The growth of bureaucracy around the world has led to a proliferation of rules. This creates multitudes of problems, one of which is that the state has made understanding what it is doing impenetrable, boring, nuanced, and technical. With vast resources, numerous employees, activist attitudes, and widespread presence, government bureaucracies have become so complex that few people can, or even want to, keep track of their activities.

There is no better example of this than the Federal Reserve. When the Fed was founded in 1913, the US was basically on a gold standard. Slowly, but surely, the standard was diluted until Richard Nixon finally closed the gold window in the 1970s. Though, even after that, at least interest rates were tied directly to the amount of reserves that were in the system.

Then in 2008 the Fed changed the rules in such a dramatic way that they severed the connection between the amount of money in the system and the level of interest rates. The confusion this has created is rarely recognized. The press doesn’t ask questions about it, the Fed won’t explain it, people get numb thinking about it. And the world just moves on at its peril.

However, financial markets sense that monetary policy is unhinged. Even before inflation hit a 40-year high, gold prices started to rise. Now, gold has reached all-time record highs as markets watch central banks abuse money like they have so many times before.

At the same time, cryptocurrencies have become extremely popular. So popular that presidential candidates have embraced the crypto community in an attempt to reach the one in three voters who say a candidate’s stance on crypto is a consideration in how they will vote. In an effort to avoid cynicism, we assume politicians understand that crypto currencies are partly fueled by a mistrust of government. But in reality politicians may not understand and are simply placating this group to get votes. We hope this isn’t true.

The value of money is as least as important to a nation as its constitution. A constitution sets out rules for government and people in a society, while money (whether we like it or not) measures the progress and success, or failure, of those rules. Prices are key to determining the allocation of resources, but if the value of money cannot be trusted then social cohesion is frayed. Throughout history, governments have abused money…from the Romans clipping coins, to the end of the gold standard, to quantitative easing and the creation of an “abundant reserve” monetary policy in 2008.

Unfortunately, explaining this in detail requires time and can be tedious and nuanced. We hope you’ll settle in and take the time to understand how monetary policy has gone off the rails since 2008. The dangers to the US, and even the world, are very real, yet few people fully grasp the implications.

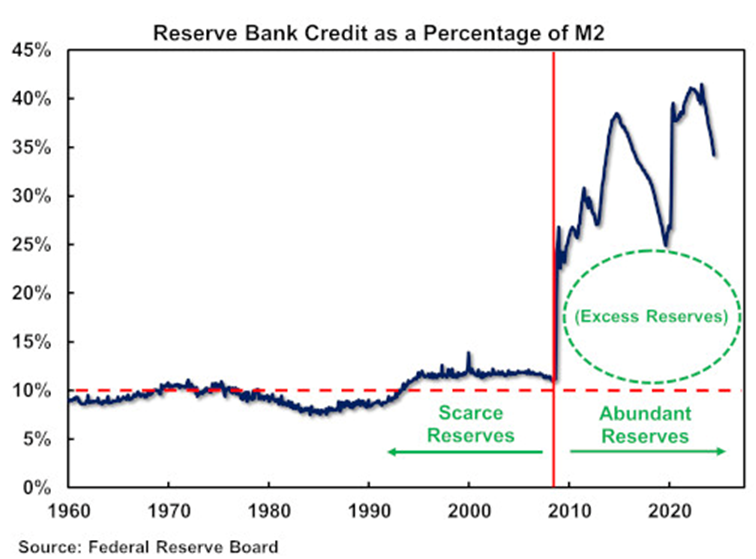

Scarce Reserves

Ever since the US shut the gold window in the early 1970s, monetary policy has had no real anchor. Gold conversion forced some discipline onto the government because investors could demand payment in a fixed price of gold for inflated and devalued currency. Ending that ability gave the Fed free reign to print money without a corrective mechanism other than when voters – and therefore politicians – revolted against inflation.

Nonetheless, the federal funds rate, the amount of reserves, and therefore the money supply were connected. It worked like this: if someone deposited $100 in a bank, that bank had to hold 10% reserves ($10) at the Fed. This made sense…even if government had no rules, banks still needed to hold reserves because deposits and withdrawals don’t always happen at the same time. Over time, 10% became the convention.

You can see in the chart below, from the 1960s through 2008, this is exactly how the system worked. Reserves averaged about 10% of M2 (a broad measure of bank deposits, including checking and savings accounts, CDs and cash). In 2007, the Fed’s Reserve Bank Credit (the Fed’s balance sheet) showed banks held $850 billion of reserves, while M2 was $7.5 trillion. This means banks held about 11% reserves at the Fed.

How did it all work? Banks had to report at least quarterly that they held 10% reserves. Just about every bank had a Federal Funds Trading Desk (unless they were small then they worked with larger correspondent banks). The traders on the desk were responsible for borrowing or lending reserves with other banks to keep everyone at the 10% level. If a bank made a big loan or had a big withdrawal of cash, it would need to borrow reserves in order to comply with the 10% rule. The more banks needed to borrow, the higher the federal funds rate would climb.

If the demand for money picked up (let’s say because home builders started building more and borrowed to do it), this would increase the money supply and banks had to hold more reserves. The trading desks would search for more reserves, and bid the federal funds rate up to get them. The Fed didn’t want this to happen, so it would inject money into the system by buying bonds, supplying more reserves. This brought the federal funds rate back down.

In other words, the Fed would accommodate the increased demand for money. If the process worked in reverse, and demand for loans fell, reserves would rise, and the federal funds rate would fall. The Fed would then sell bonds into the system to drain reserves and push rates back up. So even though the Fed could add or subtract reserves, there was still a market between banks for the reserves that were available.

The Fed could keep rates low by adding reserves, but if they added too many reserves this would increase the money supply, which in turn would increase inflation. This is exactly what happened in the 1970s. The Fed grew reserves by enough to hold interest rates down, but this meant they were adding reserves faster than money demand was increasing. Inflation was the result.

To summarize: even though the Fed controlled the amount of reserves in the system, banks traded federal funds every day. This meant there was a market-based mechanism at least partly responsible for the level of interest rates. This market-based mechanism of trading federal funds sent real signals to the financial markets about the supply and demand for money.

Look at the chart again. From the early 1960s through the mid-1970s, the Fed allowed reserves to rise from roughly 9% to roughly 11%. While this change may appear minor, banks multiplied these reserves, resulting in a significant increase in money circulating through the system. This expansion contributed to the inflation of the 1970s. However, beginning in the mid-1970s, and accelerating after Paul Volcker became Fed Chairman in 1979, reserves decreased from 11% of M2 to below 8%.

If banks needed to have 10% reserves, and there were only 8% available, imagine how difficult it was to borrow those reserves when the Fed drained them from the system. This is why interest rates shot higher in the late 1970s and early 1980s. Banks were forced to pay very high rates to borrow “very scarce” reserves, and at the same time slow the growth of their balance sheets. This slowdown in the money supply fixed the inflation problem, but it also pushed the US economy into two deep recessions in the early 1980s.

As an aside, many people think Volcker fixed inflation by boosting interest rates. This isn’t true. Volcker stopped focusing on rates at all and focused on the money supply. He knew rates would go up but didn’t really care because the way to fix inflation is to stop printing excess money. So, he squeezed reserves and let rates go where they may.

The Switch to Abundant Reserves

Then in 2008, everything changed. What is called the Great Financial Crisis led the Fed to move from a scarce reserve model to an “abundant” reserve model. The Fed calls this an “ample” reserve policy because that sounds better, as if they are doing the system a favor. If we had our way it would be called “excessively abundant” because reserves are now excessive…the Fed has grown its balance sheet roughly 10 times larger in the past 16 years. Put us in charge, and our first order of business would be to move the Fed back to a “scarce” reserve model.

Why? Because an abundant reserve policy has completely decoupled the money supply from interest rates. Look at the chart again. When the Fed did three rounds of quantitative easing during the Panic of 2008, it flooded the banking system with new deposits. During the panic, the Fed got the go ahead to pay banks interest on reserves. Prior to this, banks earned nothing on reserve deposits at the Fed. But now, the Fed could fill banks up with deposits and reserves, and then pay them not to lend them, avoiding the inflation that would have come with increased lending.

The Fed also changed the rules for banks by installing much more stringent liquidity rules and higher capital standards. In other words, even though the amount of deposits in the banking system soared, banks were forced to hold most of this excess cash as reserves at the Fed. This is why all the predictions of hyper-inflation from 2008-2015 never came to fruition. Reserves soared to roughly 40% of deposits, but M2 did not accelerate, continuing to grow around 6% per year. But banks have been flooded with reserves and new deposits. In fact, 60% of the current US money supply has been added in just the past 16 years.

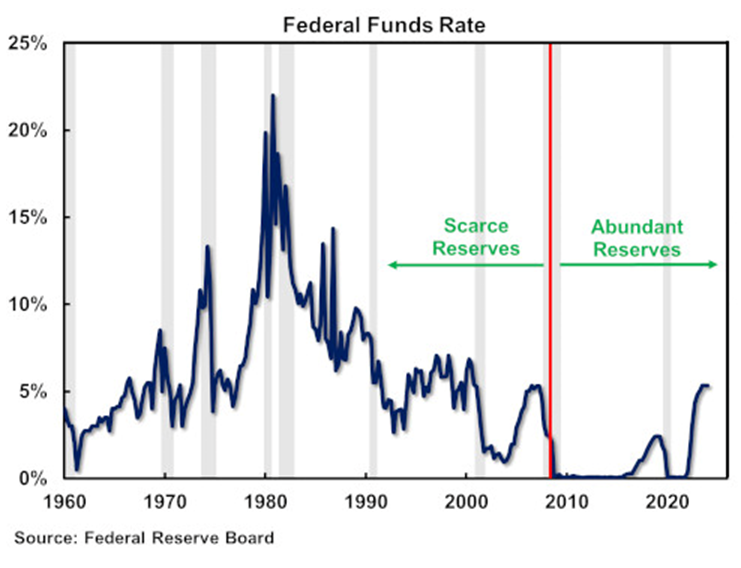

So, where does the Federal Funds Rate come from? There are no traders (all the Federal Funds Trading Desks are gone). Virtually no banks need to borrow reserves anymore, a vast majority have excess reserves now. There is no market for fed funds. If there is no trading, then guess what? The Fed just makes it up. Seriously, 12, or 17, or whatever number, people sitting around a table in Washington DC just make up the interest rate. There is no longer a true market, we have government price fixing for the most important interest rate in the world.

Here is a chart of the Federal Funds Rate back to 1960. Look at the difference between how the market moved before and after 2008. The left side looks like a market, it’s volatile, the right side looks like price fixing, it’s smooth. Interest rates are supposed to compensate investors for inflation, but the Fed has held interest rates below inflation 80% of the time over the past 16 years.

Now consider if you are a government with a debt of $35 trillion and you also get to set interest rates, where would you set them? The 400 Ph.D. economists at the Fed decided that holding them at 0% for nine of the past 16 years was appropriate. Convenient! But at least 0% was more appropriate than the negative interest rates that were seen in Europe and Japan.

But there is another point that comes from looking at this chart. Because people have wrongly interpreted Volcker as fixing inflation by raising interest rates, they believe Fed rate hikes to be the critical tool to fight inflation today. This isn’t true, either. Ben Bernanke held the funds rate at 0% for seven years and yet the US did not experience inflation. Why? Because Bernanke did QE with 0% rates but squeezed banks with new regulations and kept M2 from growing excessively.

Jerome Powell only held rates at 0% for two years, but COVID policies juiced the M2 measure of money by over 40%. That’s why Powell’s QE turned into inflation, but Bernanke’s didn’t. In other words, the reason inflation is falling today, and at the same time the economy is slowing, is because the money supply has declined by more than at any time since the Great Depression. Not because interest rates are up.

The Mess Must Be Fixed

We think we described this change in Fed policy adequately. However, to do it complete justice would take a book. There are so many nuances that we skipped. For example, because of these policies the Fed loaded its balance sheet with very low interest rate assets and now is paying private banks and private entities over $200 billion per year in interest on all their excess reserves. Yes, you read that right, the government is paying private entities hundreds of billions per year. It’s paying banks more than it is earning on its bonds and the Fed is now losing over $100 billion per year. Yet, somehow, it is still paying for the Consumer Finance Protection Bureau and its own staff of more than 20,000 employees. How is it doing this without borrowing money from the Treasury? No journalist will ask the question, and the Fed isn’t volunteering answers.

The worst inflation in 40 years was a direct result of Fed actions. Banks have failed because they believed the Fed would hold rates at 0% for even longer, while the market spends a majority of its time talking about what/when/how much the Fed might cut rates. This is what price fixing brings.

The Federal Reserve should move back to a scarce reserve model. Better yet a gold standard, or, dare we say it, a Bitcoin standard. Why? Because if the US were on a gold or Bitcoin standard, then the Fed could have never done quantitative easing. The Treasury would have had to issue its debt during the financial panic and COVID without having the Fed buy it. They would have had to pay market interest rates.

The Fed’s shift to an abundant reserve policy moves the US more into the territory of Modern Monetary Theory, where Fed and Treasury policies are intertwined. It moves the US closer and closer to a National Bank. We keep reading from former Fed leaders that Donald Trump has a plan to make the Fed subservient to the government. It looks to us like this has already happened. No matter who is in charge, monetary policy should only have one objective…to keep the value of the dollar stable. Abundant reserves put that at risk more than any policy shift in the history of the United States.

Brian S. Wesbury – Chief Economist

Robert Stein, CFA – Deputy Chief Economist

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© First Trust Advisors

Read more commentaries by First Trust Advisors