In this article, Russ Koesterich analyzes the leadership reversal and market sell-off observed in recent weeks and shares his thoughts on why an emphasis on equities with consistent fundaments is justified.

Key takeaways

- The broad risk-off trade that started in mid-July has been sharp, with equities down ~10%.

- Several factors likely led to this with the main catalyst an increase in recession fears across market participants.

- While economic growth is moderating, we do not believe a recession is imminent. This environment underscores the importance of quality in one’s equity exposure.

It began in mid-July as a rotation away from crowded tech-names into under-owned U.S. small caps. The rotation quickly morphed into something nastier: a broad risk-off trade. While the worst damage was in semiconductor and other tech names, by Monday, August 5th broader equity indices were down close to -10% from their recent peak.

This may beg the question as to why a routine shift in market leadership turn into a rapid and violent sell-off? I believe that several factors contributed, including an abrupt reversal in the Japanese yen, which had been the funding source for many risk trades, as well as extreme crowding in several AI themed names. But the main catalyst was a pair of weak economic prints that raised recession fears. The good news: While the economy is normalizing from an inflated post-pandemic growth rate, a recession (i.e. negative growth) does not appear imminent.

Return to normal growth, not recession

Ironically, market volatility began rising in mid-July coincident to the rotation into U.S. small caps and regional banks. At the time, I was surprised by the move. Buying highly cyclical stocks into a well telegraphed growth slowdown seemed like an odd trade. As it turns out, it did not last long. Investor enthusiasm for riskier stocks quickly dissipated as recession fears rose.

While an economic slowdown is evident in the data, a recession is less certain. The recent ISM manufacturing report was soft, but manufacturing has been struggling since early 2022 and is not a big driver of the current economy. In contrast, the much larger service sector is growing at a reasonable pace, evidenced by the July ISM Services numbers.

Apart from tepid manufacturing, investors were also spooked by recent labor market numbers. While the July headline number was weak, the labor market is normalizing not collapsing. The spike in the unemployment rate was a function of higher labor force participation. Slowing job growth is a reversion to a more sustainable level after several years of above trend growth. The three-month average of net new jobs is around 170,000, consistent with modest economic growth.

Higher volatility underscores need for quality

However, while I think recession fears are overblown, I am sympathetic to investor concerns. Growth is slowing, seasonal factors are turning negative and if history is any guide, the upcoming election could be accompanied by rising volatility.

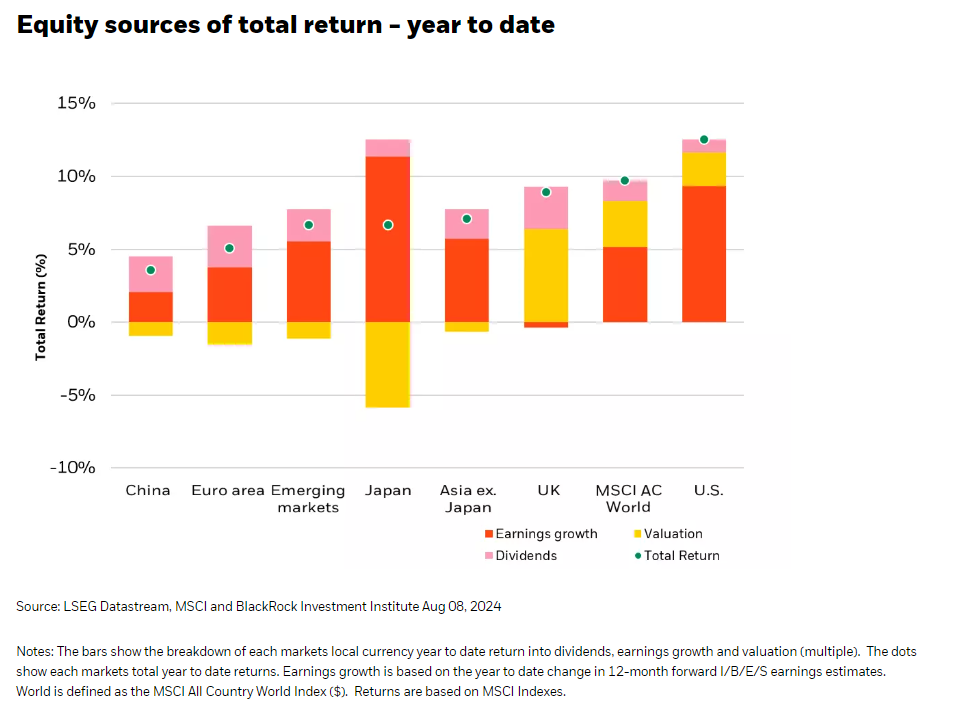

To be clear, this suggests managing risk exposure not abandoning equities. Stocks had a good run in the first half of the year, but unlike 2023 gains were powered by higher earnings not multiple expansion (see Chart 1). A trend that I think could continue in the second half of the year.

Chart 1

Rather than dramatically reducing equity exposure, I would suggest a two-pronged strategy: trim stocks and moderate cyclical exposure in favor of more stable companies. This approach would suggest emphasizing stocks with consistent fundamentals: stable revenue, earnings and margins. Many of these companies can be found in pharmaceuticals, infrastructure plays tied to energy, as well as software and higher quality consumer companies. Looking ahead, I still believe equity markets can end the year higher, albeit with some volatile days between now and November.

About the Author

Russ Koesterich, CFA, JD, Managing Director and portfolio manager, is a member of the Global Allocation team.

Mr. Koesterich's service with the firm dates back to 2005, including his years with Barclays Global Investors (BGI), which merged with BlackRock in 2009. He joined the BlackRock Global Allocation team in 2016 as Head of Asset Allocation and was named a portfolio manager of the Fund in 2017. Previously, he was BlackRock's Global Chief Investment Strategist and Chairman of the Investment Committee for the Model Portfolio Solutions business, and formerly served as the Global Head of Investment Strategy for scientific active equities and as senior portfolio manager in the U.S. Market Neutral Group. Prior to joining BGI, Mr. Koesterich was the Chief North American Strategist at State Street Bank and Trust. He began his investment career at Instinet Research Partners where he occupied several positions in research, including Director of Investment Strategy for both U.S. and European research, and Equity Analyst. He is a frequent contributor to financials news media and the author of two books, including his most recent "The Ten Trillion Dollar Gamble."

Mr. Koesterich earned a BA in history from Brandeis University, a JD from Boston College and an MBA from Columbia University. He is a CFA Charterholder.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please click on the fund tile.

The Morningstar Rating for funds, or "star rating," is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© BlackRock

Read more commentaries by BlackRock