The appetite for nuclear energy is growing fast. Here in the US, most adults now favor expanding our nuclear power capabilities because it’s a great alternative to fossil fuels. Unlike wind or solar, nuclear provides energy around the clock. So, why haven’t we built more nuclear power plants?

It’s simple: red tape. It takes around 16 years to get a nuclear power plant up and running in the US. Globally, it’s closer to 6‒8 years.

Hopefully, that is starting to change. The ADVANCE Act, which was signed into law earlier this month, moved through Congress relatively fast thanks to bipartisan support. The Act updates the Nuclear Regulatory Commission’s framework for bringing new nuclear technologies online faster and cheaper, and for extending the lives of the nation’s 94 operable reactors.

Nuclear power accounted for 9% of US energy consumption last year. But with energy demand set to reach new highs this year and next, the US needs more power generation. Energy-hungry data centers and an increasing industrial base mean demand for electricity will continue to grow.

Billionaire tech titans are funding new types of advanced nuclear reactors. TerraPower, founded by Bill Gates, is building its first nuclear reactor in Wyoming with the help of up to $2 billion in federal funding. It should come online by 2030.

Jeff Bezos is participating, too, financially backing Canadian nuclear power company General Fusion, which aims to bring “commercial fusion energy to the grid by the 2030s.” And over at Amazon, the company he founded has purchased a massive, $650 million nuclear-powered data center campus to help support Amazon Web Services.

OpenAI CEO Sam Altman is the chairman of Oklo, a nuclear power tech firm developing fission reactors.

Building Nuclear Resiliency

One surprising weak link in our nuclear renaissance is the source of a critical resource: uranium.

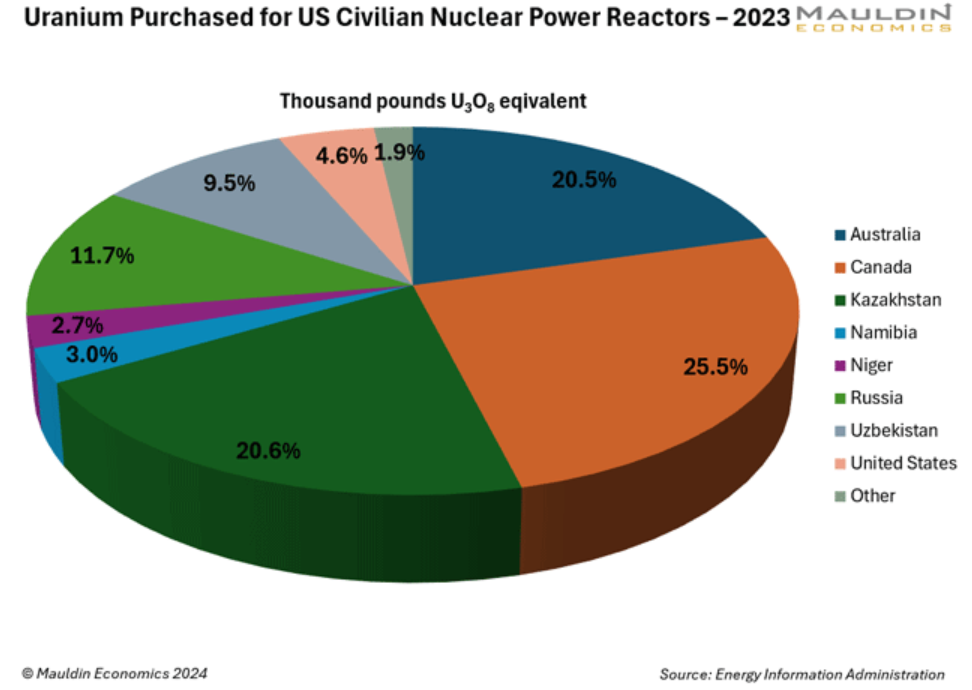

Uranium is the key input for nuclear power. Yet most of the uranium purchased by US nuclear power plant operators is imported.

In 2023, less than 5% of the uranium fueling US reactors came from US sources. That wouldn’t pose such a massive national security risk if a greater share came from Canada and Australia, which do supply a fair amount. The risk comes from relying on Russia, Kazakhstan, and Uzbekistan for a combined 41.8%.

During our interview last September, Uranium Energy Corp. CEO Amir Adnani said uranium posed “the most fundamental supply deficit of any commodity anywhere on the planet.” Here’s Amir:

“The reality is we still have a fundamental supply deficit both globally and in the US when it comes to uranium. And that, again, doesn’t include the needs of advanced and small reactors. That doesn’t include the needs of 108 microreactors that are powering the nuclear Navy. Every aircraft carrier and submarine is powered by uranium. And we’re not talking about to wage war. We’re talking about just the regular ability to roam the international waters. You look at the needs of NASA. Space travel is powered by microreactors that are powered by uranium.…

“We are facing a serious crisis when it comes to the lack of domestic production in the US. Thankfully, I think people are starting to get it. Washington’s starting to get it.”

Part of “starting to get it” is the US strategic uranium reserve—the US Department of Energy began awarding contracts to build a stockpile in 2022.

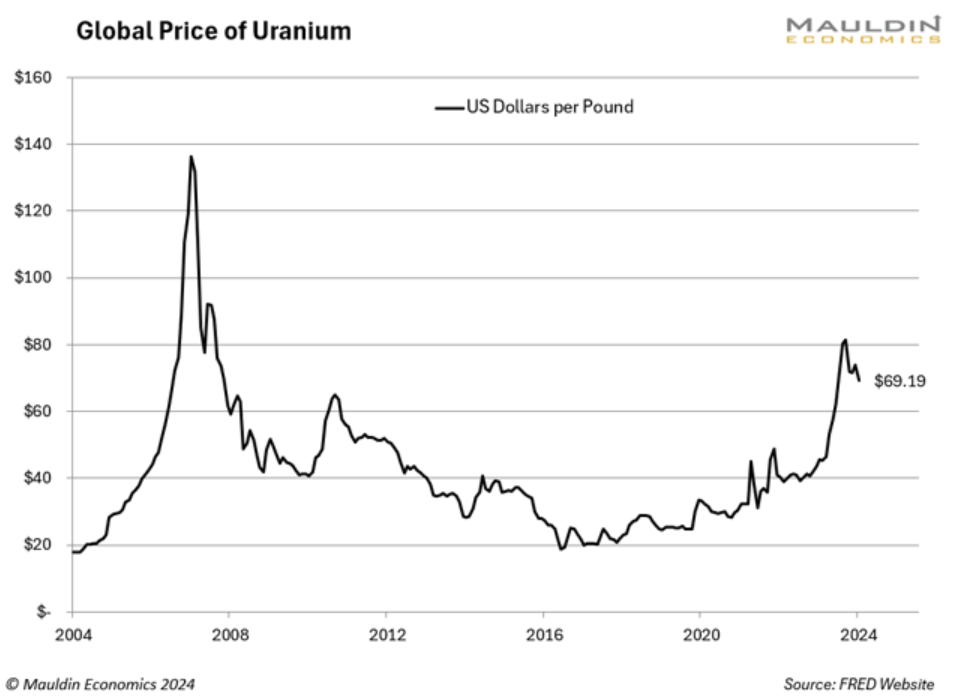

The US has uranium in the ground. At the end of 2023 domestic uranium reserves were estimated at 446 million pounds. But uranium is cheaper to produce elsewhere. And despite a substantial runup last year, uranium prices would need to stay higher for longer to induce more domestic production.

This is a prime example of the “resiliency-driven inflation” I have been predicting. The US needs to become more resilient when it comes to accessing critical inputs. Uranium is an obvious example. Prices must be higher to support the higher costs of domestic mining and refining. In the end, we may have no choice. Just as China is working hard to secure its own sources of advanced microchips, we (the collective West) should be working hard to secure our own sources of the critical inputs and commodities necessary to support our economy.

For investors, this scenario presents opportunities. Next week I’ll write about another critical input—rare earth metals.

Until then, thanks for reading. Sign up for our online discussion community here if you’d like to leave a comment or pose a question.

Ed D’Agostino

Publisher & COO

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Mauldin Economics

Read more commentaries by Mauldin Economics