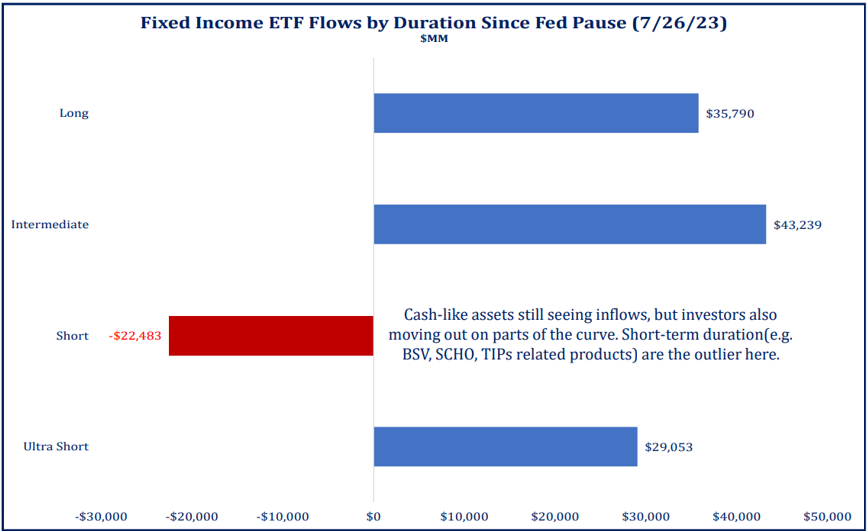

Investors took refuge in short-term Treasury bonds throughout 2023, where they reaped the rewards of higher-yielding money markets. Meanwhile, longer duration Treasuries have been mired in a bear market since 2020 but could finally start to see a reversal of fortune.

In just one month, the odds of a September rate cut have risen from nearly 50% to 100%, as of Wednesday. The market had pared back its expectation of five rate cuts to a single cut at one point. It has bumped back up to 2.5 cuts this year. A combination of cooling inflation, softer payrolls and weaker growth data have contributed to the uptrend in the federal funds futures market. Federal Reserve Chair Jay Powell reiterated last month that if the labor market were to slow “unexpectedly,” the Fed would be “prepared to respond” by cutting rates. June core consumer prices rose at their slowest monthly pace since January 2021 – during a winter flare-up of Covid-19 – setting the stage for rate cuts, as investors grapple with whether bad news for the economy is good news for rate policy.

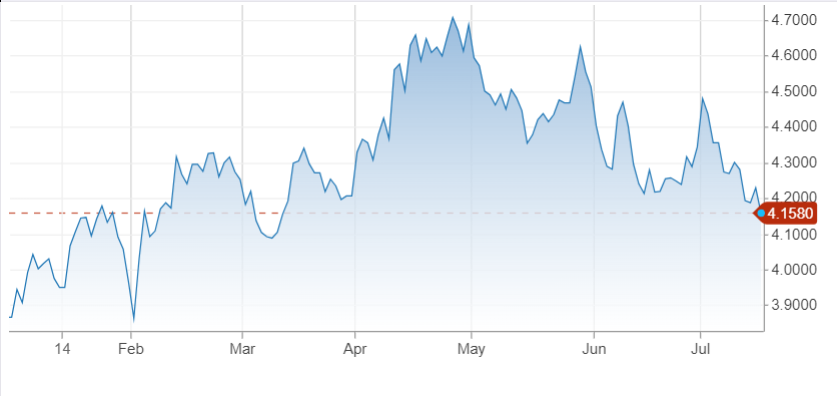

U.S. 10-Year Treasury Yield

The iShares 20+ Year Treasury Bond ETF (TLT) – the biggest long-duration bond ETF out there – just enjoyed a record day and week of inflows last month and is now coming off its fifth week of inflows north of $1 billion in 2024. The $55 billion fund, often treated as a proxy for the long-term Treasury bond market, has also raked in more than $7 billion in net inflows so far this year – a sign that perhaps investors are finally willing to either take on or extend duration.

TLT did suffer sizable outflows in January and March, as rate cut odds wavered amid signs of stickier inflation. But overall, it’s seen strong net positive inflows for the year. Bond returns have been sluggish up until interest rates peaked at the end of April. However, Treasuries have widely recouped most of their losses since January.

Moving into Longer Maturities

Other longer-term bond plays that have benefited from high hopes for lower rates include the Vanguard Intermediate-Term Treasury ETF (VGIT), which hauled in $1.4 billion in the last four weeks and $7.2 billion so far this year. The fund charges 0.04% with an average duration of five years. A virtually identical fund, the Schwab Intermediate-Term U.S. Treasury (SCHR), is slightly cheaper at 0.03% and has also seen inflows. Such funds serve as effective portfolio ballasts during periods of slowing growth and volatile inflation.

Another pair of funds that bear striking similarities would be the Vanguard Long-Term Treasury ETF (VGLT) and Schwab Long-Term U.S. Treasury ETF (SCHQ) – both of which have an average duration of more than 15 years. Both have netted inflows, with VGLT has bringing in an impressive $3.3 billion. On the flip side, the short-term equivalents of these four products have all suffered net outflows this year.

Beyond Treasuries, the Vanguard Long-Term Corporate Bond ETF (VCLT) and Vanguard Intermediate-Term Corporate Bond ETF (VCIT) offer primarily investment-grade fixed rate corporate bonds.

Sources: Strategas, Bloomberg

Building Duration into Model Portfolios

As investors looked to shore up positions and build resiliency at the midyear mark, largest asset managers both started adding duration to their model portfolios last quarter as well. State Street Global Advisors tacked on a 3% allocation in SPDR Portfolio Long Term Treasury ETF (SPTL) to its Moderate Growth active allocation ETF model last month. SPTL is a low-cost core SPDR Portfolio ETF. It aims to provide exposure to Treasuries with remaining maturities of up to 10 or more years. The fund is the among the cheapest of its kind. It charges 0.03%, and has seen north of $2 billion in net inflows so far.

We’ll be delving deeper into duration risk and more at VettaFi’s upcoming Fixed Income Symposium on Thursday, July 25.

For more news, information, and analysis, visit VettaFi | ETF Trends.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more commentaries by VettaFi