August brought a bit of whiplash for investors.

Markets fell at the beginning of the month, caught in the ripples of an interest rate increase in Japan disrupting a significant currency trading strategy. This led to a brief, intense global selloff.

In the U.S., the incident was aggravated by a weak jobs report with unemployment rising from 4.1% to 4.3% – which remains historically low, it’s worth noting. The report brought the U.S. into Sahm rule territory, a macroeconomic assessment which judges whether the economy is in recession based on unemployment rate increases. Additionally, several disappointing earnings releases created a sense of caution with investors over the health of the consumer.

“However, other data has been stronger, and a soft landing still appears to be the most likely outcome for the economy,” Raymond James Chief Investment Officer Larry Adam said. “For instance, retail sales for July were up a healthy 1% and the Consumer Price Index [CPI] showed that inflation is being tamed with three-month core CPI falling to an annualized rate of 1.6%. And the stage appears set for the Federal Reserve [Fed] to kick off an easing cycle, which should support broader participation and higher equity markets longer term.”

Toward the end of the month, Fed Chair Jerome Powell said “the time has come” for the Fed to adjust policy, a much-anticipated statement for those expecting interest rate cuts this year. Those remarks kicked off an equity market rally, with the S&P 500 ending the month up 2.3% and the Dow Jones Industrial Average hitting an all-time high.

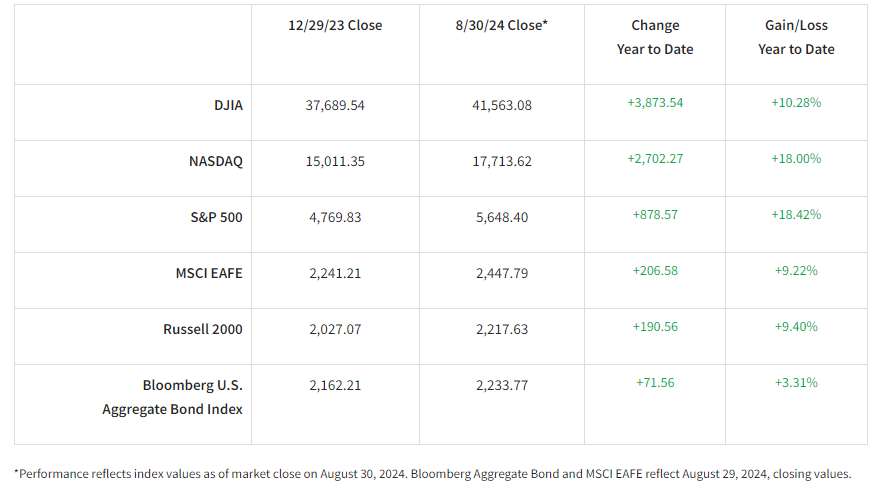

We’ll dive into the details below, but first let’s look at the numbers year-to-date:

Labor market weakens

The U.S. labor market has weakened, as suggested by data including a major revision of jobs reports spanning April 2023 to March 2024. The Bureau of Labor Statistics lowered estimates by 818,000 jobs, a 29% difference from preliminary estimates. Combined with the inflation rate continuing to decelerate, the weaker jobs numbers made the Fed’s path to lowering interest rates clearer.

S&P 500 rallies, but headwinds remain

The S&P 500 experienced a good rally – up 8% over eight days – affecting a wide range of stocks while volatility indicators remained low. This was supported by reassuring economic data, namely the third consecutive month of sub-0.2% core CPI increases and the uptick in retail sales. Headwinds remain, however, and August and September are typically the softest months of the year for stocks, so further volatility is to be expected.

An interesting dynamic developing in the S&P 500 is the subtle shift in market leadership. Defensive, interest-sensitive sectors like utilities, real estate and health care are at new highs, while the semiconductor group is down.

Treasury yields lower, rate cuts imminent

Treasurys rallied across the curve in August, bringing yields lower. One-year and two-year Treasury yields are down 35 basis points (bps) and 39 bps respectively, while the 10-year and 30-year yields are down 19 bps and 17 bps.

Fed Chair Powell’s statement from Jackson Hole indicated interest rate cuts are coming, with investors expecting two to three 25-bps cuts by the end of the year. Next year could deliver more than 200-plus bps cuts, bringing the yield curve to a more normal, upward slope.

Tech tension escalates

In its simmering trade conflict with China, the U.S. Congress is tightening control over tech exports, especially semiconductors, and seeking international support, particularly from the Netherlands and Japan. Expectations are high for new rules targeting high-performance memory chips while the Commerce Department is considering new restrictions on AI memory chips, which could impact major tech companies’ ability to sell to China.

Oil demand high, despite headwinds in China

Oil prices are down as the summer driving season comes to an end, prompting OPEC to extend production cuts. Global demand is at a record high in 2024, 3% over pre-COVID-19 levels, but is still less than oil producers hoped for early in the year. Among the reasons: China, the world’s largest oil importer, has become the first major economy where electric vehicles have reached 50% of auto sales. Meanwhile, neither the conflict in Gaza nor the one in Ukraine has had any meaningful effect on oil supply.

Japan's economy reveals fragility, UK's shows resilience

The benchmark Nikkei 225 index plunged after the Bank of Japan raised interest rates on July 31, demonstrating the fragility of the Japanese economy and financial markets. While the market has since rebounded, the country’s economy continues to face significant headwinds, including an aging population and low domestic demand.

Bank of Japan Governor Kazuo Ueda defended the decision to raise interest rates, saying the market turmoil had more to do with concerns about the U.S. economy than Japan’s, while Finance Minister Shun’ichi Suzuki argued that higher interest rates could be detrimental to the Japanese economy.

The UK economy is showing some resilience, with a 0.6% growth in GDP in the second quarter and a strengthened pound sterling. With inflation slightly above its 2.2% target, the Bank of England cut interest rates by 0.25% to 5.00% – the first cut since the start of the pandemic. However, Finance Minister Rachel Reeves discovered a £22 billion shortfall in next year’s budget, which, along with pressure to increase wages in the public sector, could have a negative effect on inflation and economic growth.

The bottom line

As we remain in the weakest seasonal period of the year, investors may expect to see some back-and-forth trading ahead. Economic data and actions from the Fed will remain key influences to watch.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Raymond James Chief Investment Officer and are subject to change. There is no assurance the trends mentioned will continue or that the forecasts discussed will be realized. Past performance may not be indicative of future results. Economic and market conditions are subject to change. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australasia and Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small-cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. The performance mentioned does not include fees and charges, which would reduce an investor’s returns. Investing in the energy sector involves special risks, including the potential adverse effects of state and federal regulation, and may not be suitable for all investors. A credit rating of a security is not a recommendation to buy, sell or hold the security and may be subject to review, revision, suspension, reduction or withdrawal at any time by the assigning Rating Agency. Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. Income from municipal bonds is not subject to federal income taxation; however, it may be subject to state and local taxes and, for certain investors, to the alternative minimum tax. Income from taxable municipal bonds is subject to federal income taxation, and it may be subject to state and local taxes. Investing in commodities is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility. The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence. The Consumer Price Index is a measure of inflation compiled by the US Bureau of Labor Studies. The Leading Economic Index (LEI) provides an early indication of significant turning points in the business cycle and where the economy is heading in the near term. This is not a recommendation to purchase or sell the stocks of the companies pictured/mentioned. Investing in small-cap stocks generally involves greater risks, and therefore, may not be appropriate for every investor. The prices of small company stocks may be subject to more volatility than those of large company stocks. The Nikkei 225 is a stock market index is for the Tokyo Stock Exchange (TSE). It is the most widely quoted average of Japanese equities. Sector investments are companies engaged in business related to a specific sector. They are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Material created by Raymond James for use by its advisors.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Raymond James

Read more commentaries by Raymond James