The View From Canada

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEditor’s Note: I chaired an international economics conference in Canada earlier this month. Delegates from all over the world attended to discuss the issues of the day. Following is an abridged version of the meeting summary that I offered during the closing session.

I made my first trip north of the U.S. border, to Lake Kipawa in Quebec, when I was a teenager. It began a love affair with Canada that is in its sixth decade.

I first came to know Canada through its unspoiled wilderness. When I began traveling there for business, the elegance of its cities formed a lasting impression. Northern Trust has clients from the Maritimes to Vancouver Island, and I’ve had the privilege of visiting a range of Canadian locations with my partners.

I returned to Toronto in early July for a series of discussions with peers. We had a few opportunities to appreciate the city’s amazing skyline, but the beautiful backdrop was somewhat at odds with the economic picture that emerged from this year’s presentations.

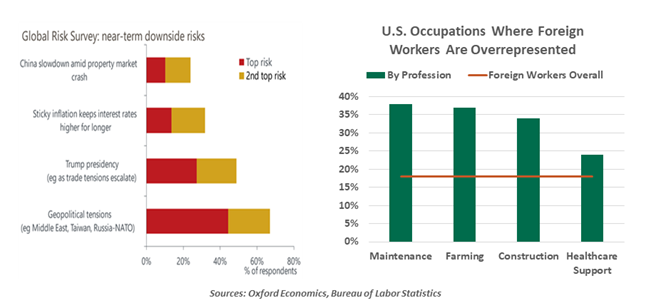

The group, collectively, had a long list of concerns. The extensive series of elections being held this year, and the negativity they seem to be generating, may be bringing otherwise latent anxieties to the fore. The resulting uncertainty will be a headwind for productive investment, economic growth, and market performance.

The Main Event

The Americans at the conference were besieged with questions from our foreign delegates about the November election. It was not easy to answer them, as the campaign was in a very fluid state. (And this was before President Biden withdrew from the race.)

No matter who emerges victorious, America is not likely to regain its appetite for global engagement. International organizations like the World Trade Organization and (dare we say it) the North Atlantic Treaty Organization (NATO) are struggling to sustain support. And that will not help anyone, anywhere rest more easily.

The biggest loser from the trend away from globalization, by a long margin, is China. Our member covering that country suggested that we are past “peak China,” offering the following evidence:

- In 2023, China’s economy grew by less than the worldwide rate for the first time in more than 40 years, and China’s economy shrank in US dollar terms last year.

- The country is in the midst of a slow-motion property crash, where small savers are among the most impacted. Consumption and confidence are slumping, and saving rates are soaring.

- China has, arguably, the worst demographic outlook in the world.

- Sufficient stimulus has not been forthcoming, perhaps because China has a substantial level of debt in both the public and private sectors. What stimulus that has been done has been implemented on the supply side, which most Western observers think is misguided.

- Low levels of inflation are becoming more deeply intrenched, and deflation is a distinct risk.

Returning to the Western Hemisphere, our delegate from Mexico had mixed feelings about what was going on with his neighbor to the north. One the one hand, Mexico has been the recipient of a substantial amount of inbound investment as firms seek a clear path to the U.S. market. On the other hand, a lot of the inbound investment has come from China, which has sought to preserve market share by white-labeling its exports.

Further, the United States-Mexico-Canada Agreement (USMCA) comes up for review in mid-2026. At that point, the signatories need to decide whether to continue on; objections by any of them would place the agreement on a path to sunset. This feature is problematic, as long tenures are thought to be essential to successful trade pacts. Our Canadian host noted that uncertainty over the USMCA may limit the ability of its participants to capitalize on reshoring.

The Republican platform also calls for more aggressive controls on immigration, and the deportation of some undocumented workers from the United States. The effort will be an expensive one: according to Forbes, it would cost $265 billion to deport the 11 million people who are in residence without visas. In addition, the loss of that many workers will disrupt agriculture, care giving and other industries which rely on their efforts.

Tougher trade terms and a reduced labor force would both be inflationary, which would complicate the task of the Federal Reserve. Those assembled were concerned that stress between the new administration and the Fed could increase, and that the independence of monetary policy could be reduced.

Restrictions on trade and immigration will add to inflation.

Prices And Policy

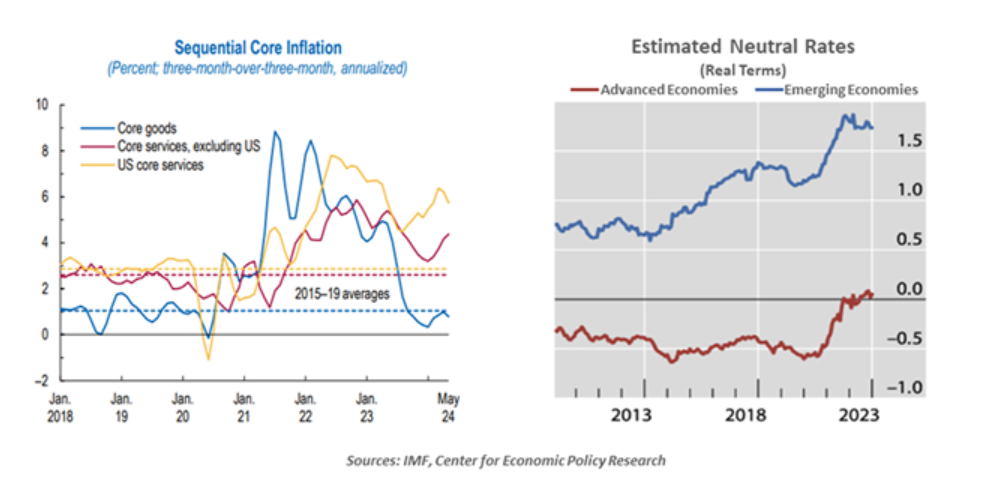

Inflation isn’t the scourge it was two years ago, but it still featured prominently in our discussions. A few insights on this front stood out:

- Across markets, core services are at the center of the last mile problem. The group had a vigorous debate over whether immigration flows, which have been heavy in several countries, are helping or harming. In the long run, the added labor supply should help, but the initial phase finds newcomers adding to consumption before they are in a position to work. This could be holding inflation up.

- Several segments highlighted the perception problem that surrounds inflation. Even though the rate of increases in prices is coming down, many households still feel as if things are terribly expensive. And they are holding politicians accountable for it.

One participant contended that inflation is relatively unnoticeable until it breaches a certain threshold. Once crossed, however, it is difficult to return inflation to the recesses of memory.

This is one reason, among many, why central banks might not be comfortable raising their inflation targets, as that would invite more occasions where price level increases pass from tolerable to intolerable.

With this backdrop on inflation, our group resumed a long-running discussion of the neutral level of interest rates. Like its algebraic expression, r-star, this remains an ethereal concept. Factors like demographics and productivity that are thought to have an important influence on r-star have ambiguous contributions.

Is AI The Answer?

One potential antidote to inflation is productivity. A potential driver of this trend is artificial intelligence (AI), which was a focus of our conversations. The group views AI as both a great hope and a great worry; our most recent piece on the topic can be found here.

The rapid improvement in natural language models is making the technology more efficient, adaptable and accurate. But like past innovations, AI will take time to adopt. Failure to account for the lag between development and acceptance can lead to an overestimation of potential in the near term and an underestimation of potential for the longer term.

Smaller economies don’t have the capacity to invest as substantially in the infrastructure that top-end algorithms require, and the international desire to restrict outside access to the data needed to train models leaves emerging markets at a disadvantage. AI algorithms also lie in that grey area between civilian and strategic applications that leads owners to look less favorably on sharing them with others.

A new paradigm for interest rates and productivity is at hand.

Those with better access to computing power and the understanding of how to use it will have an advantage in the years ahead. AI may therefore exaggerate economic inequality, leaving some populations with a more narrow path to prosperity.

If we fail to outline that path and help communities to traverse it, societies will experience higher levels of political discontent. The world’s experience with free trade is instructive here: economists did a particularly poor job in marketing the benefits of imports and exports, and in designing programs to support those who were displaced by more open borders. This added momentum to the rise of populism around the world.

Deep political divides will make it difficult for countries to address debt and deficits.

Fiscal Friction

Of the elections already behind us, the balloting in Europe will likely be the most impactful. It has been a difficult year for moderates and incumbents; the edges of the ideological spectrum have gained, making it very difficult to find a middle ground. Finances in Europe are stretched; there is little room to address imperatives like energy resilience and security, even if consensus could be reached on how to tackle them.

Spending required to recover from the pandemic added a significant new increment to government borrowing around the world, and higher interest rates have added a significant new increment to government spending. Countries have lost some control over their tax bases, given the ability of companies to manage the geography of operations and profits to minimize their tax bills.

The rate of economic growth in several European countries is in danger of falling below the interest rate, a development that can presage a debt crisis. There may be pressure in those areas on the central bank to compromise on their mandates.

There is a disconnect between political and fiscal realities. This isn’t unique to Europe, but that doesn’t make it any easier to deal with.

The potential consequences of climate change are far-ranging.

Threatening Climate

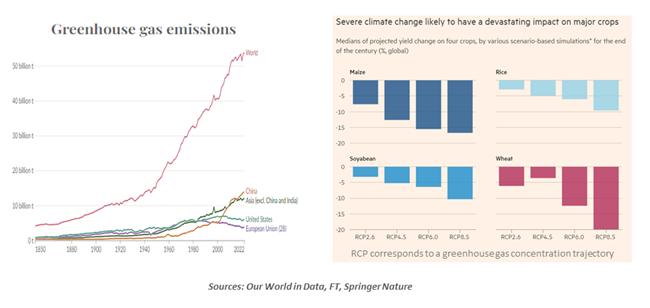

One area where international cooperation and financing will be essential is in the management of climate change. Greenhouse gas emissions have fallen in Europe and leveled off in the United States, but they are still rising globally. This raises the risk that temperatures, like interest rates, could stay higher for longer.

This scenario would have significant consequences for commerce and the quality of life in the decades ahead. The availability and cost of a range of basic foodstuffs could come under significant pressure. This, in turn, could create inflation that would lead central banks to respond with higher interest rates, creating another headwind to economic performance.

The impact on agriculture could prompt mass migration, as populations seek water, arable land and access to sustenance.

Before all of you reading give up all hope, I would note that economists have been described as people who can find a dark cloud behind any silver lining. Perhaps that is because our jobs often involve identifying potential tail risks, or it could also be that the profession tends to attract people who aren’t happy unless they are unhappy about something.

Encouragingly, most of these concerns never come to fruition. During our discussions, we noted several issues that seemed threatening at past meetings that have since receded. Pandemic scars are still visible in vacant office space and underperformance by schoolchildren, but the most dire predictions for the post-COVID world have, happily, not been realized.

For all of the challenges that lie ahead, we can’t lose sight of the fact that hundreds of millions of people around the world are much better off than they were a generation ago. And often, things that seem very pressing in one moment fade from concern in the next.

As we closed, the group expressed the wish that when fear knocks on the door, reason and faith will answer. And we are certainly hoping that concerns raised this year will have been allayed by the time the group gathers again a year from now in Dublin.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All