August 2024 Monthly Market Commentary

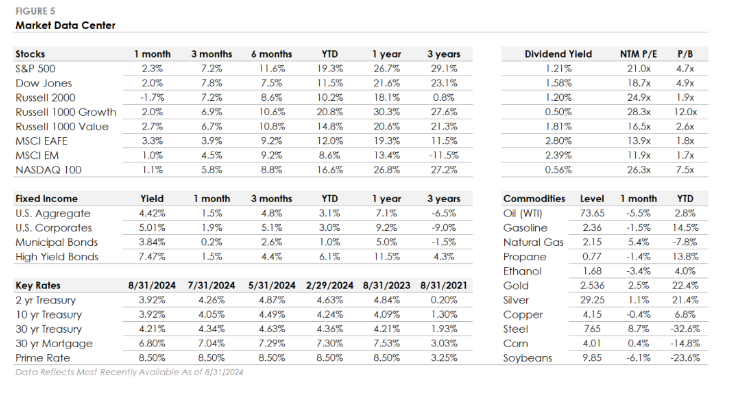

- The S&P 500 increased 2.3% in August, outperforming the Russell 2000’s decline of 1.7%. Nine of the eleven S&P 500 sectors traded higher, led by Consumer Staples, Real Estate, Health Care, and Utilities.

- Corporate investment-grade bonds increased 1.9% as Treasury yields declined, slightly outperforming corporate high-yield’s increase of 1.5%.

- International stock performance was mixed. The MSCI EAFE developed market stock index jumped 3.3% and outperformed the S&P 500, while the MSCI Emerging Market Index lagged with an increase of 1.0%.

Markets Finish Higher in August, Recovering from Early-Month Selloff

The stock market finished August higher, recovering from an early-month selloff over fears of a weakening economy. The S&P 500 dropped over 5% in the first week after a report showed unemployment rose to 4.3% in July. Small-cap stocks underperformed as investors reduced exposure to riskier assets amid spiking volatility. However, financial markets quickly stabilized and climbed throughout the remainder of the month. By month end the S&P 500 recovered all its losses, ending the month less than 1% below its all-time high from mid-July.

Meanwhile the Nasdaq 100 Index, which includes the “AI” companies that drove the stock market higher in early 2024, lagged the broader market. In the bond market, Treasury yields fell for the second consecutive month, driven by expectations for deeper rate cuts in response to rising unemployment. Fixed Income traded higher for a fourth consecutive month as Treasury yields declined and investors rushed to lock in current fixed income yields ahead of the first expected interest rate cut in September.

Fed to Slash Interest Rates as Focus Shifts to the Labor Market

The Federal Reserve is expected to start cutting interest rates at its next meeting on September 17th. Fed Chair Jerome Powell signaled the move at last month’s Jackson Hole conference by saying, “The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook and the balance of risks.” It was the Fed’s clearest policy signal since it last raised interest rates 14 months ago.

The Fed’s transition to cutting interest rates comes as its focus shifts from lowering inflation to supporting the labor market. Since the last rate hike in July 2023, inflation has dropped from to 2.9% (from 3.3%), while unemployment has risen from 4.3% (from 3.5%). The Fed is now more confident that inflation will return to its 2% target but remains concerned about the health of the US labor market. The main focus for investors should is no longer if the Fed will cut rates in 2024, but how much and how quickly the Fed will lower interest rates. Investors anticipate that the Fed will cut rates by approximately 2% by the end of 2025, but the timing and amount will depend on the economy’s path. A weaker economy would justify more rate cuts, while a stronger economy would likely lead to fewer rate cuts.

As we have noted the most important factor to all this will be the strength of the US labor market, which represents a catch-22 for the market. The stronger the labor market, the less the Fed will likely cut rates, and the less the market may react positively.

Disclosures

This commentary reflects the personal opinions, viewpoints and analyses of the author providing such comments, and should not be regarded as a description of advisory services provided by Defiant Capital Group or performance returns of any Defiant Capital Group client. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Defiant Capital Group manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance is no guarantee of future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

A word on risk

All investments carry a certain degree of risk, including possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-U.S. investments involve risks such as currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. This report should not be regarded by the recipients as a substitute for the exercise of their own judgment. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group