Key Takeaways

- Companies are investing billions into AI infrastructure to position them to meet future demands.

- As we encountered peak “AI hype,” mega-cap tech valuation multiples expanded drastically.

- Some valuations remain within historical norms and aren’t completely dislocated.

- It’s important to be valuation-sensitive with position sizing to avoid over-concentration at peak valuations.

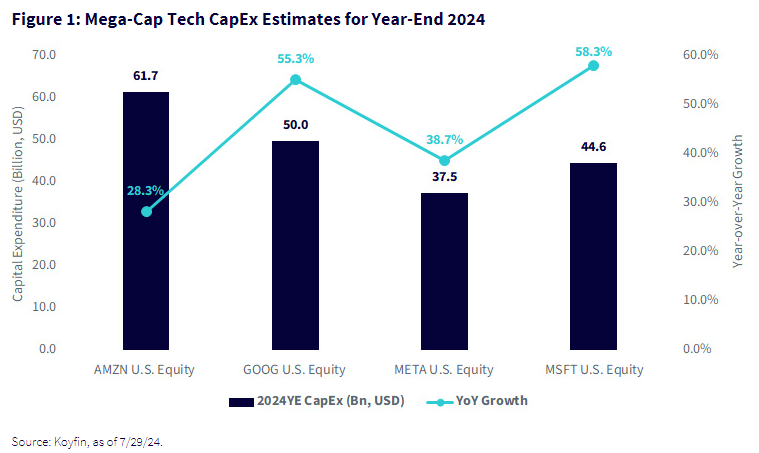

Since the release of ChatGPT, mega-cap technology companies poised to profit from AI-enhanced software tools or cloud AI-model training capabilities have seen a surge in their stock prices. Yet, many have yet to realize significant AI-driven revenue growth, let alone a substantial impact on their bottom lines. This has formed the basis for what Sequoia Capital calls AI’s $600B question—whether today’s capital expenditures (CapEx) levels can offer an estimated $600B in revenue generated from AI software and services to provide positive return on investment (ROI), given the industry’s heavy investment in hardware infrastructure.

The obvious beneficiaries of this investment so far have been Nvidia and its semiconductor peers, who are experiencing exponential revenue growth due to the high demand for AI training chips. With significant capital expenditures being made to purchase these chips and build the next wave of AI data centers, several critical questions arise: Will end users and enterprises see enough value to justify these costs? Will current investments in AI infrastructure deliver positive returns? And most importantly, are these firms fairly valued?

In this blog post, we will focus on the question of valuation, examining whether the current stock prices of these tech giants are justified given the modest impact of AI on their revenues so far.

Valuation Trends and Market Sentiment

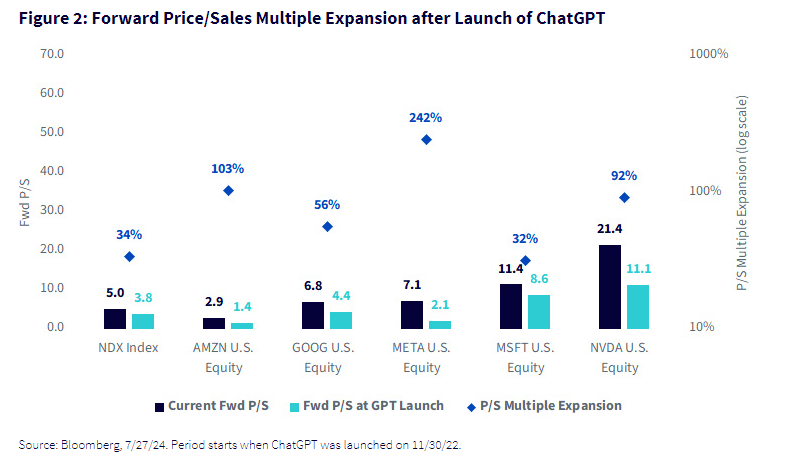

The narrative has always positioned AI as a software revolution. While semiconductors serve as essential tools, it’s the software that will be the key differentiator as users seek the most advanced, intelligent platforms. Consequently, mega-cap tech companies have seen significant stock price appreciation since ChatGPT’s launch, driven by investor optimism about AI’s potential future earnings being concentrated among these prominent players. However, this enthusiasm has led to valuation multiple expansions, which many believe may indicate a bubble.

Examining the period since ChatGPT’s launch, figure 2 shows that the Nasdaq forward price-to-sales (P/S) ratio expanded from 3.8 to 5.0, a moderate 34% increase. However, Amazon, Google, Meta and Nvidia all saw expansions of more than 50%, with some exceeding 100%. This could imply that these stocks are overvalued, or it might indicate that the market considers them fairly valued given the expectations of substantial future AI revenues and earnings potential beyond current forward sales estimates.

More recently, Wall Street’s sentiment toward these firms has shifted from positive to negative as investors question the potential ROI from large capital expenditures and the timeline for realizing these returns. Recent earnings reports from major tech companies revealed mixed results.

Amazon’s stock declined due to a cautious revenue outlook and disappointing sales, compounded by rising costs to expand Amazon Web Services. Microsoft reported slowing growth in its Azure cloud-computing arm and plans to continue substantial investments in data centers. In contrast, Meta posted strong earnings, appeasing investors and buying time for its AI investments to bear fruit. Meanwhile, Alphabet’s shares fell after the company surprised Wall Street with sharply higher costs, overshadowing its better-than-expected sales. The impact of a weaker-than-expected jobs report at the end of the week further exacerbated declines in these stocks, prompting investors to reassess their positions amid a slowing economy. As a result, there have been significant multiple contractions as investors sell shares and reposition themselves. The valuation premium previously afforded to these stocks has diminished as concerns grow that the AI hype may not meet expectations.

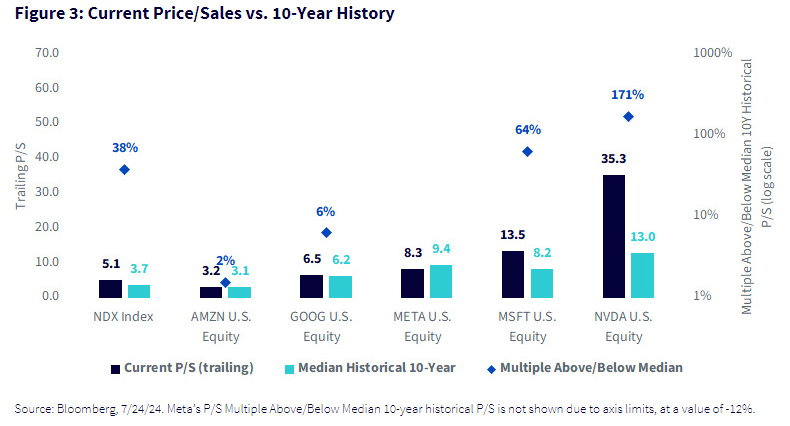

Examining current P/S ratios in the context of historical trends can provide valuable insights into whether valuations have become stretched compared to the past. Figure 3 sheds light on whether the recent pullbacks in stock prices are justified.

Nvidia and Microsoft stand out as notable outliers, with current P/S ratios significantly higher than their historical 10-year medians. This could suggest that the market expects fair value for extremely strong growth ahead, or it could indicate overvaluation. By piecing together forward and historical ratios, we see that Amazon, Google and Meta have recovered from relatively low valuation ratios recently. With significant multiple expansions post-GPT launch, they have returned to valuations that are in line with their historical numbers. However, the story may be different for Microsoft and Nvidia, as both have experienced significant multiple expansions beyond what is seen in the broader Nasdaq Index, materially exceeding historical norms.

AI’s potential as a game-changer for mega-cap tech companies might justify higher valuations now and into the future. Historically, investing in these firms five or more years ago would have been highly profitable, regardless of valuation. However, the current valuations of some indicate a significant “valuation premium” compared to the past, which likely explains why investors are now more cautious. This caution has contributed to recent price pullbacks, even amid positive earnings reports.

Historical Perspectives on Valuations

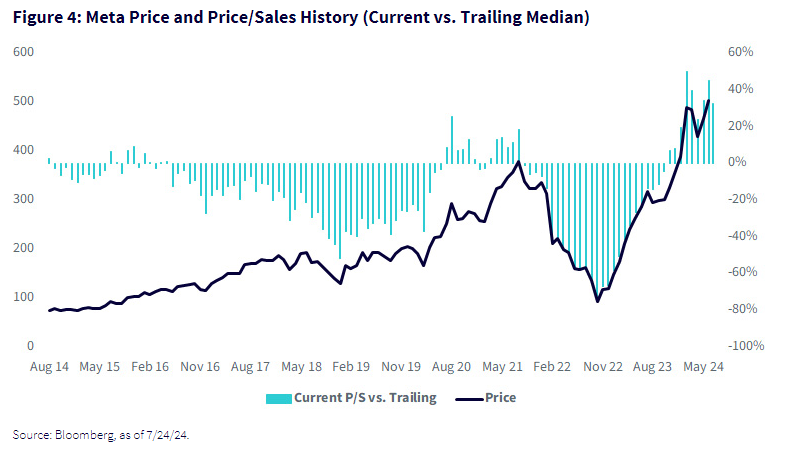

Investing in exponential technologies like AI can benefit portfolios, but it is essential to manage concentration risk and market timing. By being aware of valuation trends, investors can strategically trim positions when overvalued and add when undervalued—following the classic “buy low, sell high” adage. A 10-year chart of Meta illustrates how trimming positions during overvaluation periods and accumulating during undervaluation relative to historical norms could have been beneficial.

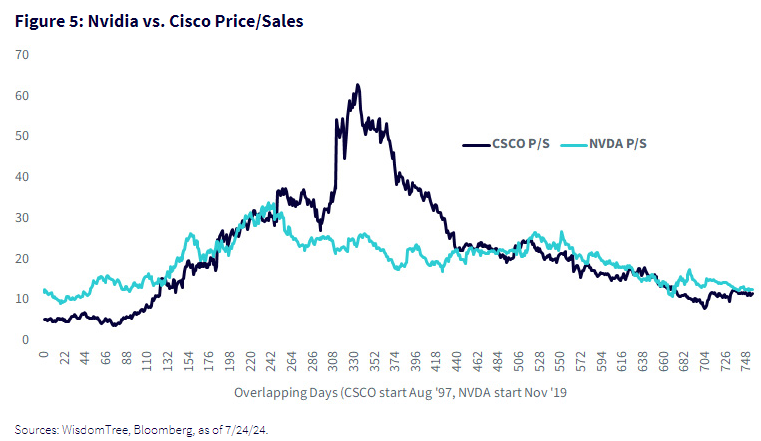

Reflecting on past market bubbles, such as Cisco during the dot-com era, can provide valuable context for remaining valuation-sensitive when investing in technology equities. Cisco’s P/S ratio soared to 60 before the stock price collapsed by more than 80% in the early 2000s. Comparatively, Nvidia’s current P/S of approximately 35 is not at dot-com bubble levels, indicating a less extreme valuation.

This historical perspective helps address the question, “How far is too far?” when valuations seem stretched. While mega-cap tech firm P/S ratios have expanded significantly since the onset of the AI wave, they remain well below the extremes seen during the dot-com bubble. This suggests that although valuation multiples have increased since ChatGPT’s launch, we are not witnessing a bubble akin to the early 2000s.

Conclusion

While investing in AI and exponential technologies is exciting, a valuation-aware approach is crucial. Rather than avoiding these investments entirely, investors should adjust their exposure as valuations fluctuate, ensuring they avoid over-concentration at peak valuations and maintain a diversified portfolio.

At WisdomTree, we seek to take this approach in our WisdomTree Artificial Intelligence and Innovation Fund (WTAI), which invests in the entire AI ecosystem and value chain. With exposures in software and semiconductors, as well as other important hardware key to the value chain, the Fund remains diversified by taking a modified equal weighting approach, with the flexibility to rebalance allocations where dislocations may be by trimming positions that may have been “too far stretched” while adding to those that may be “underappreciated,” giving investors the benefit of flexibility within a highly dynamic market environment.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

This article originally appeared on WisdomTree's website and is reprinted on VettaFi | Advisor Perspectives with permission from the author. For more information, please visit WisdomTree.com

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© WisdomTree, Inc.

Read more commentaries by WisdomTree, Inc.