Municipal August update

- Munis cemented their best “summer” since 2010 after another month of strong performance.

- Some near-term caution is warranted given that September has been historically challenging.

- Robust issuance ahead of the election should provide opportunities in the primary market.

Market overview

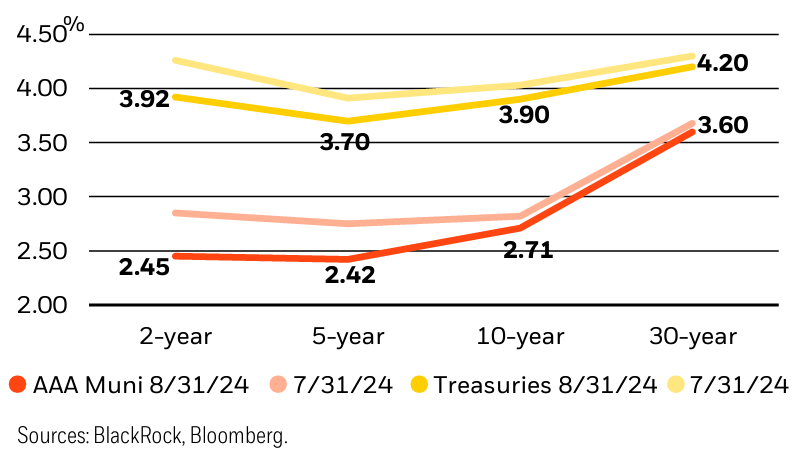

Municipal bonds posted their third-consecutive month of positive performance in August. Continued weakening in economic data and rhetoric from the Federal Reserve that “the time has come for policy to adjust” solidified expectations for a series of rate cuts starting in September and pushed yields lower across the curve. The S&P Municipal Bond Index returned 0.82%, bringing the year-todate total return to 1.86%, but slightly underperformed comparable Treasuries. High yield credits, the intermediate part of the yield curve, prerefunded bonds, and the resource recovery, IDR/PCR, and tax-backed sectors performed best. The asset class has now delivered a cumulative total return of 3.28% in June, July, and August, making it the best “summer” period since 2010.

Issuance accelerated to $49 billion in August, 20% above the five-year average, bringing the year-to-date total to $322 billion, up 37% year over year. Supply outpaced reinvestment income from maturities, calls, and coupons by over $8 billion, once again negating the seasonal benefit of net negative supply that is typical during the summer. As a result, deals were oversubscribed 3.6 times on average, remaining below the year-to-date average of 4.2 times for the second-consecutive month. At the same time, demand remained firm, and the asset class garnered consistent inflows.

Looking ahead, September has been the worst-performing month of the year, on average, over the past five years. Thus, given recent performance strength, some caution is likely warranted. However, with issuance expected to remain robust as deals are pulled forward ahead of the election, the new issue market should provide ample opportunity to source bonds at attractive concessions.

Strategy insights

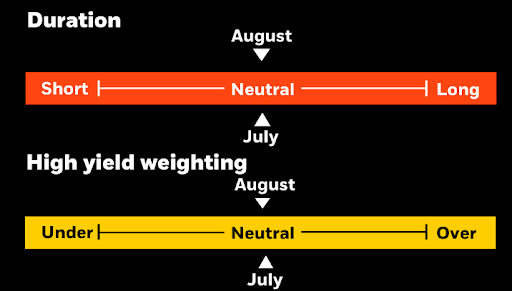

We remain neutral duration overall. We maintain a barbell yield curve strategy (0-2 years and 15-20 years), though we see increased value in the belly after the recent steepening. We prefer single-A rated credits but think high yield offers a good risk-reward opportunity, given attractive carry, favorable structures, and the ability to generate alpha through security selection.

Overweight

• Essential-service revenue bonds

• Suburban governments and school districts

• Flagship universities

• Select issuers in the high yield space

• National and large regional health systems

Underweight

• Speculative projects with weak sponsorship, unproven technology, or unsound feasibility studies

• Senior living and long-term care facilities

• Small private colleges

• Stand-alone and rural health providers

Credit headlines

After five missed interest payments, holders of the 2017 $287 million Wisconsin Public Finance Authority bonds, backed by New Jersey economic development grants from sales tax collections at the American Dream megamall, received $25.7 million of the $46.4 million in overdue interest payments. The delays were due to documentation issues with state grant appropriations. Triple Five, the developer, borrowed an additional $800 million in revenue bonds backed by payments in lieu of property taxes (PILOT), along with nearly $3 billion in private loans, to finance the $5 billion project. The mall, a high-profile credit in the high yield municipal market, has been plagued with construction delays, cost overruns, and a lockdown a few months after its October 2019 opening. Sales have been improving with two-consecutive quarters of double-digit increases, although they remain well below the initial projections. Despite the mall’s financial struggles, the PILOT bonds have remained current, with reserve funds covering the shortfalls due to reductions in the assessed value and tax rate on the complex.

Tower Health, a not-for-profit healthcare system in Pennsylvania that was initially rated single-A from all three agencies and is now rated NR/CC/CCC, is planning to restructure its debt. The plan involves issuing $1.3 billion of new revenue bonds in exchange for its $1.2 billion of existing debt. The move aims to provide Tower with increased liquidity and flexibility. Despite recent financial improvements, including a reduced operating loss, Tower would have faced mandatory upcoming debt obligations that will now be pushed out. The restructuring is seen as an effort to continue its turnaround efforts, with the exchange offer expiring September 13.

Municipal and Treasury yield movements

Municipal performance

Investment involves risk. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from tax-exempt bonds may be taxable. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of Sept 11, 2024, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader.

©2024 BlackRock, Inc or its affiliates. All Rights Reserved. BlackRock is a trademark of BlackRock, Inc or its affiliates. All other trademarks are those of their respective owners.

Prepared by BlackRock Investments, LLC, member FINRA.

Not FDIC Insured • May Lose Value • No Bank Guarantee 374000-0824

374000-0824

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© BlackRock

Read more commentaries by BlackRock