Landing is the most critical phase of flight. Pilots must concentrate and use all available tools to touch down smoothly.

The Federal Reserve is in the pilot’s seat as the American economy approaches a soft landing. The runway is in sight, but some careful maneuvering will still be needed.

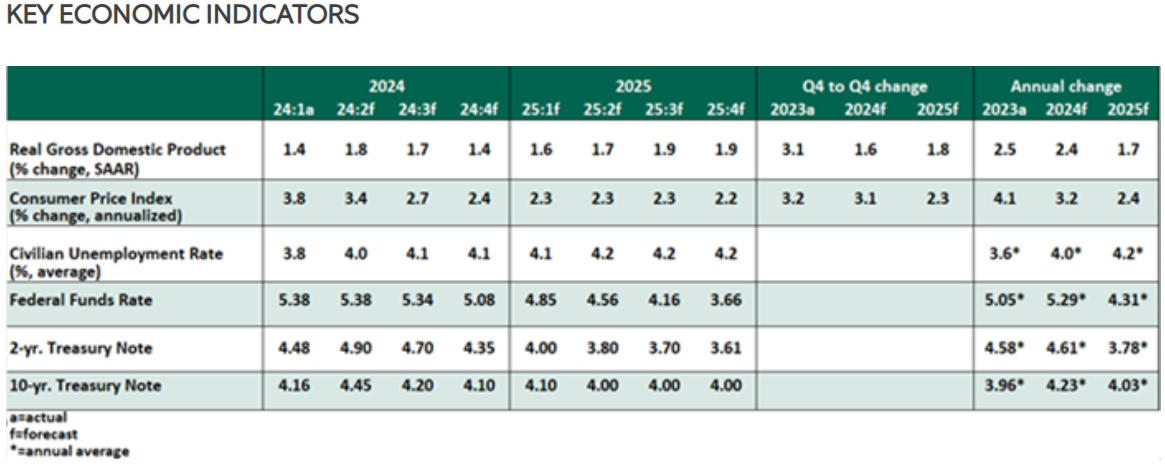

The U.S. economy continues to expand, but the pace of growth has slowed. Consumption and the labor market have moderated. We anticipate that real growth will proceed at a 1.5% pace in the second half of 2024, with only modest risk of recession.

After stalling during the early part of the year, inflation has resumed its downward trend. Hopes for a rate cut by the Fed at the September meeting have risen.

Following are our thoughts on recent data and developments.

Influences on the Forecast

- Consumer spending has moderated in the first half of the year. Consumption was revised down by 50 basis points to a 2% annualized rate. Personal consumption expenditure on goods rebounded to 0.6% month over month in May, but the overall path for goods spending this year has been weak. Expenditure on services remained soft in May. A slowdown in auto sales suggests some hesitation to make major purchases. These trends are more of a return to a normal pace of spending rather than a sign of a recession, as household balance sheets remain healthy.

- The employment report for June depicted a labor market that is settling, but still solid. The economy added 206,000 jobs during the month of June, tempered by downward revisions of 111,000 jobs to the prior two readings. The unemployment rate ticked up further to 4.1% in June, the highest since November 2021. This 0.4 percentage point increase since December 2023 is now only one-tenth shy of triggering a well-known recession indicator, the Sahm rule.

- After ticking up in May, wages resumed deceleration, moderating two-tenths to 3.8% year over year, another positive omen for underlying disinflation.

Softer demand is translating into a loosening of the labor market, fanning worries about the durability of the expansion. We think the jobs market is on track to resemble conditions before the pandemic, with no obvious signs of major cracks. Jobless claims have not risen much. Layoffs remain low, with narrow breadth. The ratio of openings to unemployed workers has reached 1.2, consistent with a balanced labor market.

- U.S. inflation continued to cool for the third straight month in June. After remaining flat in May, the headline consumer price index (CPI) declined 0.1% from May to June. On a year over year basis, the headline rate decelerated three-tenths to 3.0%. Core inflation slowed to a 41-month low, rising 0.06% month over month. A large drop in volatile components like gasoline, lodging and airfares were the main contributors to the overall monthly decline. Shelter inflation slowed sharply on a monthly basis, returning to its pre-pandemic norms, but remains elevated on a year over year basis at 5.1%.

The Federal Reserve’s favored inflation measure, the deflator on personal consumption expenditures excluding food and energy costs, moderated in May. The index increased less than one tenth of 1%, bringing the year over year change to 2.6%.

- The housing market is showing signs of cooling. Elevated mortgage rates are weighing on housing starts as well as new and existing home sales. House price appreciation is also likely turning a corner with the S&P CoreLogic Case-Shiller national home price index decelerating two-tenths to 6.3% year over year in April. New housing permits and construction starts took a sizeable step down in May, amid an already undersupplied market.

The rising inventory of new homes will help in rebalancing the demand-supply dynamics in housing markets. Cooler housing costs will be needed for inflation to reach and sustain the target of 2%. House prices don't feed directly into the CPI for rent of shelter, but usually lead the rent CPI by a year.

- Fed Chair Powell, along with others such as the Chicago and San Francisco Fed presidents, are starting to sound more confident on inflation progress and appear to be inclined to embark on a policy pivot. Speaking at the Economic Club of Washington, Chair Powell did not comment on the specific timing of the first rate cut but noted that the central bank was moving closer to lowering rates amid the recent progress on inflation.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.