cap space include the Avantis U.S. Small Cap Value ETF (AVUV) and the VictoryShares Small Cap Free Cash Flow ETF (SFLO).

See also: “Rate Cuts to be Catalyst for Small-, Mid-Cap Quality ETFs”

Gold also is a beneficiary of rate cuts. The precious metal, on a bull run this year, hit a new high this week on market expectations of a rate cut. Gold was up 23.9% YTD as of 09/13/24, according to Y-Charts data. Historically, gold and inflation have an inverse relationship, with low rates correlating to higher gold prices. Goldman Sachs forecasts for $2,700 an ounce by early next year.

Beyond rate cuts, gold is also a preferred hedge by many for economic and geopolitical risk. Given the aggressiveness of the initial rate cut, the Fed’s focus on heating up the cooling labor market only serves to underscore the economic risk that still looms over the U.S. Should the Fed not manage a soft landing, gold demand would likely increase sharply.

Gold funds to consider include the SPDR Gold Shares ETF (GLD) and the Franklin Responsibly Sourced Gold ETF (FGDL).

See also: “Gold Pushes Past $2,600 En Route to New Highs”

Look to Opportunities in Real Estate, Long Duration Bonds

Falling rates may bring relief for the beleaguered real estate sector. Record-high mortgages kept many residential buyers out of the market in the last year. On the commercial side, high rates led to declining property values. As of mid-July, commercial real estate prices declined 21% from their peaks in 2022, reported the Harvard Business Review.

An easing of rates could lead to greater market activity for the sector as a whole. Lower mortgage rates would entice more buyers on the residential side while rebounding prices benefit commercial real estate. Those investors wishing to gain exposure to the real estate sector should consider the Real Estate Select Sector SPDR Fund (XLRE) or the Fidelity Real Estate Investment ETF (FPRO).

See also: “Real Estate ETF AVRE Shines Amid Market Sell-Off”

Long-term bonds will likely prove to be a beneficiary of declining rates, as longer-duration bonds carry greater interest rate sensitivity. While pressure in a rising and high-rate environment, long-duration bond prices may rise more significantly in declining rates than shorter-duration peers. It’s important to note that bond yields and prices move inversely to each other.

Investors are also likely to sit underweight in longer-duration bonds currently. They’ve shown a strong preference for ultra-short and short-duration bonds in a rising and elevated rate environment. Now, as rates decline, greater demand may create added pricing pressure in long-duration bonds.

Fixed income funds to consider include the Vanguard Long-Term Bond ETF (BLV) with an average duration of 13.8 years as of 08/31/24 and the iShares 20+ Year Treasury Bond ETF (TLT) with an effective duration of 16.9 years as of 09/17/24.

For more news, information, and analysis, visit VettaFi | ETF Trends.

VettaFi LLC (“VettaFi”) is the index provider for SFLO, for which it receives an index licensing fee. However, SFLO is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of SFLO.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more commentaries by VettaFi