In this article, Russ Koesterich discusses why the next bout of market volatility may last a bit longer than previous downturns and how to best position your portfolio against this backdrop.

Key takeaways

- While fall has historically been a weaker period for equities, this year may be compounded by extended seasonal weakness.

- In this environment, investors should consider hedging strategies to help protect gains in their portfolio.

- One solution is to purchase put options which are currently pricing at historically cheap levels.

In early August investors experienced a violent, albeit brief spike in market volatility. If seasonal patterns are any guide, the next spike may last a bit longer. As we enter fall, historically one of the weaker periods of the year, investors should consider hedging strategies to protect this year’s substantial gains.

I last discussed seasonality back in the spring. I highlighted that while there is some truth to the adage, ‘Sell in May and go away’, election years tend to have somewhat different seasonal patterns. Rather than summer weakness, markets are more likely to stumble in the fall. Year-to-date this pattern has held. Even after suffering a near 10% drawdown in early August, as of late August the S&P 500 is 10% higher than it was in late April.

But while stocks have remained resilient, and solid year-to-date momentum suggests more gains into year’s end, seasonal patterns are now turning less favorable. This suggests not only weaker returns but also higher volatility. With current implied volatility below average, as derived from options pricing, investors have an opportunity to hedge their equity exposure with relatively cheap options.

Investing involves risks: Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of “Characteristics and Risks of Standardized Options.” Copies of this document may be obtained from your broker, from any exchange on which options are traded or by contracting The Options Clearing Corporation, (1-888-678-4667).

During election years going back to 1990, the CBOE Volatility Index (commonly referred to as the VIX index), which tracks implied volatility on the S&P 500 Index, has typical risen around 10% in September and another 25% in October. This equates to an average VIX level of 25 in the October preceding a U.S. Presidential election.

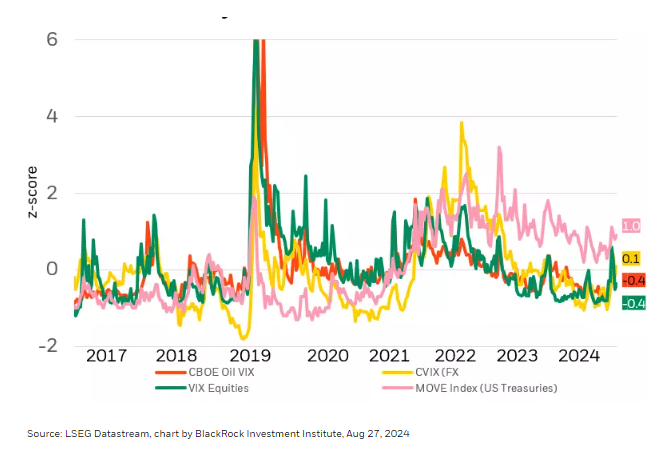

As of late August, markets did not appear to be discounting the traditional rise in volatility. While equity volatility spiked in early August, the rise, while historic, was remarkably short lived. By the end of the month, implied volatility had faded, back near the long-term average across multiple asset classes (see Chart 1).

Chart 1

Cross - asset volatility

Not only is current volatility modest, but looking at future contracts on the VIX Index, investors are not expecting a significant rise any time soon. The October contract suggests only a small rise in volatility in October, to approximately 18, versus the average level of 25 in prior election years.

While recent economic data, particularly strong July retail sales report, has allowed investors to breathe a sigh of relief, there are some legitimate sources of volatility lurking in the background. In the coming months, investors will need to balance the risks of a slowing economy, aggressively priced expectations for Fed rate cuts, lingering geopolitical risk and what is likely to prove a close election. All of which suggests that equity volatility has the potential to rise significantly from current levels.

Use cheap option volatility as a hedge

Last month I advocated trimming equity exposure and emphasizing consistency in portfolios. A third strategy for investors to consider is to use cheap volatility to buy protection, i.e. put options and structures that rise in value in the event of a decline in price and/or a rise in volatility. Currently, these options are unusually cheap, providing an opportunity to protect gains as the traditional summer lull comes to an end.

About the Author

Russ Koesterich, CFA, JD, Managing Director and portfolio manager, is a member of the Global Allocation team.

Mr. Koesterich's service with the firm dates back to 2005, including his years with Barclays Global Investors (BGI), which merged with BlackRock in 2009. He joined the BlackRock Global Allocation team in 2016 as Head of Asset Allocation and was named a portfolio manager of the Fund in 2017. Previously, he was BlackRock's Global Chief Investment Strategist and Chairman of the Investment Committee for the Model Portfolio Solutions business, and formerly served as the Global Head of Investment Strategy for scientific active equities and as senior portfolio manager in the U.S. Market Neutral Group. Prior to joining BGI, Mr. Koesterich was the Chief North American Strategist at State Street Bank and Trust. He began his investment career at Instinet Research Partners where he occupied several positions in research, including Director of Investment Strategy for both U.S. and European research, and Equity Analyst. He is a frequent contributor to financials news media and the author of two books, including his most recent "The Ten Trillion Dollar Gamble."

Mr. Koesterich earned a BA in history from Brandeis University, a JD from Boston College and an MBA from Columbia University. He is a CFA Charterholder.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please click on the fund tile.

The Morningstar Rating for funds, or "star rating," is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of September 2024 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2024 BlackRock, Inc or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH0924U/S-3849539

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© BlackRock

Read more commentaries by BlackRock