Gold Shines, Defying Historical Relationships

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways

- Gold’s performance YTD is in line with U.S. large cap equities. This strength is surprising given elevated interest rates and the U.S. Dollar, which historically has been a headwind for the metal.

- Going forward, the price of gold may continue to have support given increased demand from central banks and investors in the face of large, and increasing, U.S. fiscal debt levels.

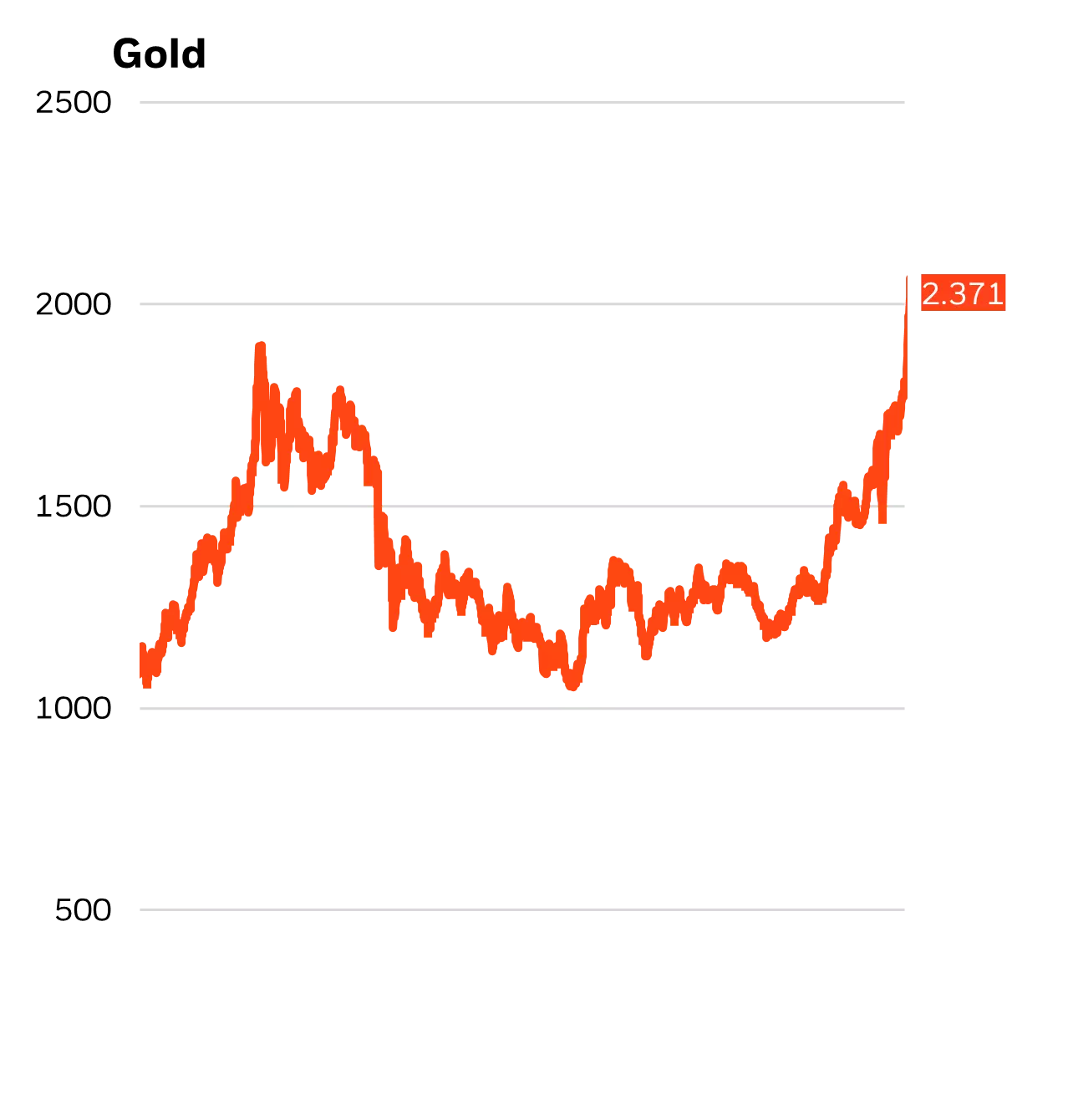

Gold is having a very good year. Following the release of the June inflation report, via the consumer price index (CPI), the price of gold surged 2%, pushing year-to-date gains to 17%. (see Chart 1). Recent gains put gold’s performance on par with U.S. large cap equities. With government bonds roughly flat over the period, gold is easily outperforming a traditional 60/40 portfolio.

Source: LSEG Datastream and BlackRock Investment Institute Jul 11, 2024

Gold’s rally is more impressive when you consider that most traditional economic drivers, notably interest rates and the dollar, should be acting as headwinds. In other words, given a higher dollar and interest rates, you would have expected the price of gold to be down, not surging higher. Instead, investors have been ignoring moves in the rate markets and instead have been focusing on central bank buying along with record levels of government debt, both of which support an exposure to gold.

Traditional relationships breaking down

I admit that I’ve been surprised, i.e. wrong about gold in 2024. While gold has benefited in recent weeks from the pullback in real interest rates, for most of the year real-rates had been grinding higher. Historically, this would have put downward pressure on gold.

The negative relationship between real rates and gold has a long pedigree. Looking at 20 years of quarterly data, changes in 10-year yields have a strong negative correlation (-0.64) with changes in gold prices (i.e. as yields have increased, the price of gold has decreased and vice versa). A similar dynamic holds for gold and the dollar. The dollar continues to defy expectations and has risen year-to-date. In the past, that would have also been associated with lower gold prices.

Watch the central banks

If not rates and the dollar, what accounts for the recent surge in gold? One catalyst has been a significant pickup in central bank buying. Based on data from Bloomberg, annual central bank precious metal purchases have quadrupled since 2020. The increase has been particularly acute for China, where gold on the central bank’s balance sheet has risen sharply since early 2023.

Outside of central banks diversifying their holdings, investors appear to also be taking note of increasingly unsustainable government budget deficits, mostly but limited to the United States. U.S. deficits appear stuck at 6-7% of gross domestic product (GDP) for the foreseeable future. Structural deficits, coupled with record pandemic stimulus efforts, have pushed gross public debt (which includes debt held by the Federal Reserve) near $35 trillion, more than 120% of GDP and a level last seen in the aftermath of WW II.

Going forward, investors may need to rethink the role of gold in a multi-asset portfolio. As the past year has demonstrated, gold may have support even in the face of elevated real rates and the near-term inflation outlook. Instead, gold appears to be evolving into a play on how central banks hold their reserves as well as a proxy for investor angst on when, if and how the U.S. address its debt problems.

About the Author

Russ Koesterich, CFA, JD, Managing Director and portfolio manager, is a member of the Global Allocation team as well as the lead portfolio manager on the GA Selects model portfolio strategies.

Mr. Koesterich's service with the firm dates back to 2005, including his years with Barclays Global Investors (BGI), which merged with BlackRock in 2009. He joined the BlackRock Global Allocation team in 2016 as Head of Asset Allocation and was named a portfolio manager of the Fund in 2017. Previously, he was BlackRock's Global Chief Investment Strategist and Chairman of the Investment Committee for the Model Portfolio Solutions business, and formerly served as the Global Head of Investment Strategy for scientific active equities and as senior portfolio manager in the U.S. Market Neutral Group. Prior to joining BGI, Mr. Koesterich was the Chief North American Strategist at State Street Bank and Trust. He began his investment career at Instinet Research Partners where he occupied several positions in research, including Director of Investment Strategy for both U.S. and European research, and Equity Analyst. He is a frequent contributor to financials news media and the author of two books, including his most recent "The Ten Trillion Dollar Gamble."

Mr. Koesterich earned a BA in history from Brandeis University, a JD from Boston College and an MBA from Columbia University. He is a CFA Charterholder.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please click on the fund tile.

The Morningstar Rating for funds, or "star rating," is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

Russ Koesterich, CFA, is a Portfolio Manager for BlackRock's Global Allocation Fund and Lead Portfolio Manager for BlackRock’s Global Allocation (GA) Selects Model Portfolios and is a regular contributor to Market Insights.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of July 2024 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2024 BlackRock, Inc or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH0724U/S-3746155

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All